Life insurance is a contract between an insurance company and a policyholder, where the insurer agrees to pay a sum of money to one or more named beneficiaries when the insured person dies. In exchange, the policyholder pays premiums to the insurer during their lifetime. The death benefit is usually tax-free and can be used by the beneficiaries for any purpose, such as paying off debts, covering living expenses, or funding children's education. There are two main types of life insurance: term life insurance, which lasts for a certain number of years, and permanent life insurance, which remains active until the insured person dies or stops paying premiums. Permanent life insurance policies, such as whole life and universal life, also have a cash value component that can be accessed by the policyholder during their lifetime. When choosing a life insurance policy, it is important to consider factors such as the coverage amount, the type of policy, and the cost of premiums.

| Characteristics | Values |

|---|---|

| Purpose | Financial protection and peace of mind for loved ones |

| Function | Provides a financial safety net for loved ones in the event of the policyholder's death |

| Contract | A legally binding contract between the policyholder and the insurance company |

| Payment | The policyholder pays a premium upfront or regular premiums over time |

| Payout | The insurance company pays a sum of money to the policy's beneficiaries when the policyholder dies |

| Tax | The death benefit is usually tax-free |

| Use of payout | The beneficiaries can use the payout for any purpose, e.g. living expenses, debts, funeral costs, education |

| Types | Term life insurance, permanent life insurance |

| Features | Optional riders, cash value, living benefits |

Explore related products

What You'll Learn

![]()

Replacing lost income

Life insurance is a way to provide financial security for your loved ones after you're gone. One of the most important reasons to get life insurance is to replace the lost income of a family's spouse, parent, or breadwinner. Losing a breadwinner's income can be devastating for a family, and many people don't have enough savings to cover such an event. By purchasing life insurance, you can ensure that your beneficiaries will have the funds to cover expenses and maintain their standard of living.

When determining how much life insurance you need to replace your income, you should consider your annual salary, the number of years you want to cover, anticipated raises, and any additional expenses such as college fees. A common guideline is to multiply your annual salary by the number of years you want to cover. For example, if you earn $60,000 per year and want to provide five years of coverage, you would need a $300,000 policy.

It's also important to include daily tasks in your calculations, such as childcare, cleaning, and cooking. These services can be expensive to replace, and life insurance can help cover the cost of hiring someone to perform these tasks. Additionally, if you have group life insurance through your employer, you may want to include this in your calculations, keeping in mind that this coverage may be tied to your employment.

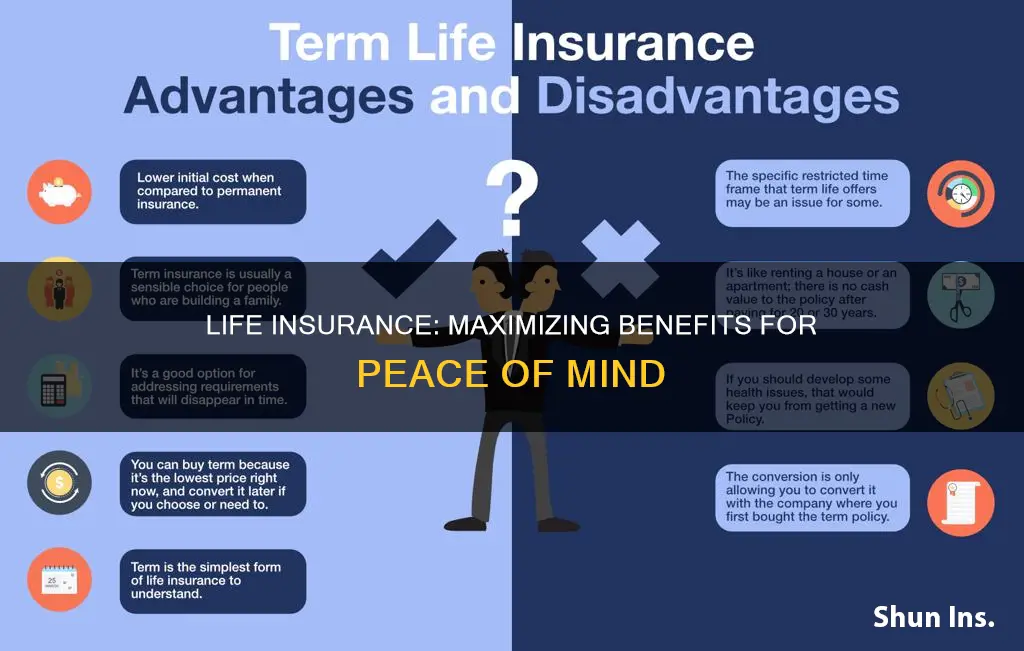

Term life insurance and permanent life insurance are the two main types of life insurance. Term life insurance lasts for a set period, such as 10, 20, or 30 years, and is typically the most affordable option. Permanent life insurance, on the other hand, lasts for the insured's entire life and is more expensive. It often includes a cash value component that can be used for various purposes, such as taking out loans or paying policy premiums.

