Universal life insurance is a type of permanent life insurance that offers lifelong coverage as long as you pay your premiums. Unlike term life insurance, which only covers you for a set period, universal life insurance allows you to adjust your premiums and death benefit. It also comes with a cash value component that grows over time and can be used to pay premiums. While universal life insurance offers flexibility, it is important to monitor the performance of your cash value to ensure that your policy does not lapse.

| Characteristics | Values |

|---|---|

| Coverage | Universal life insurance offers lifelong coverage |

| Premium payments | Universal life insurance provides flexibility in paying premiums |

| Cash value | Universal life insurance has a cash value component that grows over time |

| Death benefit | Universal life insurance allows the death benefit to be adjusted |

| Lapse | If the cash value drops to zero, the policy will lapse |

| Interest rate | Universal life insurance has a minimum guaranteed interest rate |

| Loans | Universal life insurance allows loans against the cash value |

| Taxation | Some withdrawals from the cash value are taxable |

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

What You'll Learn

![]()

Universal life insurance policies can be adjusted

Secondly, universal life insurance policies may also allow adjustments to the death benefit. Policyholders can choose to increase or decrease the size of their death benefit, although this may require a medical examination. Increasing the death benefit can be done by building up the cash value, while decreasing it can help to lower premiums.

Universal life insurance policies also offer the flexibility to borrow against the accumulated cash value. Policyholders can take out loans or make partial withdrawals from the cash value, which can be useful in times of financial need. However, it is important to closely monitor the cash value and ensure it does not fall to zero, as this can cause the policy to lapse.

Finally, universal life insurance policies provide the option to surrender the policy and receive the cash value if the policyholder decides they no longer want the coverage. This flexibility allows policyholders to adjust their coverage according to their changing needs and financial circumstances throughout their lifetime.

Therapy and Life Insurance: What's the Connection?

You may want to see also

Explore related products

![]()

Universal life insurance is permanent

Universal life insurance is a form of permanent insurance, meaning that coverage can last for your lifetime if you pay your premiums. This is in contrast to term life insurance, which only covers the holder for a set period, such as 10 or 20 years. Universal life insurance is often compared to whole life insurance, which also offers lifelong coverage but is generally less flexible and more expensive than universal life insurance.

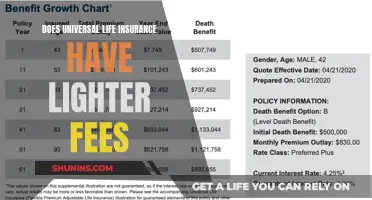

Universal life insurance has a cash value component that is separate from the death benefit. Each time a premium payment is made, a portion is put toward the cost of insurance (such as administrative fees and the death benefit) and the rest becomes part of the cash value. The cash value is guaranteed to grow at a minimum annual interest rate but may grow faster, depending on the company's market performance.

The cash value of a universal life insurance policy can be used in several ways. Firstly, if the policyholder decides they no longer want the policy, they can surrender it to the company and receive the cash value. Secondly, the cash value can be used as loan collateral, allowing the policyholder to borrow money from the company. Finally, the cash value can be used to pay premiums. However, it is important to closely monitor the cash value, as policies will lapse if the cash value drops to zero.

Universal life insurance policies typically mature when the policyholder reaches a certain age (often between 85 and 121). When a policy reaches its maturity date, the policyholder generally receives a payment and the coverage ends. The payment amount may be equal to the death benefit or a specified amount, but it is usually equivalent to the policy's cash value.

Trustage Life Insurance: Suicide Coverage and Exclusions

You may want to see also

Explore related products

![]()

Universal life insurance has a cash value component

The cash value of a universal life insurance policy can be used in several ways:

- Surrender value: If you decide you no longer want the policy, you can give it back to the company, which is called surrendering it, and the company will give you the cash value.

- Loan collateral: You can borrow money from the company and use the cash value as collateral. This is the maximum amount you can borrow, and these loans are subject to interest rates set by the company.

- Premium payments: You can use the cash value to pay some or all of a premium. It's important to monitor the cash value closely, as policies will lapse if the cash value drops to zero.

The premiums of a universal life insurance policy are split between the cost of coverage and the cash value. Policyholders can choose how much to pay within the minimum and maximum premium amounts. Many people choose to pay the maximum for the first several years of coverage, building a large cash value that can be used to pay premiums later on. This can be a good strategy for those who want permanent coverage during retirement when income may be smaller. However, if the cash value runs out, policyholders may be stuck paying the full cost of insurance, and there will be no surrender value.

