Mortgage insurance is an insurance policy that protects the lender or titleholder in the event that the borrower defaults on payments, passes away, or is otherwise unable to meet the contractual obligations of the mortgage. It is important to note that mortgage insurance does not protect the borrower; instead, it lowers the lender's level of risk by providing something to fall back on if the borrower does not hold up their end of the bargain with payments. The type of mortgage insurance one needs can depend on various factors, including the type of mortgage and the size of the down payment.

| Characteristics | Values |

|---|---|

| What is mortgage insurance? | An insurance policy that protects the lender or titleholder if the borrower defaults on payments, dies, or is otherwise unable to meet the contractual obligations of the mortgage. |

| Who does it protect? | The lender or titleholder. |

| Who does it not protect? | The borrower. |

| What does it protect against? | Loss if a sale is later invalidated because of a problem with the title. |

| What are the types of mortgage insurance? | Private mortgage insurance (PMI), qualified mortgage insurance premium (MIP) insurance, and mortgage title insurance. |

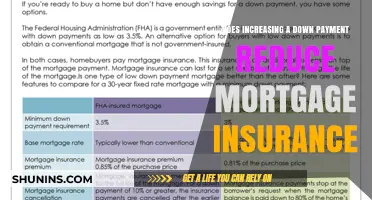

| What is PMI? | A type of mortgage insurance that mortgage lenders may require borrowers to purchase if they make a small down payment. |

| How is it paid? | Monthly premium added to the monthly mortgage payment, or as a lump-sum payment at the time of mortgage origination. |

| How to avoid PMI? | Put down at least 20% of the purchase price or choose a mortgage loan with a higher interest rate. |

| What is the cost? | Depends on the insurance company, coverage amount, and duration. |

Explore related products

What You'll Learn

![]()

Private mortgage insurance (PMI)

PMI is not always required. If you can make a 20% down payment, you won't have to pay PMI. You can also avoid PMI by choosing a mortgage loan with a higher interest rate that compensates the lender for the additional risk.

PMI protects the lender, not the borrower. If the borrower stops making payments on their loan, the PMI covers any losses for the lender. However, PMI does not protect the borrower, and they can still lose their home through foreclosure.

PMI can be paid in different ways. Most PMI is paid monthly, with little to no initial payment at closing. Sometimes, PMI is paid with a one-time upfront premium at closing. You can also pay with both upfront and monthly premiums.

Under certain circumstances, you can cancel your PMI. Lenders are required to cancel it when your mortgage balance reaches 78% of your home's original value or once you are halfway through your loan term, whichever comes first. You can also request to cancel PMI when your mortgage balance reaches 80% of your home's value.

Cobra House Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Mortgage protection insurance (MPI)

MPI is often compared to other types of insurance, such as life insurance or short- and long-term disability insurance. One key difference is that MPI protects the lender, while life insurance protects the policyholder's beneficiaries. MPI is also more restrictive in terms of coverage, as it only pays off the mortgage loan, whereas life insurance can be used to cover other expenses.

MPI policies are typically purchased through an insurance broker or directly from an insurance company, and the cost depends on factors such as the number of years left on the mortgage, the mortgage balance, the policyholder's age, and the property location. MPI premiums are usually paid monthly, and the coverage decreases over time as the mortgage balance is paid down.

While MPI can offer peace of mind and is easier to obtain for those with medical conditions, it tends to be more expensive than life insurance due to the more flexible underwriting criteria. It's important for individuals to carefully consider their personal situation and compare the costs and benefits of MPI and other insurance types before making a decision.

Doctors: Is Disability Insurance a Must-Have?

You may want to see also

Explore related products

![]()

Mortgage default insurance

In the case of a borrower's default, the insurer oversees all legal proceedings and payment enforcement, compensating the lender for any shortfalls after the property has been sold and all expenses have been paid.

It is important to distinguish between private mortgage insurance (PMI) and mortgage protection insurance (MPI). PMI is designed to protect the lender, while MPI protects the borrower by covering their mortgage payments if they lose their job, become disabled, or pass away. MPI is voluntary and may be a good option for those who feel their circumstances or risk factors warrant additional protection.

