Life insurance is a contract between a policyholder and an insurance company that pays out a death benefit when the insured person passes away. There are several types of life insurance, including term and permanent plans, and the type of policy influences the payout process and amount. When a policyholder passes away, beneficiaries will typically receive the death benefit payout. However, there are instances where life insurance won't pay out, such as if the policyholder stopped paying premiums, lied on their application, or passed away during the waiting period. The payout process depends on whether the policy is term or permanent life insurance. Term policies offer straightforward payouts, while permanent policies involve a cash value component.

| Characteristics | Values |

|---|---|

| Types of life insurance | Term, Permanent, Whole, Universal, Variable Universal, Indexed Universal |

| Payout options | Lump-sum, Installments, Retained asset accounts, Annuities, Interest-only |

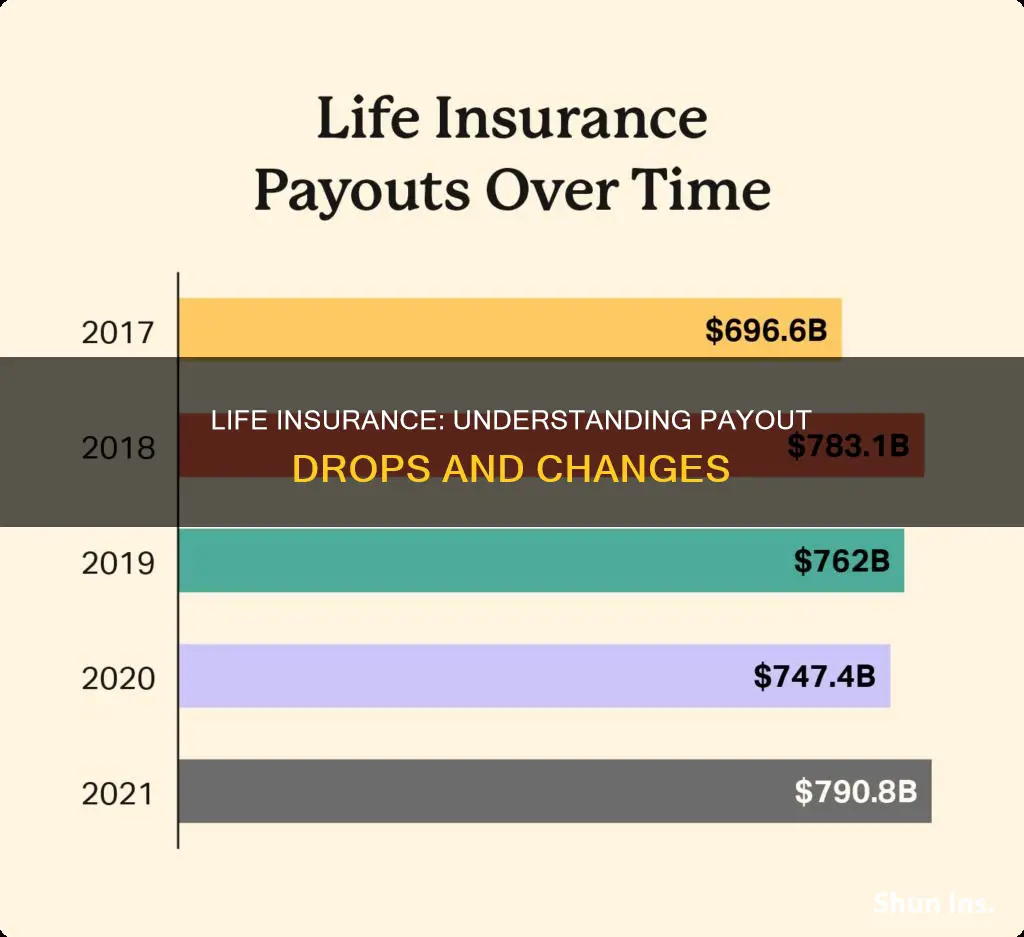

| Average payout | $168,000 |

| Time to payout | 14-60 days, depending on insurer procedures, claim filing time, policy length, cause of death, and state laws |

| Reasons for non-payout | Policyholder stopped paying premiums, lied on application, death by suicide, death during waiting period, death from criminal activity, term life policy expired |