Universal life insurance policies mature when the policyholder reaches a certain age (often 85 to 121). Generally, when a policy reaches its maturity date, the policyholder receives a payment, and the coverage ends. The payment is usually equal to the policy's cash value and may be the death benefit or a specified amount.

It's important to choose a policy with a suitable maturity date, considering the reason for purchasing the coverage. For example, if the primary purpose is to prevent heirs from paying inheritance taxes, a very high age for the maturity date should be set.

Life Insurance and Short-Form Death Certificates: What's Accepted?

You may want to see also

Explore related products

![]()

Universal life insurance is flexible

Universal life insurance is a form of permanent insurance that offers flexible premium payments and death benefits. It is a lifelong coverage option that provides flexibility in paying premiums, a cash savings component, and a death benefit. Unlike term life insurance, which only covers a set period, universal life insurance allows individuals to increase or decrease their premium payments within certain limits. This flexibility can be beneficial for those with varying incomes or changing financial circumstances.

The cash value component of universal life insurance is an important aspect of its flexibility. Each premium payment is split between the cost of insurance and the cash value. The cash value grows over time, earning interest based on the insurer's set rate or the market performance of the insurer's portfolio. This cash value can be used to pay premiums, taken as a loan, or withdrawn. However, careful management is required to ensure the cash value does not deplete and cause the policy to lapse.

Universal life insurance also offers the flexibility to adjust the death benefit. Depending on the policy, individuals may be able to increase or decrease the death benefit amount, allowing them to tailor the coverage to their needs and budget. This adjustability is a significant advantage for those who experience changes in their financial situation or long-term goals.

While universal life insurance provides flexibility, it is important to note that it comes with certain risks. The cash value can be affected by market performance, and if interest rates drop, the growth of the cash value may be impacted. Additionally, there is a risk of policy lapse if the cash value is insufficient to cover the cost of insurance. Therefore, regular monitoring and management of the policy are necessary to maintain coverage.

In summary, universal life insurance is flexible in terms of premium payments, death benefits, and the cash value component. This flexibility allows individuals to customize their coverage and make adjustments as their financial circumstances change. However, it is important to carefully manage the policy to avoid potential risks and ensure lifelong coverage.

Term Life Insurance: Does GEICO Offer This?

You may want to see also

Explore related products

![]()

Universal life insurance is not guaranteed

One of the key differences between universal life insurance and whole life insurance is that the latter offers guaranteed coverage as long as the premiums are paid, whereas universal life insurance provides flexibility in exchange for fewer guarantees. While universal life insurance allows for adjustable premiums and death benefits, there is a risk that the policy could become underfunded and lapse if the cash value is insufficient to cover the cost of insurance.

The cash value component of universal life insurance is crucial to the policy's longevity. The cash value grows over time, earning interest set by the insurer, and can be used to pay premiums or withdrawn as loans. However, if the cash value is not carefully monitored and managed, it could deplete, leading to a lapse in coverage.

Additionally, universal life insurance policies are subject to changes in interest rates. If interest rates drop, the cash value may not perform well, and the policyholder may need to increase premium payments to maintain coverage. This uncertainty makes universal life insurance less predictable than whole life insurance, where premiums and benefits are fixed.

In summary, while universal life insurance offers flexibility and the potential for cash value growth, it is not a guaranteed contract. Policyholders must actively manage their policies to ensure sufficient funding and avoid a lapse in coverage. The risk of large payment requirements or policy lapse, unpredictable returns, and the potential for high administrative fees are important considerations when deciding whether universal life insurance is the right choice.

Teamsters Life Insurance: Interest Included or Excluded?

You may want to see also

Frequently asked questions

Universal life insurance is a form of permanent insurance, meaning coverage can last for your lifetime if you pay your premiums. This is different from term life insurance, which only covers you for a set period, such as 10 or 20 years.

Universal life insurance offers lifelong coverage and the flexibility to adjust your premiums and death benefit. Whole life insurance, on the other hand, offers consistent premiums and guaranteed cash value accumulation. Whole life insurance premiums are also typically higher than those of universal life insurance.

Some advantages of universal life insurance include flexible death benefits, the ability to borrow against the policy, and the potential for cash value growth. However, there is a higher risk of policy lapse, returns are not guaranteed, some withdrawals may be taxed, and administrative fees tend to be high.