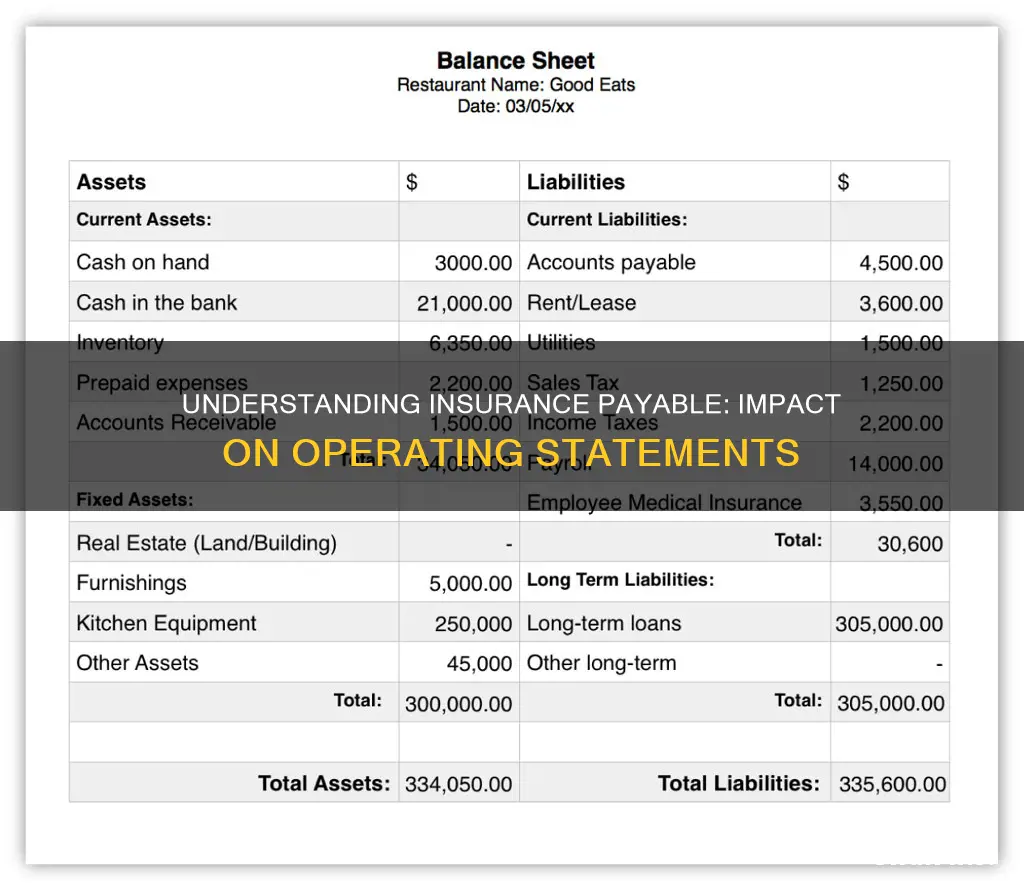

Insurance payable is a debt that is related to insurance expenses. It represents the amount of unpaid insurance premiums that a company owes. Insurance expenses, on the other hand, refer to the costs incurred by a company for insurance contracts and premium payments. While insurance payable is a liability that appears on a company's balance sheet, insurance expenses are typically found on the income statement. Prepaid insurance expenses, which are payments made in advance for future coverage, are initially recorded as assets on the balance sheet and later recognised on the income statement as they are utilised or expired. This accounting treatment ensures that expenses are accurately matched to the period in which they are incurred, providing a comprehensive view of a company's financial performance and position.

| Characteristics | Values |

|---|---|

| Definition of Insurance Payable | Insurance payable is the debt related to insurance expense, showing the amount of unpaid premiums. |

| Relationship with Insurance Expense | Insurance payable and insurance expense are interrelated; one does not exist without the other. |

| Recording in Financial Statements | Insurance payable is recorded on the company's balance sheet as an asset. It is not included in the income statement per generally accepted accounting principles (GAAP). |

| Treatment of Expired and Unexpired Premiums | Expired insurance premiums are reported as Insurance Expense, while unexpired insurance premiums are reported as Prepaid Insurance (an asset account). |

| Tax Implications | Insurance expenses can be deducted from tax liability as a business expense, depending on the type of business. |

Explore related products

What You'll Learn

![]()

Insurance payable is a debt related to insurance expense

Under the accrual basis of accounting, insurance expense is the cost of insurance that has been incurred, expired, or used up during the current accounting period for the non-manufacturing functions of a business. A manufacturer will report on its income statement the insurance expense incurred for its selling, general, and administrative functions. However, the insurance costs associated with the manufacturing function are included in the cost of the current period's output.