Explore related products

What You'll Learn

![]()

Lump-sum payments

A lump-sum payment is the most common type of life insurance payout. It allows the beneficiary to receive the entire death benefit at once, usually tax-free. This option provides the beneficiary with immediate access to the full amount, which can be crucial for covering significant expenses or debts. Lump-sum payments offer the most flexibility to the beneficiary, who can use the money as they see fit. However, receiving a large amount of money all at once can be overwhelming, and it is up to the beneficiary to manage the funds wisely.

FedEx Part-Time Employees: Life Insurance Benefits Explained

You may want to see also

Explore related products

![]()

Installments

One of the options for receiving a life insurance payout is in the form of installments. The insurance company will pay the beneficiary a certain amount of money at regular intervals, such as monthly, quarterly, or yearly. This option provides a steady income stream, making financial planning easier. However, any interest earned on these payments may be subject to taxation.

The length of the installment period can vary, and some insurance companies offer lifetime installments. In this case, the insurance company estimates how long the beneficiary will live and bases the installment amount on that. If the beneficiary passes away before the end of the installment period, the remaining payments may go to a secondary beneficiary or be kept by the insurance company.

Another type of installment option is the specific income payout, where the beneficiary receives monthly installments over a set time period while the money is held in an interest-earning account. This ensures that the funds are not spent too quickly.

Compared to a lump-sum payment, installments provide less flexibility and control over the money. The beneficiary must carefully manage the installments to make them last, and there is a risk of the money running out before the end of the installment period. Additionally, the total amount received over time may be less than the original lump sum due to inflation.

When choosing between a lump sum and installments, it is important to consider the beneficiary's financial situation, age, and needs. Installments can be a good option for those who want a steady income stream and are concerned about spending a large sum too quickly. However, a lump sum provides more flexibility and control, allowing the beneficiary to invest the money as they see fit.

Life Insurance and DSHS: Counting Assets and Impact

You may want to see also

Explore related products

![]()

Retained asset accounts

A Retained Asset Account (RAA) is a temporary repository of funds, allowing beneficiaries to take their time to consider their financial options. The account is set up by the insurer in the beneficiary's name and works like a checking account. The beneficiary is provided with a checkbook to draw funds as needed. The principal and a minimum rate of interest are guaranteed by the insurer, with additional interest credited at a rate declared by the insurer. RAAs are not held in an FDIC-insured bank, but the money is protected and accessible at all times. The death benefit is income-tax exempt, but tax considerations may impact when the beneficiary withdraws the money.

Payout Options

There are several payout options available with an RAA:

- Single, lump-sum payment: The beneficiary can write a check for the full amount and take the payout as one payment.

- Installment payout: The beneficiary can choose a fixed monthly, quarterly, or annual payment for a set period or until the account is empty.

- Interest-only payout: The beneficiary can choose to receive interest from the account on a monthly, quarterly, or annual basis. The principal can be passed on to beneficiaries upon the original beneficiary's death.

Key Considerations

If you are considering an RAA, it is important to ask the following questions:

- What interest rate will be paid, how will it be determined, and how will it be credited to the account?

- Will the proceeds be held in a bank, and will they be FDIC-insured up to the legal limit?

- Will the proceeds be held by the insurer and covered by a state guaranty fund if the insurer fails?

- Will the proceeds be held in a bank checking or insurer draft account, and what banking services will be provided?

- What services will be provided at no charge, and what services will incur a fee?

Fidelity's Ladder Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Suicide or criminal activity

Suicide is a tragic but relatively common cause of death, and it is important to understand how life insurance policies handle such situations. While it may be challenging to consider, having this knowledge can ensure that your loved ones are protected financially.

