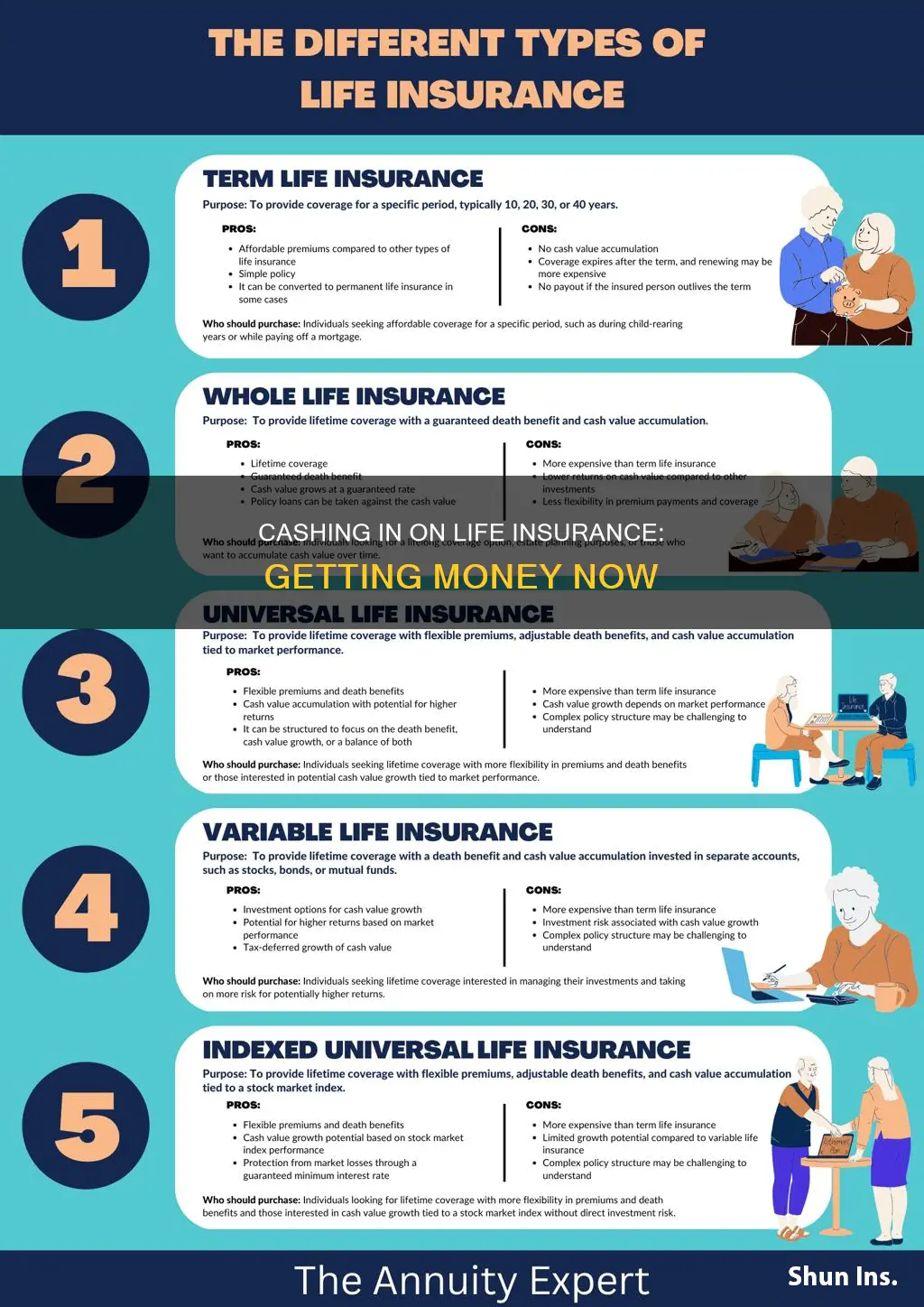

Life insurance is typically taken out to provide financial security for loved ones after the policyholder's death. However, permanent life insurance policies, such as whole life or universal life insurance, can accrue cash value over time, which the policyholder can access while they are still alive. This can be done in several ways, including withdrawing, borrowing, surrendering, or selling the policy. Each option has its own pros and cons, and it's important to carefully consider the potential impact on the death benefit for beneficiaries and any associated fees or tax implications before making a decision.

| Characteristics | Values |

|---|---|

| Options | Withdraw, borrow, surrender, sell |

| Pros | Access cash value, low-interest loan, no loan application or credit check, generally tax-free funds |

| Cons | Reduced death benefit, potential tax liability, surrender fees, reduced cash value, higher tax liabilities, reduced payouts to beneficiaries |

| Who can use this option? | Policyholders with permanent life insurance policies that have had time to build cash value |

| Who cannot use this option? | Policyholders with term life insurance policies |

Explore related products

What You'll Learn

![]()

Withdraw cash from your policy

Withdrawing cash from your life insurance policy is a simple process. All you need to do is contact your insurance company and inform them of the amount you wish to withdraw. They will then wire the cash to you or deposit it into your bank account. This option is usually available after the first two years of the policy.