Prepaid expenses, such as insurance, are not included in the income statement per generally accepted accounting principles (GAAP). The GAAP matching principle requires accrual accounting, which stipulates that revenue and expenses must be reported in the period that the spending occurs, not when cash or money exchanges hands. Prepaid expenses are first recorded on the balance sheet as an asset. As the products and services are received, prepaid expenses are then recognized on the income statement for each period when the money is spent.

Any prepaid insurance costs that have not expired as of the balance sheet date should be reported as a current asset, such as Prepaid Insurance. On the other hand, expired insurance premiums are reported as Insurance Expense. If a retailer has incurred some insurance expense but has not yet paid the premiums, they should debit Insurance Expense and credit Insurance Premiums Payable, which is a liability or debt for the company. This Insurance Payable represents the amount that the retailer owes for the insurance coverage they have already received but have not yet paid for, making it a debt related to insurance expense.

Who Insures the Baby? Mom or Dad's Insurance?

You may want to see also

Explore related products

![]()

Insurance expense is the cost of insurance incurred during the accounting period

Insurance expense is the cost of insurance incurred during an accounting period. It is the amount of expenditure paid to acquire an insurance contract, including any additional premium payments. This expense is incurred for all insurance contracts, such as property, liability, and medical insurance. Under the accrual basis of accounting, the expenditure is only recorded as an insurance expense to the extent that the insurance has been consumed during the accounting period. For example, if a company pays $12,000 in advance for liability insurance coverage for the next twelve months, it records this expenditure as a current asset. Then, each month, the company charges $1,000 of this prepaid asset to expense, spreading the expense recognition over the coverage period.

Under the cash basis of accounting, the expenditure is charged to expense as soon as cash is paid to the insurance provider. The amount paid is charged to expense in a period, reflecting the consumption of the insurance over that time. If insurance relates to production operations, such as property coverage for a factory building, this expense can be included in an overhead cost pool. This means that some of the insurance expense will be included in ending inventory, and some will be assigned to the units sold during the period.

Prepaid insurance costs are reported as current assets on a company's balance sheet. Once these prepaid expenses are incurred, they are recognised on the income statement for each period when the money is spent. Expired insurance premiums are reported as Insurance Expense on the income statement.

Insurance payable is a related concept, representing the amount of a company's unpaid insurance premiums. It is a debt that must be settled as soon as possible, usually by the end of the current period, to avoid late charges or cancellation of the insurance policy. Insurance payable is a part of a corporate balance sheet, distinct from the income statement.

Insurance Lapses: How They Affect Your Rates

You may want to see also

Explore related products

![Careers for Teens Surgeon (Medical) [Special Edition]](https://m.media-amazon.com/images/I/71C5FTcgxAL._AC_UY218_.jpg)

![]()

Prepaid insurance costs are reported as current assets

Prepaid insurance is considered a current asset on a company's balance sheet. It represents the amount paid in advance for insurance coverage that will be utilised within the next 12 months. Prepaid expenses are not included in the income statement per generally accepted accounting principles (GAAP). This is because the GAAP matching principle requires accrual accounting, which stipulates that revenue and expenses must be reported in the period that the spending occurs, not when the money changes hands.

Prepaid expenses are first recorded on the balance sheet as an asset. However, as the products and services are received, prepaid expenses are recognised on the income statement for each period when the money is spent. Prepaid expenses are incurred for assets that will be received at a later time. Prepaid insurance is also considered an asset because of its redeemable value. Any remaining prepaid portion of the premium could be refunded to the business if the policy is cancelled before the period covered by those premiums has expired.