When choosing a life insurance policy, it's important to consider your income, expenses, and the financial needs of your beneficiaries. By replacing lost income with life insurance, you can ensure that your loved ones will have the financial support they need to maintain their standard of living.

Group Life Insurance: Retirement and Coverage

You may want to see also

Explore related products

![]()

Paying off debts

Life insurance is a useful tool for paying off debts after you die. While your assets will usually be used to pay off your debts, life insurance can help your beneficiaries pay off any remaining balance. This is especially important if you have a co-signer or joint owner of your debt, as they may be held responsible for it after your death.

Types of Debt

There are two main types of debt: secured and unsecured. Secured debt requires an asset as collateral, such as a mortgage or auto loan. If you default on a secured debt, the lender can seize the asset to recoup their costs. Unsecured debt, on the other hand, does not require collateral and is based on the borrower's creditworthiness. Examples of unsecured debt include credit card debt and medical bills.

Life Insurance Options

There are several options for using life insurance to pay off debts. One option is to take out a term life insurance policy, which is designed to last for a set period, such as 10 or 20 years. You can match the term length to the length of the loan, ensuring that your beneficiaries have the financial support they need to pay off the debt.

Another option is to take out a permanent life insurance policy, which lasts your entire life. While these policies are more expensive, they can provide peace of mind knowing that your beneficiaries will receive a payout regardless of when you die.

Additionally, you may consider credit life insurance, which is designed to pay off a borrower's outstanding debts if the policyholder dies. The face value of this type of policy decreases as the loan is paid off over time. However, credit life insurance is typically voluntary and not required by lenders.

Pros and Cons

Using life insurance to pay off debts has several advantages. It can help reduce the financial burden on your loved ones, lower your debt-to-income ratio, and free up money for saving and investing. Additionally, you may be able to pay less interest by paying off the debt sooner. However, there are also some disadvantages to consider. Withdrawing cash from your life insurance policy will reduce the death benefit later on, and you may have to pay surrender fees or taxes on the withdrawn amount.

Alternatives

If you are unsure about using the cash value of your life insurance to pay off debts, there are alternative options available. One option is to take out a debt consolidation loan, which can help you pay off multiple debts with a single loan, making it more manageable. Another option is to open a balance transfer credit card with 0% APR and transfer your current balance to that card. This can save you money on interest, but it is important to repay the balance before the introductory offer expires.

Seeking Expert Advice

When considering your options for paying off debts, it is always a good idea to speak to an insurance or financial expert. They can help guide you toward a plan that aligns with your financial goals and ensure that your loved ones are protected.

Transamerica Life Insurance: Exam Requirements and Health Checks

You may want to see also

Explore related products

![]()

Covering funeral costs

Life insurance can be used to cover funeral costs, which can reach $8,000 for a traditional funeral service. This is a significant expense for loved ones, and life insurance can help ease this burden. Burial insurance, a type of life insurance, can be used to cover funeral and burial expenses. It is a small whole life policy with a death benefit of $5,000 to $25,000. The application process for burial insurance is straightforward and sometimes non-existent. However, these plans usually only pay out a prorated amount based on the premiums paid.

Another option for covering funeral expenses is final expense insurance, which is similar to burial insurance but can be purchased through a funeral home. This type of insurance is designed to cover funeral expenses and may only cover services provided by the specific funeral home. It is important to review the policy details to understand the coverage limitations.

Life insurance payouts do not occur immediately and can take 30 to 60 days or longer, depending on the complexity of the policy. To ensure funds are available when needed, it is essential to plan and set up the policy in advance. Communicating the details of the policy to loved ones is also crucial so that they know what to expect.

To receive a life insurance payout, the beneficiary must submit a claim to the insurance company, along with an official death certificate and other relevant information. The insurance company will then review the claim and determine the total benefit. Advance funding companies are an alternative option for quick access to funds, as they offer policy beneficiaries an advance on their life insurance benefits.

It is important to regularly update and review life insurance policies to ensure adequate coverage. Life events such as marriage, divorce, or retirement should trigger a review of the policy. Additionally, the list of beneficiaries should be routinely checked and adjusted if circumstances change.

Life Insurance Rates: COVID's Impact and Rising Costs

You may want to see also

Explore related products

![]()

Funding children's education

Life insurance can be used to fund your children's education and safeguard their future even in your absence. Here are some ways in which life insurance can help fund your children's education:

Lump-sum Benefit

In the unfortunate event of the policyholder's death within the policy term, a lump-sum benefit is provided to the children, ensuring that their education fund is not compromised and they can continue their education without financial constraints. This benefit can be used to cover tuition fees, books, uniforms, and other educational expenses.