However, it's important to note that there are some consequences to withdrawing cash from your life insurance policy. Firstly, it may reduce your death benefit, leaving less for your heirs after your death. Secondly, withdrawals above the cost basis may be subject to taxable ordinary income. If the withdrawal exceeds the amount of premiums paid, it may also be taxed as income. Additionally, if your policy is a Modified Endowment Contract (MEC), withdrawals are treated as gains first and are subject to ordinary income taxes. If you are under 59 ½ years old, you may also have to pay a 10% federal tax penalty on taxable withdrawals.

It's also worth considering the alternatives to withdrawing cash from your life insurance policy, such as borrowing against the policy or surrendering it. Borrowing against your life insurance policy can provide you with funds at a lower interest rate than a personal loan, and you don't have to go through a loan application or credit check. On the other hand, surrendering your policy will result in a lump sum payment, but you will lose your coverage and your beneficiaries will not receive a death benefit.

Becoming an Independent Health and Life Insurance Agent

You may want to see also

Explore related products

$15.95

$2.99 $12.95

![]()

Take a loan from your policy

Borrowing from your life insurance policy can be a quick and easy way to get cash. However, there are some important considerations to keep in mind. Here are four to six paragraphs on taking a loan from your life insurance policy:

If you have a permanent life insurance policy with a cash value component, you can take out a loan from your life insurance company. This means using the cash value of your policy as collateral. There is no approval process or credit check, and you can use the money for any reason. The only requirement is that you have sufficient cash value built up in your policy, and the minimum amount varies by insurer. It's important to note that borrowing against your life insurance policy is not risk-free. If you don't pay back the loan, it may reduce your death benefit or cost you your policy.

The limit for borrowing money from your life insurance policy is typically set by the insurer, and it's usually no more than 90% of the policy's cash value. Interest rates for life insurance loans are generally lower than those for personal loans or credit cards, ranging from 5% to 8%. There is no strict repayment schedule, but it's in your best interest to pay back the loan as soon as possible to minimise the interest you'll owe. If you don't make regular payments, your policy could lapse, especially if the amount you owe exceeds the policy's cash value.

If you pass away with an outstanding loan on your life insurance policy, the insurer will deduct the amount owed, including any interest, from your death benefit. This means your beneficiaries will receive a reduced payout. Additionally, if you don't repay the loan or your policy lapses, you may owe taxes on the amount you borrowed. It's important to speak with a financial advisor to understand the tax implications before taking out a loan against your life insurance policy.

Life insurance loans can be a convenient way to access cash, especially if you need money quickly. They offer low-interest rates, flexible repayment options, and no impact on your credit score. However, it's important to weigh the benefits against the potential drawbacks, such as reduced death benefits and the risk of policy lapse.

Overall, taking a loan from your life insurance policy can be a viable option if you need quick access to cash and are comfortable with the potential risks and implications. Be sure to carefully review the terms and conditions of your policy and consult with a financial professional before making any decisions.

GSK Retirement Benefits: Life Insurance Coverage Explained

You may want to see also

Explore related products

![]()

Surrender your policy

Surrendering your life insurance policy means cancelling your coverage in exchange for a lump sum. This is a good option if you no longer need the policy or you need money quickly.

When you surrender your policy, you are agreeing to take the cash surrender value assigned to it by the insurance company. In return, you forgo the death benefit. Whole and universal policies accrue cash value, making them the most likely option for surrender. Depending on the type and age of the policy, they may have accrued a significant amount of cash value.

The cash surrender value is the money a life insurance policyholder receives for ending their coverage before the maturity date or before they pass away. This can be appealing if you no longer need the coverage to pay off outstanding debts like a mortgage or other loans. Surrendering your policy can also help if you can no longer afford the premiums.

There are a few things to consider before surrendering your life insurance policy. Firstly, if your policy isn't very old, you may incur surrender fees, which will reduce the amount of cash you receive. Secondly, the gain on your policy will be taxed as income. Death benefits are tax-exempt, but the cash you receive from surrendering is taxable. Finally, surrendering your policy means your beneficiaries will no longer receive a death benefit.

There are generally no restrictions on when you can surrender a life insurance policy, as long as you've made it through the surrender period. This period varies by policy and could be a couple of years to over 15 years. After the surrender period, the timing depends on your personal preference and financial situation. However, most policies require you to pay surrender fees when surrendering, and these fees often decrease over the policy's life. So, the longer you wait, the less you'll likely pay in surrender fees.

Most life insurance companies make it straightforward to surrender your policy. You'll need to contact your insurance company or agent, and you may have to sign paperwork to confirm the surrender. Once the process is in motion, the insurance company will handle the details of calculating your final payout. This amount is usually your cash value balance minus any surrender fees or outstanding loans on your policy.

ACA and Pre-Existing Conditions: Life Insurance Impact

You may want to see also

Explore related products

![]()

Sell your policy

Selling your life insurance policy is a big decision and it's important to understand the implications for your finances and beneficiaries. Carefully consider your options to figure out which, if any, is the best way to use your policy while you're alive.