Prepaid insurance is recorded in the general ledger as a prepaid asset under current assets. A current asset is a financial resource that can be easily liquidated, or converted to cash, in a year or less. In contrast, a non-current or fixed asset, like real estate, cannot be easily liquidated in a year or less. The full value of the prepaid insurance is recorded as a debit to the asset account and as a credit to the cash account.

Each month, as a portion of the prepaid premiums are applied, an adjusting journal entry is made as a credit to the asset account and as a debit to the insurance expense account. This process is known as amortization. In this way, the asset value of the prepaid insurance will be reduced to zero at the end of the time period which was paid for in advance. Similarly, the expense will reach the total of the prepaid amount at the end of that same period.

How an OWVI Affects Your Insurance Rates

You may want to see also

Explore related products

![]()

Insurance expense is listed as an overhead cost

Insurance expenses are considered overhead costs, which are the ongoing costs required to run a business but are not directly tied to the production of goods or services. Overhead costs are expenses incurred by a company through its normal business operations and are essential to keep the business operational.

Insurance expenses are classified as overhead costs because they are not directly related to the production of goods or services. Instead, they are considered administrative or general and administrative (G&A) expenses, encompassing costs such as insurance payments, salaries for administrative personnel, and other day-to-day costs of running a business.

In accounting, insurance expenses can be classified as prepaid expenses, which are payments made for goods or services that will be received in the future. Prepaid expenses are initially recorded as assets on a company's balance sheet and are not included in the income statement per generally accepted accounting principles (GAAP). Once the expenses are incurred, the asset account is reduced, and the expense is then recorded on the income statement.

For example, a retailer with insurance policies for property, general liability, vehicles, and employees' compensation may pay insurance premiums in advance. Any unexpired insurance premiums as of the balance sheet date are reported as a current asset, such as Prepaid Insurance. Once the insurance coverage period begins and the expense is incurred, the prepaid asset account is reduced, and the insurance expense is recognised on the income statement.

By effectively managing overhead costs, including insurance expenses, companies can set competitive prices, maximise sales, and retain a significant portion of their revenues. Regularly reviewing overhead expenses also enables businesses to identify opportunities for cost savings and increase profitability.

Key Elements of Concealed Carry Insurance

You may want to see also

Explore related products

![]()

Insurance expense is separate from the balance sheet

An income statement is a financial document that tracks income and expenses, portraying the specifics of how a business arrived at the financial situation reflected on its balance sheet. It is broken down into sections for income and expenditures, with each section further divided into categories. One of these categories is insurance expense, which aggregates any insurance payments made during the period covered by the statement.

Insurance expenses are typically prepaid, which means they are paid in advance of receiving goods or services. Prepaid expenses are not included in the income statement per generally accepted accounting principles (GAAP). Instead, they are first recorded on the balance sheet as an asset. Only when the products and services are received are prepaid expenses recognised on the income statement. This is because the GAAP matching principle requires accrual accounting, which stipulates that revenue and expenses must be reported in the period that the spending occurs, not when the money changes hands.

However, the balance sheet itself does not include a specific line or category for insurance expense, or any other category of expenditure. This is because the balance sheet is a summary of a company's assets and liabilities at a particular moment in time, whereas insurance expense reflects a specific amount spent, rather than an asset or liability.

Therefore, insurance expense is separate from the balance sheet, which instead shows how much money a business has left after its insurance expense and other expenses have been factored into its overall financial position.

E&S Insurance Carrier: What's the Deal?

You may want to see also

Frequently asked questions

Insurance payable is the debt related to insurance expenses, showing the amount of unpaid premiums.

Insurance payable exists on a company's balance sheet only if there is an insurance expense. The company must pay premiums on all its insurance policies, and if they expire, they must be recorded as an expense.

Insurance payable is recorded as an expense for the accounting period. If the insurance covers production and operations, the expense is listed in an overhead cost pool and divided into each unit produced during the period.

Insurance expense is the cost of insurance incurred during the current accounting period. Insurance payable is the amount of unpaid premiums. One does not exist without the other.

No, insurance payable is part of a corporate balance sheet. However, the income statement will show the insurance expense incurred, and the balance sheet will reflect the lower bank balance after the insurance payment.