Pancreatitis is an inflammation of the pancreas, which can cause both mental and physical stress. It can be categorised as acute or chronic. Acute pancreatitis is a temporary condition that usually passes within a few days, whereas chronic pancreatitis is a long-term, progressive condition that gets worse over time. Both types can impact your ability to obtain life insurance, but it is still possible to obtain coverage. Life insurance companies will want to know the extent of the damage to the pancreas and whether there are any other underlying health conditions. If you have pancreatitis and are looking for life insurance, it is important to work with an experienced agent who can help you find the best rates.

| Characteristics | Values |

|---|---|

| Does pancreatitis make you ineligible for life insurance? | No, individuals with a history of pancreatitis can qualify for life insurance, but they are considered a higher risk. |

| Types of pancreatitis | Acute pancreatitis, chronic pancreatitis |

| Acute pancreatitis | Temporary condition with a sudden onset of inflammation of the pancreas |

| Chronic pancreatitis | Long-term, progressive condition that gets worse over time |

| Symptoms of acute pancreatitis | Pain in the upper abdomen, abdominal pain radiating to the back, abdominal pain after eating, tenderness in the abdomen |

| Symptoms of chronic pancreatitis | Pain in the upper abdomen, unexplained weight loss, indigestion and pain after eating, fatty stools, lightheadedness |

| Causes of pancreatitis | Abdominal injury and/or surgery, use of certain medications, family history, high calcium or triglyceride levels in the blood, alcohol use, gallstones, infections, autoimmune disease, inherited gene mutations, complications of cystic fibrosis |

| Complications of pancreatitis | Cysts and infections, chronic pancreatitis, pancreatic pseudocysts, increased risk of pancreatic cancer |

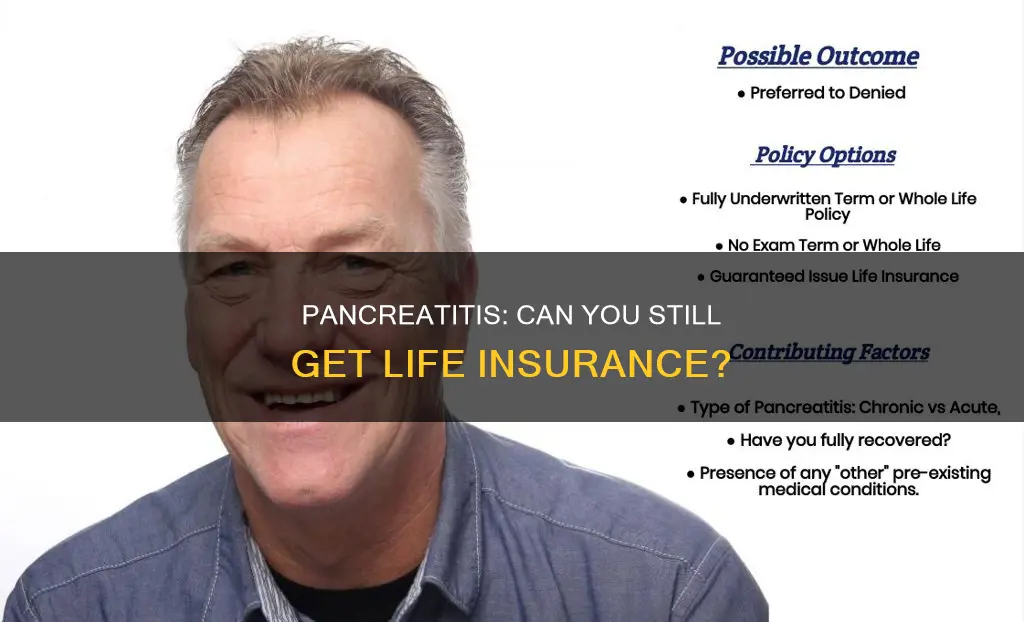

| Application process for life insurance with pancreatitis | Life insurance companies will ask about the type of pancreatitis, extent of damage to the pancreas, underlying health conditions, and may request medical records and test results |

| Factors affecting life insurance rates | Number of pancreatitis attacks, time since last attack, underlying health condition causing pancreatitis, severity of symptoms and attacks, smoking and alcohol use, permanent damage to the pancreas or other organs |

Explore related products

What You'll Learn

![]()

Can I qualify for life insurance if I have pancreatitis?

Yes, it is possible to qualify for life insurance if you have pancreatitis. However, the type of pancreatitis you have will be a key factor in the life insurance company's decision.

