Medicare is a health insurance program provided by the federal government, specifically for people over 65. While it covers most hospital and doctor expenses, there are still out-of-pocket costs, deductibles, copayments, and coinsurance that the user must pay. This is where supplemental insurance comes in. Also known as Medigap, it is an extra insurance policy provided by private insurance companies to help pay these additional costs. Medigap policies do not cover prescription drugs, dental care, routine eye care, or long-term care. To purchase a Medigap policy, you must be enrolled in Medicare Part A and B.

| Characteristics | Values |

|---|---|

| What is Supplemental Insurance? | Extra insurance to help cover out-of-pocket costs and gaps in coverage |

| Who is it for? | Those with Medicare |

| What does it cover? | Financial protection for deductibles, coinsurance, and other medical expenses not fully covered by Medicare |

| What is it called? | Medicare Supplement Insurance or Medigap |

| Who sells it? | Private insurance companies |

| What are the requirements? | You need to have Original Medicare – Part A (Hospital Insurance) and Part B (Medical Insurance) |

| What is the cost? | You pay a monthly premium to the insurance company |

| What is not covered? | Prescription drugs, dental care, routine eye care, or long-term care |

| What are the alternatives? | Medicare Advantage Plan |

Explore related products

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. It helps to pay your share of out-of-pocket costs in Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Generally, you must have Original Medicare (both Part A and Part B) before you can buy a Medigap policy. Medigap policies do not typically cover long-term care, vision, dental, hearing aids, private nursing, or prescription drugs. However, some Medigap policies offer coverage when you travel outside the United States.

Medigap policies are designed to fill in the gaps in Original Medicare coverage. For example, under Medicare Part B, the government pays for 80% of doctor services, while the patient is responsible for the remaining 20%. In the case of a $100,000 surgery, the patient would owe $20,000. A Medigap policy could help cover this large out-of-pocket expense, providing financial protection for deductibles, co-payments, and coinsurance costs.