Flexible Payout Options

Child education plans often offer flexible payout options, allowing parents to receive funds during crucial educational milestones, such as college admission. This helps to cover expenses such as tuition fees, room and board, books, and supplies. The payout can also provide extra spending money for the child, even if they plan to pay for their education themselves.

Waiver of Premium

Child education plans may include a waiver of premium benefit, where the insurance company takes over premium payments in the event of the policyholder's untimely death. This ensures that the policy remains active, and the child's educational goals are not disrupted.

Tax Benefits

In many places, such as India, premiums paid towards child education plans may be eligible for tax deductions, and the maturity or death benefit received is often tax-exempt. This helps to maximize returns on investment, allowing parents to save more for their child's education.

Life Cover

Life cover is a crucial component of child education plans, providing a financial safety net for the child in case of the policyholder's untimely demise. It offers a lump-sum payment to the beneficiary (usually the child) to meet their financial needs, including education expenses. This ensures that the child's education is not disrupted and provides peace of mind for the parents.

Investment Flexibility

Child education plans offer investment flexibility, allowing parents to invest at regular intervals or as a one-time contribution. This helps them build a corpus for their child's education over time.

High Returns

Child education plans often provide the dual benefit of insurance and investment, offering the potential for higher returns compared to traditional savings. This can help parents keep up with the rising cost of education.

Inflation Shield

With the cost of education continuing to rise due to inflation, child education plans can help parents stay prepared. The plans enable children to pursue the best courses without financial constraints.

Partial Withdrawals

Child education plans usually allow partial withdrawals after a certain number of years, providing funds for educational milestones such as admission fees, tuition expenses, or educational trips.

Guaranteed Education Benefits

Insurance and savings plans with guaranteed education benefits can help ease financial concerns by growing over time and being used to fund school expenses, including tuition fees, books, transportation, and school supplies.

Long-term Financial Security

Child insurance plans provide long-term financial security for the child, even if the parent is no longer able to provide financial support due to unemployment, sickness, accident, or untimely death.

Beat Inflation

Child insurance plans can help beat inflation through regular investments, ensuring that education costs do not outpace the family's financial capabilities.

Tax-advantaged Growth

The cash value component of life insurance policies can offer tax-advantaged growth, making it appealing to high-income parents who wish to transfer wealth to their children.

Alternative to Student Loans

Life insurance policies can be used as collateral when availing of education loans for children, providing an alternative to taking on student loan debt.

Peace of Mind

By investing in a child education plan, parents can have peace of mind knowing that their child's educational needs will be met, even in their absence. This allows them to focus on other aspects of their lives, such as their careers and families.

Heart Attacks: Accident Insurance Coverage and Definition

You may want to see also

Explore related products

![]()

Covering medical expenses

Life insurance can be used to cover medical expenses, although it is primarily designed to provide financial support to beneficiaries following the death of the insured.

Life insurance policies often include living benefits, which allow the insured to claim against their death benefit and accelerate a portion of it to cover medical costs. This means that the insured can use their death benefit while they are still alive. The death benefit will be reduced by the amount claimed, and the monthly premium will also decrease.

To accelerate the death benefit, the insured must be diagnosed with a qualifying medical condition, such as a heart attack, stroke, or invasive cancer. The insurance company will assess the severity and life expectancy of the insured and make an offer, which can be accepted or rejected.

The money from the accelerated death benefit can be used to pay off hospital bills, health insurance deductibles or co-insurance, or to seek alternative treatment. It is important to note that accelerating the death benefit may have tax consequences, and there may be an administrative charge for processing the claim.

In addition to living benefits, life insurance can also provide coverage for medical expenses through riders, which are add-ons to the policy. Relevant riders include:

- Accelerated death benefit rider: Allows the insured to access a portion of their death benefit if diagnosed with a terminal illness.

- Critical illness death benefit rider: Allows the insured to access a portion of their death benefit if diagnosed with a critical illness.

- Chronic illness death benefit rider: Allows the insured to access their death benefit if they become chronically ill and unable to perform at least two activities of daily living.

- Long-term care rider: Helps cover the costs of long-term care services, such as nursing home care or in-home health care.

While life insurance can be used to cover medical expenses, it is important to note that it is not designed specifically for this purpose. The primary function of life insurance is to provide financial support to beneficiaries following the death of the insured.

Lightning McQueen's Life Insurance: What's the Deal?

You may want to see also

Frequently asked questions

Life insurance is a contract between an insurance company and a policy owner in which the insurer guarantees to pay a sum of money to one or more named beneficiaries when the insured person dies. In exchange, the policyholder pays premiums to the insurer during their lifetime.

Life insurance works by providing a death benefit in exchange for paying premiums. One popular type of life insurance—term life insurance—only lasts for a set amount of time, such as 10 or 20 years. Permanent life insurance also features a death benefit but lasts for the life of the policyholder as long as premiums are paid.

To qualify for life insurance, you need to submit an application. Life insurance is available to almost anyone, however, the cost or premium level can vary based on your age, health, and lifestyle.