Acute Pancreatitis

Acute pancreatitis is a temporary condition that usually occurs once and can be treated with rest, hydration and pain relief. If you have suffered only one or two attacks of acute pancreatitis that were not caused by a serious or chronic illness, and they were successfully treated, you can expect to receive the best health class ratings. This assumes that you are generally in good health and are not a smoker.

If you have had multiple acute attacks, it may be best to delay your life insurance application until a certain amount of time has passed without an attack. Some companies require you to be asymptomatic for at least one year. Once you have cleared this time frame, you can expect to receive a Standard health class rating.

Chronic Pancreatitis

Chronic pancreatitis is a long-term, progressive condition that gets worse over time. It is caused by persistent inflammation of the pancreas, which leads to irreversible damage. Chronic pancreatitis will likely result in a Sub-Standard rating with high premiums. You could even be declined if not enough information is supplied.

The life insurance company will want to know the underlying health condition causing the chronic pancreatitis. If the cause is genetic, due to alcohol or drug use, or due to more serious health conditions, this will affect the health class rating.

Guaranteed Acceptance Life Insurance

If you have been declined for traditional life insurance due to permanent damage to the pancreas and other health complications, you may want to consider guaranteed acceptance life insurance. These policies do not require you to disclose information about your pancreatitis and allow you to secure coverage regardless of your medical background. However, there is a two-year waiting period before the policy becomes fully in force.

Working with an Agent

When searching for life insurance with pancreatitis, it is important to work with an experienced agent who can help you navigate the underwriting process and find the best rates. They will need detailed information about your condition, including the cause, dates of episodes, treatment, and any residual effects or complications.

Life Insurance Coverage for Emphysema: What You Need to Know

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Why do life insurance companies care about a pancreatitis diagnosis?

Life insurance companies care about a pancreatitis diagnosis because the condition can lead to severe, and sometimes life-threatening, complications. Pancreatitis is an inflammation of the pancreas, an organ that sits in the upper region of the abdomen, behind the stomach. The pancreas produces digestive enzymes and hormones, including insulin, which is crucial for regulating blood sugar levels.

There are two types of pancreatitis: acute and chronic. Acute pancreatitis is a temporary condition that usually resolves within a few days. However, recurring attacks of acute pancreatitis can lead to chronic pancreatitis, which is long-term and degenerative. Chronic pancreatitis can cause permanent damage to the pancreas, including fibrosis and calcification, leading to digestive problems and diabetes.

The complications related to pancreatitis, especially chronic pancreatitis, can be life-threatening, which is why life insurance companies consider individuals with this diagnosis a high risk. These complications include cysts and infections that may require surgery. Additionally, chronic pancreatitis can increase the risk of pancreatic cancer.

When assessing an individual with a pancreatitis diagnosis, life insurance companies will want to know the type of pancreatitis (acute or chronic) and the extent of damage to the pancreas. They will also be interested in any underlying health conditions, such as alcohol abuse, that may have contributed to the development of pancreatitis.

The impact of a pancreatitis diagnosis on life insurance rates will depend on the severity and frequency of the condition, the presence of permanent damage, and any impact on overall life expectancy. Individuals with chronic pancreatitis may find it more difficult to get approved for traditional life insurance coverage or may face higher rates.

In summary, life insurance companies care about a pancreatitis diagnosis because of the potential for severe complications and the impact on the individual's overall health and life expectancy. The type and severity of pancreatitis will play a significant role in the life insurance underwriting process and the resulting rates offered to the individual.

Life Insurance and Disaster: What's Covered and What's Not?

You may want to see also

Explore related products

![]()

What information will insurance companies ask for?

When applying for life insurance, you will be asked to provide a range of personal information. This will include basic information such as your name, address, occupation, and employer. You will also be asked about your lifestyle habits (e.g. smoking, drinking, exercise), your health history, and your family's health history. Be prepared to disclose any pre-existing medical conditions, history of moving violations, DUIs, and any dangerous hobbies (e.g. auto racing or skydiving).

- When was your first attack/diagnosis?

- How many attacks have you experienced?

- What symptoms led to your diagnosis?

- What type of pancreatitis were you diagnosed with?

- How was your pancreatitis treated?

- Did your treatment require a hospital stay?

- Do you know why you developed pancreatitis?

- Have you been diagnosed with any other pre-existing medical conditions?

- Are you currently taking any prescription medications?

- Do you have any history of drug or alcohol abuse?

- Do you have any issues with your driving record?

- Have you been hospitalized for any reason in the past two years?

- Are you currently working?