To minimise the cost of mortgage default insurance, borrowers can make a larger down payment or consider purchasing a less expensive home. It is also important to compare different insurance providers and understand the terms and costs associated with the policy.

Zaful Shipping Insurance: Worth the Extra Cost?

You may want to see also

Explore related products

![]()

Mortgage insurance premiums (MIPs)

Mortgage insurance protects the lender or titleholder if the borrower defaults on payments, passes away, or is otherwise unable to meet the contractual obligations of the mortgage. It does not protect the borrower.

Mortgage Insurance Premium (MIP) is a type of mortgage insurance that is required of homeowners who take out loans backed by the Federal Housing Administration (FHA). Unlike conventional loans, which typically only require private mortgage insurance (PMI) if a home down payment is less than 20% of the purchase price, all FHA loans require MIP. MIP is paid by homeowners who take out loans backed by the FHA. FHA-backed lenders use MIPs to protect themselves against higher-risk borrowers who are more likely to default on loans.

MIP is paid on an FHA-backed mortgage loan. The annual premium is calculated yearly, then divided by 12 and included in a borrower’s monthly mortgage payment. There are two parts of FHA MIP: upfront MIP and annual MIP. The upfront premium for all FHA loans is currently 1.75% of the loan amount. The upfront fee can be rolled into the mortgage, but this increases the loan amount and overall costs. For loans originated after June 3, 2013, if a down payment is less than 10% of the home's value, the borrower must pay the MIP for the life of the loan.

MIP can be removed by refinancing into a non-FHA product. Borrowers may also be able to cancel their MIP during the loan term depending on the loan’s origination date, value, down payment and lender.

BMW Gap Insurance: Is It a Smart Investment?

You may want to see also

Explore related products

![]()

Mortgage insurance and foreclosure

Mortgage insurance protects the lender, not the borrower, in the event that the borrower falls behind on their payments. If the borrower defaults, their credit score could suffer and they could lose their home through foreclosure. In the worst-case scenario, if the property is sold through foreclosure and the sale is not enough to cover the mortgage balance in full, mortgage insurance makes up the difference so that the lender is repaid the full amount.

Mortgage insurance lowers the risk to the lender of the borrower defaulting on their payments. There are several types of mortgage insurance, including private mortgage insurance (PMI), qualified mortgage insurance premium (MIP) insurance, and mortgage title insurance. PMI is typically required if the borrower makes a small down payment (less than 20% of the total value of the property). The cost of PMI varies depending on the down payment amount and credit score of the borrower.

MIP is required for all Federal Housing Administration (FHA) loans and costs the same regardless of the borrower's credit score, with a slight increase for down payments of less than 5%. With FHA loans, the borrower must pay both an upfront mortgage insurance premium (MIP) and a monthly MIP. The upfront cost can be rolled into the mortgage, but this increases the overall cost of the loan.

Mortgage title insurance protects against losses if it is found that someone other than the seller owns the property. This type of insurance is typically purchased before mortgage closing, when a title search is performed to uncover any liens or issues with the title that could prevent the owner from selling.

Mortgage protection insurance (MPI) is a type of insurance policy that helps the family of the policyholder make mortgage payments if the policyholder dies before the mortgage is fully paid off. MPI can also provide coverage for a limited time if the policyholder loses their job or becomes disabled after an accident. MPI is not the same as PMI, which protects the lender, not the borrower, in the event of default.

The Impact of Driver's Ed on Insurance Rates: A Farmer's Perspective

You may want to see also

Frequently asked questions

Yes, mortgage insurance protects the lender or title holder in the event of a borrower's default. It is important to note that mortgage insurance does not protect the borrower, and they may still lose their home through foreclosure.

Mortgage default insurance is required when a borrower makes a down payment of less than 20%. It protects the lender in the event of a borrower's default by compensating for any shortfall after the property has been sold.

PMI (Private Mortgage Insurance) protects the lender in the event of a borrower's default, while MPI (Mortgage Protection Insurance) protects the borrower by covering their mortgage payments if they lose their job or become disabled.

To qualify for mortgage default insurance, you need to have an amortization period of less than 25 years and make a higher down payment if the purchase price is between $500,000 and $999,000. If the purchase price is over $1 million, you will not need mortgage default insurance as a minimum 20% down payment is required.