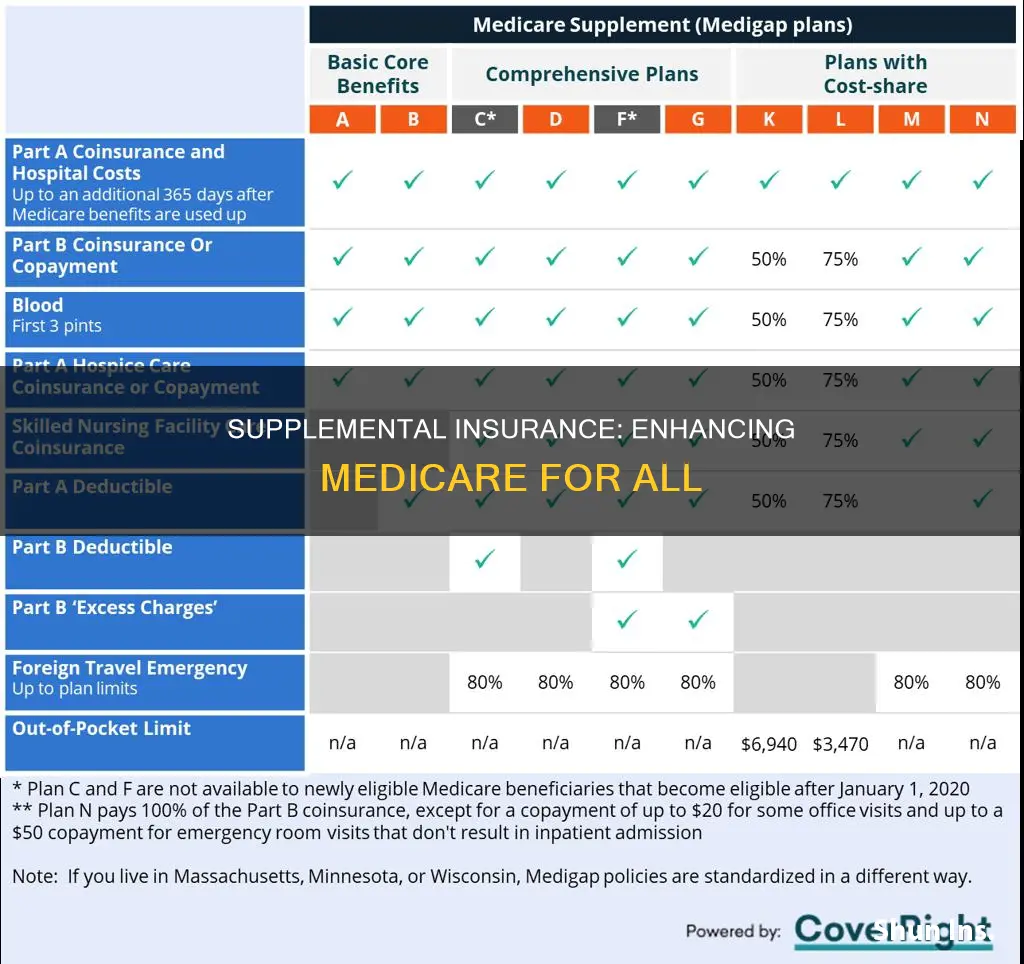

There are standardized Medigap plans offered by private insurance companies, with each plan balancing coverage and premium costs. For instance, Medigap Plan K may have a lower premium because it only covers 50% of the Medicare Part B coinsurance, while Plan C covers the entire Part B coinsurance but charges a higher monthly premium. During the Medigap open enrollment period, which lasts six months after enrolling in Medicare Part B at age 65, individuals can sign up for any Medigap plan available in their area. After this period, enrollment may be subject to health underwriting, and pre-existing conditions could result in higher premiums or even denial of coverage.

It is important to note that Medigap policies only cover medical bills and do not include prescription drugs, dental care, routine eye care, or long-term care. To cover these expenses, individuals may need additional insurance policies. Medigap is one option for supplemental insurance, and there are also Medicare Advantage plans that can help cover retirement health insurance costs. When considering supplemental insurance, it is recommended to review the potential costs and benefits to ensure it aligns with your specific needs and financial situation.

Passport Insurance in Kentucky: Application Process Simplified

You may want to see also

Explore related products

![]()

Coverage gaps

Medicare Part A and Part B may leave beneficiaries with out-of-pocket expenses, resulting in coverage gaps for certain healthcare services. These out-of-pocket costs typically include a yearly deductible that beneficiaries must meet before their Part B coverage begins. After meeting the deductible, beneficiaries are responsible for a coinsurance amount, which is a percentage of the Medicare-approved cost for covered services. This means that individuals may still need to pay a portion of their healthcare costs even after Medicare pays its share.

Medicare Part B may not cover certain services, such as routine vision and dental care, or specific prescription drugs that are not administered in a medical setting. Beneficiaries must be aware of these limitations and expenses when utilizing Part B services. Additionally, Medicare Part B covers only 80% of doctor services, leaving the beneficiary to pay the remaining 20%. This can result in large bills for expensive surgeries or treatments.

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private company to help pay for these out-of-pocket costs in Original Medicare. Medigap policies help cover deductibles, coinsurance, and copayments, providing financial protection for beneficiaries. Some Medigap policies also offer coverage for services that Original Medicare doesn't, such as emergency medical care when travelling outside the US. However, Medigap policies generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

It is important to be aware of coverage gaps before signing up for Medicare to ensure that you choose the most suitable plan for your healthcare needs. Understanding these gaps allows you to maximize your benefits, plan for costs, and access the care you need from trusted providers. Additionally, evaluating the coverage gaps of different plans can help you find one that meets your unique healthcare requirements and provides comprehensive and cost-effective coverage.

United Insurance: Steps to Apply for Paneling

You may want to see also

Explore related products

![]()

Out-of-pocket costs

Medicare Supplement Insurance (Medigap) is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare. Medigap plans help cover out-of-pocket costs associated with Original Medicare, such as copayments, coinsurance, and deductibles. Each plan covers different out-of-pocket costs, and some Medigap policies include extra benefits, such as coverage for emergency medical care when travelling outside the US.