- Have you applied for or received any form of disability benefits in the past 12 months?

- Do you have any criminal convictions?

- Have you ever been declined for life, health or disability insurance?

- How will you pay for your policy?

In addition to these questions, you will also need to provide the names and contact details of your primary physician and the physician who last treated you.

The insurance company will also want to know about your family's health history, particularly whether your parents or siblings have been diagnosed with or treated for conditions such as heart disease, cancer, diabetes, or mental illness.

Life Insurance Checks: Impact on Social Security?

You may want to see also

Explore related products

![]()

What rate can I qualify for?

The rate you can qualify for depends on several factors, including the type of pancreatitis you have, the severity of the condition, and your overall health. Here are some key points to consider:

- Acute Pancreatitis: If you have acute pancreatitis, the rate you can qualify for will depend on the number of occurrences and the underlying cause. If it is a one-time event caused by gallstones and you have fully recovered, you can typically qualify for standard life insurance rates. However, multiple episodes of acute pancreatitis may lead underwriters to suspect alcohol abuse, resulting in a postponement of your application for 1-2 years of documented abstinence. If alcohol use is not a factor and there are no permanent health complications, you may be able to obtain standard rates even with multiple episodes.

- Chronic Pancreatitis: Chronic pancreatitis is generally considered a more serious condition and may result in higher rates or even a decline for traditional life insurance coverage. The irreversible damage caused by chronic pancreatitis, such as fibrosis and the resulting malnutrition and diabetes, will be assessed by underwriters. The underlying condition leading to chronic pancreatitis and the extent of damage to the pancreas will be key factors in determining your rate.

- Health Factors: In addition to the type and severity of pancreatitis, underwriters will consider various health factors when determining your rate. These factors include the diagnosis date, the cause or source of pancreatitis, dates of all episodes, alcohol consumption, smoking history, any residual health effects, and other underlying health issues.

- Guaranteed Acceptance Policies: If you have been declined for traditional life insurance due to permanent damage or health complications from pancreatitis, you may consider guaranteed acceptance life insurance policies. These policies do not require disclosure of medical information and provide coverage regardless of your health background. However, they typically have a 2-year waiting period before the policy becomes fully effective.

- Working with an Agent: It is recommended to work with an experienced agent who can guide you through the process and help you find the best rates. They can assist in organising your medical information and presenting it effectively to insurance companies.

Employer Life Insurance: Cash Value or Policy Benefit?

You may want to see also

Explore related products

![]()

How can I get the best life insurance?

The best life insurance for you will depend on your circumstances, but there are several things you can do to help ensure you get the best life insurance for your needs.

Shop around

First, it's important to shop around and compare prices and policies between different insurers. You might find that some insurance companies offer similar policies for different prices. For instance, State Farm and Nationwide could offer policies with the same coverage amount and riders for a different cost.

Check customer reviews

It's also worth looking at how satisfied customers are with an insurer. You can visit the National Association of Insurance Commissioners (NAIC) website to see the number of complaints filed within a state.

Assess the company's financial strength

Another thing to consider is whether the company will be able to pay out to your beneficiaries when you die. You can assess this by looking at the company's financial rating from a credit rating agency like AM Best. A high credit rating indicates that a company is financially strong and will likely be around to pay out to your beneficiary when you die.

Work with an independent agent

Working with an independent agent who has experience working with a wide variety of pre-existing medical conditions and has access to dozens of different life insurance companies can be beneficial. This means they won't have to rely on a "one-size-fits-all" approach and can help you find the best policy for your specific circumstances.

Take your time

Taking your time to review your options and ask a lot of questions can also help you get the best life insurance for your needs. Don't rush into a decision, and make sure you understand the different policies and what they cover before choosing one.

Life Insurance After Retirement: What You Need to Know

You may want to see also

Frequently asked questions

Yes, individuals who have been previously diagnosed with Pancreatitis can and often will be able to qualify for a traditional term or whole life insurance policy. However, it depends on the type of Pancreatitis and the severity of the damage to the pancreas.

Pancreatitis is a severe infection that can lead to severe, and sometimes life-threatening, complications. There are two types of Pancreatitis: Acute Pancreatitis, which is a temporary condition, and Chronic Pancreatitis, which is a long-term, progressive condition. Due to the potential severity of the disease, insurance companies will want to know more about your diagnosis before making a decision.

Insurance companies will likely ask about the cause and dates of your diagnosis, the treatment you received, whether you've had any surgeries, your alcohol consumption, and any other underlying health issues. They will also want to see your medical records and review test results.