Most life insurance policies include what is known as a "suicide clause", which typically prevents the insurer from paying out the full death benefit if the insured person dies by suicide within a specified period after the policy is issued. This period is often referred to as the exclusion period and usually lasts for the first one to three years, with two years being the most common duration. The purpose of this clause is to protect the insurance company from individuals who intend to end their lives shortly after purchasing a policy, thereby providing financial benefits to their beneficiaries.

During the exclusion period, if the policyholder dies by suicide, the insurance company may deny the death benefit or choose to refund only the premiums paid up to that point. However, once this exclusion period ends, most life insurance policies do cover suicide, and beneficiaries would be entitled to receive the full death benefit.

It is worth noting that certain types of life insurance policies may have different clauses and conditions that impact coverage in these circumstances. For example, group life insurance policies, often provided by employers, typically do not include a suicide clause, and beneficiaries would receive the death benefit regardless of the cause of death. On the other hand, supplemental life insurance purchased from an employer usually includes a suicide clause or contestability period.

Military life insurance policies, such as those offered by Veterans' Group Life Insurance (VGLI) and Servicemembers' Group Life Insurance (SGLI), also differ from traditional policies. These policies typically pay out the death benefit regardless of the cause of death, including suicide or acts of war.

In the case of criminal activity, life insurance policies may deny coverage if the insured person dies while committing or participating in illegal or dangerous acts. This is often covered under the contestability period, which allows the insurer to deny or reduce the death benefit if the insured dies within the first one to three years of the policy and the company finds undisclosed health conditions, risky behaviours, or discrepancies in the application.

To summarise, while suicide and criminal activity can impact life insurance payouts, the specific coverage depends on the type of policy, the presence of a suicide clause, and the duration of the exclusion and contestability periods. Being aware of these clauses and their implications is essential for understanding the financial protection provided by a life insurance policy.

Whole Life Insurance: Joint Policies' Value Increase Explained

You may want to see also

Explore related products

![]()

Policy delinquency

The consequences of policy delinquency can vary depending on the type of life insurance policy. For term life insurance policies, which provide coverage for a specified period, failure to pay premiums can result in the policy lapsing and the coverage ending. On the other hand, permanent life insurance policies, which provide coverage for the entire lifetime of the insured, may have some flexibility in terms of premium payments. Some permanent policies may allow for automatic premium loans when a payment is overdue, while others may have a grace period during which the policy remains in force even if the premium is not paid on time. However, if the policyholder consistently fails to pay premiums, the permanent policy may also lapse, and the insurer may cancel the coverage.

It is important to note that the specific provisions regarding policy delinquency and premium payments can vary across insurance companies and policies. Policyholders should carefully review their policy documents to understand the consequences of missed or late premium payments. Additionally, policyholders who are facing financial difficulties should contact their insurance company to discuss possible options, such as adjusting the premium payment schedule or exploring alternative coverage options.

Flight Emergencies: Insurance Coverage for Flight-for-Life Services

You may want to see also

Frequently asked questions

There are several types of life insurance payouts, including lump-sum payments, annuities, retained asset accounts, and specific income payouts. With a lump-sum payment, beneficiaries receive the entire death benefit at once. A retained asset account allows beneficiaries to withdraw funds from an interest-bearing account. An annuity provides a steady income stream over a set period, while the remaining amount earns interest. A specific income payout allows beneficiaries to receive monthly installments over a set time period.

It typically takes between 14 and 60 days for beneficiaries to receive a life insurance payout, but this can vary depending on factors such as the insurance company's procedures, the timing of the claim, the length of the policy, the cause of death, and state laws.

There are several reasons why life insurance might not pay out, including non-payment of premiums, misrepresentations or lies on the application, suicide within a specified time period, death resulting from criminal activities, the policy term expiring, and death occurring during the waiting period.

If a life insurance claim is denied, you can contact the insurer for more information, involve the state insurance department and attorney general, or consult a qualified attorney to guide you through the appeals process.