Medicare Advantage (Part C) bundles hospital, doctor, and often drug coverage, and it caps out-of-pocket expenses. This means there is a limit on what you pay out of your own pocket each year. However, Medicare Advantage restricts you to a network and usually requires referrals for specialists.

Medigap policies help to limit unexpected medical costs and provide predictable out-of-pocket costs and comprehensive coverage. During the Open Enrollment Period, which lasts six months from when you turn 65 or older and enrol in Medicare Part B, you cannot be denied coverage or charged more due to medical conditions.

Supplemental Health Insurance Plans: Qualifying for Medicaid

You may want to see also

Explore related products

![]()

Eligibility and enrolment

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that helps pay for out-of-pocket costs in Original Medicare (Parts A and B). While Medigap is optional and not a requirement, it can provide valuable financial protection against high deductibles, copays, and coinsurance.

Eligibility and Enrollment

Medigap is available to those who are enrolled in Original Medicare, which consists of Part A (Hospital Insurance) and Part B (Medical Insurance). Most people are eligible for premium-free Part A if they or their spouse, parent, or child, have a sufficient number of quarters of coverage (QCs) based on earnings. Those who are not eligible for premium-free Part A can apply for it by contacting the Social Security Administration and enrolling in Part B. It is important to note that Part B requires the payment of a monthly premium.

Eligibility for Part B depends on whether an individual is eligible for premium-free Part A or if they need to pay a premium for Part A. Those who are eligible for premium-free Part A can enroll in Part B once they are entitled to Part A. For those who must pay a premium for Part A, additional requirements for enrolling in Part B include being a U.S. resident and citizen or a lawfully admitted permanent resident who has resided in the U.S. for at least 5 continuous years prior to applying for Medicare.

The best time to purchase a Medigap policy is when you turn 65 and enroll in Medicare Part B. During the six-month Medigap open enrollment period, insurance companies cannot use medical underwriting to charge higher rates or deny coverage based on health history. Individuals whose Medicaid eligibility has been terminated may also enroll in Medicare using a Special Enrollment Period (SEP). This SEP begins when notified of the upcoming Medicaid termination and lasts for six months after the termination.

Understanding Self-Insured Medical Coverage: What You Need to Know

You may want to see also

Explore related products

![]()

Medicare Advantage

When considering a Medicare Advantage Plan, it is essential to review the specific rules and restrictions. For example, you may need to use doctors within the plan's network, and joining a plan might affect your employer or union coverage. Additionally, Medicare Advantage Plans have the right to disenroll you for various reasons, such as moving outside their service area or losing Medicare eligibility.

To enrol in a Medicare Advantage Plan, you must have both Part A and Part B. During the initial enrolment period for Medicare Part B, there is a Medigap open enrolment period of six months, during which you can also sign up for a Medicare Advantage Plan. After this period, you can still apply, but the insurance company may ask about your health and pre-existing conditions, which could impact your premium or eligibility.

Health Insurance and Medical Marijuana: What's Covered?

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare.

Medigap covers out-of-pocket expenses like copayments, coinsurance, and deductibles. It helps fill in the gaps in Original Medicare coverage. However, it does not cover prescription drugs, dental care, routine eye care, or long-term care.

You can buy Medigap if you have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). During your Medigap Open Enrollment Period, which lasts for six months starting when you turn 65 and enroll in Medicare Part B, you are guaranteed eligibility regardless of pre-existing conditions.

There are ten Medigap plans offered in most states, named by letters A through N (excluding C and F, which are no longer available to new beneficiaries). Each plan offers the same basic benefits, but the premium costs vary. You can choose a plan that balances the level of coverage you need with the premium you can afford.

You can buy a Medigap policy from any licensed insurer in your state. Remember that you cannot have both a Medicare Supplement policy and a Medicare Advantage plan.