Selling your life insurance policy is also known as a life settlement. This is when you sell your policy to a third party for a lump sum that is greater than the cash value. The transaction is often called a life settlement. Although you’ll continue making premium payments on the policy, if you die, the death benefit will go to the third party.

You can sell your life insurance policy to a life settlement broker or directly to a life settlement provider. A broker will shop your policy around to get you the best deal, but they will take a cut of the final sum.

Who can sell their policy?

Generally, you can sell both term and permanent life insurance policies, provided you are 65 or older or suffering from a serious illness that could soon take your life. But only term life policies that can be converted to permanent can be sold. Many policies have such convertibility, though it might be limited in time – such as only within the first five years of owning the policy.

The value you can get from selling a term life insurance policy depends on a number of factors:

- The way you sell the policy. Selling a life insurance policy to a settlement company may get you more money than taking the cash surrender value from the insurer.

- Age. The older you are, the higher the offer will be, as you are more likely to die compared with younger policyholders.

- Health status. The lower your life expectancy, the higher the offer will be, as the buyer will profit sooner from the sale.

- The premiums you’re paying. The lower the premium amounts, the higher the offer, as the settlement company won't have to pay as much monthly to maintain the policy.

- The policy’s death benefit. A higher death benefit makes the policy more valuable to the buyer.

The payment you receive from selling your life insurance could be taxable as income or capital gain, depending on your circumstances. If it's taxable, you'd have to include the difference between how much you paid for the policy and how much you sold it for in your annual income.

Life insurance settlement commissions can be as high as 30% of the purchase price, so more than taxes can take a bite out of the proceeds from selling your life insurance policy.

Selling a life insurance policy could lead to a lower or no payout for your beneficiaries when you pass away. The money from the policy would instead go to the new owner. If your beneficiaries planned to use the life insurance payout to cover specific costs like mortgage or funeral expenses, selling the policy could leave them struggling to meet those financial needs.

Alternatives to selling your policy

There are alternatives to selling your life insurance policy that might suit your needs better, including:

- Policy loans: If you have permanent coverage, you can borrow money from your life insurance policy's cash value. Such a loan doesn't involve selling the policy and, provided the money is repaid, can allow you access to funds without impacting your beneficiaries.

- Partial surrender: You can withdraw a portion of your policy's cash value while keeping the coverage intact. This allows you to access funds without completely giving up your life insurance protection.

- Accelerated death benefits: If you're facing a terminal illness, you might be eligible to receive a portion of the death benefit early. This can provide financial relief during challenging times without selling the policy.

- Conversion to a paid-up policy: This allows you to eliminate continuing to pay for a life insurance policy and get a break on your financial obligations.

Variable Life Insurance: Does It Expire?

You may want to see also

Explore related products

$16.53 $22.99

![]()

Use your policy's living benefits

Living benefits are riders on life insurance policies that allow you to access a portion of the death benefit early if you're diagnosed with a terminal illness and have a life expectancy of one year or less. Living benefit riders may provide up to 50% of the death benefit in advance, which can be used to cover medical costs for your care. Some life insurance policies include living benefit riders as standard with no additional costs, while others offer them as an optional add-on for a fee.

- Terminal illness: If you are given a terminal diagnosis with a life expectancy of six months to two years (the exact timeline depends on the insurer), you can use this rider to cover end-of-life care and other associated expenses.

- Chronic illness: This rider applies if you're diagnosed with a chronic illness that prevents you from performing at least two of the six "activities of daily living" (ADLs), which include bathing, eating, getting dressed, toileting, transferring, and continence.

- Critical illness: You can also access living benefits with a critical illness rider, which covers qualifying illnesses that shorten life expectancy and have high medical costs. Examples include heart attack, stroke, and kidney failure.

- Long-term care: This rider allows you to access living benefits if you need to pay for long-term care services and you can't perform at least two of the activities defined under ADL guidelines.

To access living benefits, you will need to submit a claim to your insurance company along with medical records and other relevant documentation. You may receive living benefits as a lump sum or on an as-needed basis. Typically, you're limited in how much you can withdraw to a certain percentage or dollar amount of your policy's death benefit, such as 80%.

Life Insurance and Food Stamps: Is There a Link?

You may want to see also

Frequently asked questions

There are four main ways to cash in your life insurance policy: borrow, withdraw, surrender, or sell.

Borrowing from your life insurance policy can be a fast and easy way to get cash. The interest rates are typically lower than on other types of loans, and there is no loan application or credit check. However, the loan will accrue interest and reduce your death benefit, meaning your beneficiaries will receive less.

Withdrawing cash from your life insurance policy is likely the easiest and fastest way to access the cash. The money you take out is also tax-free up to the amount of premiums you've paid. However, withdrawing cash will reduce your death benefit and may be subject to tax if it exceeds the amount of premiums paid.

Surrendering your life insurance policy will get you a lump sum payment. However, you will have to pay surrender fees and income tax on any earnings, and your beneficiaries will not receive a death benefit.

Selling your life insurance policy will get you a lump sum payment and you will no longer have to pay premiums. However, your heirs will not receive a death benefit, you may owe taxes on the sale, and the proceeds may disqualify you from certain programs such as Medicaid.