Life insurance is a contract between you and a life insurance company. By comparing quotes and plans, you can find the best option for your needs and budget. The two main types of life insurance are permanent life insurance and term life insurance. Permanent life insurance provides coverage for your entire life, while term life insurance only covers you for a fixed term. When deciding which type of insurance to choose, consider your age, health, budget, and financial obligations.

| Characteristics | Values |

|---|---|

| Type of Insurance | Permanent Life Insurance, Term Life Insurance, Whole Life Insurance, Universal Life Insurance, Variable Universal Life Insurance, No-Medical-Exam Life Insurance, etc. |

| Coverage | $50,000 to $25,000,000 |

| Age | 18-85 |

| Gender | Male, Female |

| Health | No pre-existing conditions, overweight, smoker, etc. |

| Lifestyle | Heavy drinker, extreme sports enthusiast, etc. |

| Dependents | Spouse, children, family member, etc. |

| Budget | Varies depending on the type of insurance |

| Reviews | Varies depending on the insurance company |

Explore related products

What You'll Learn

![]()

Whole life insurance vs. term life insurance

When comparing life insurance plans, it's important to consider your budget, time frame, and whether you want a savings component included in your policy. Term life insurance and whole life insurance are the two main types of life insurance policies.

Term Life Insurance

Term life insurance provides coverage for a set period, typically between 10 and 30 years, or until a specific age. It tends to be cheaper than whole life insurance because it does not have a cash value component, and there is no payout if the policyholder outlives the term. Term life insurance is usually chosen by those who only need coverage for a specific period, such as the length of their mortgage. It is also a good option for those who want affordable coverage or are considering converting to whole life insurance in the future.

Whole Life Insurance

Whole life insurance, on the other hand, provides coverage for the entire life of the policyholder. It tends to be more expensive because it serves as an investment and has a cash value component that grows tax-free over time. The cash value can be borrowed against or withdrawn, providing financial flexibility. Whole life insurance is often chosen by those who want lifelong coverage, are able to afford the higher premiums, and want to build guaranteed cash value.

Key Differences

| Term Life Insurance | Whole Life Insurance |

|---|---|

| Set time period (e.g., 10, 20, or 30 years) | Coverage until a set age (e.g., 95 or 100) |

| No cash value | Cash value grows at a guaranteed rate |

| Cheapest type of life insurance | Significantly more expensive |

COPD and Life Insurance: What's the Deal?

You may want to see also

Explore related products

![]()

Permanent life insurance

One of the main differences between permanent and term life insurance is the cash value component of a permanent life insurance policy. The policy's value increases with each premium payment, and this money can be paid out to the policyholder if the contract is cancelled. Additionally, the money can be used as collateral for a loan, which is not possible with term life insurance.

There are several types of permanent life insurance policies, including:

- Whole life insurance: This is a common type of permanent life insurance that offers coverage for the policyholder's entire life. It builds cash value in a secure account and has regularly scheduled premiums to keep the policy active.

- Universal life insurance: Universal life insurance allows for more flexibility, as premium payments can be adjusted over time. However, this may negatively impact the cash value of the plan and cause premiums to increase in the long run.

- Variable universal life insurance: This type of insurance has flexible premiums and a savings component, but more factors influence how the savings can grow. The savings portion, or cash value, grows based on the investment methods chosen by the policyholder.

- Indexed universal life insurance: This type of policy is similar to a permanent life insurance policy, but the cash value grows based on a chosen stock market index. If the chosen index performs well, the account will grow; otherwise, some companies allow it to grow at a minimum rate.

The cost of permanent life insurance depends on various factors, including age, medical history, family size, and location. It is typically more expensive than term life insurance due to its lifelong coverage and investment opportunities.

Life Insurance: Does Age Affect Payout Value?

You may want to see also

Explore related products

![]()

Universal life insurance

One of the key features of universal life insurance is its flexibility in paying premiums. You can choose how much to pay and when to pay, as long as there is enough cash value to cover the policy's monthly fees. The cash value of the policy earns interest, and you can borrow against it or use it as collateral for a loan. However, if you borrow against the cash value, interest will be charged, and any unpaid amounts may reduce the death benefit. Additionally, some withdrawals from the policy may be taxable.

When comparing universal life insurance policies, it's essential to consider your long-term goals and financial situation. Universal life insurance may be suitable for those who want flexible premiums, a savings component, and lifelong coverage. However, it's important to carefully manage the cash value and monitor the interest rates to avoid large payment requirements or policy lapse.

Overall, universal life insurance offers flexibility and lifelong protection, making it a valuable option for individuals who want to ensure their loved ones are protected and have access to additional financial resources.

Heart Attacks: Accident Insurance Coverage and Definition

You may want to see also

Explore related products

![]()

Average life insurance rates

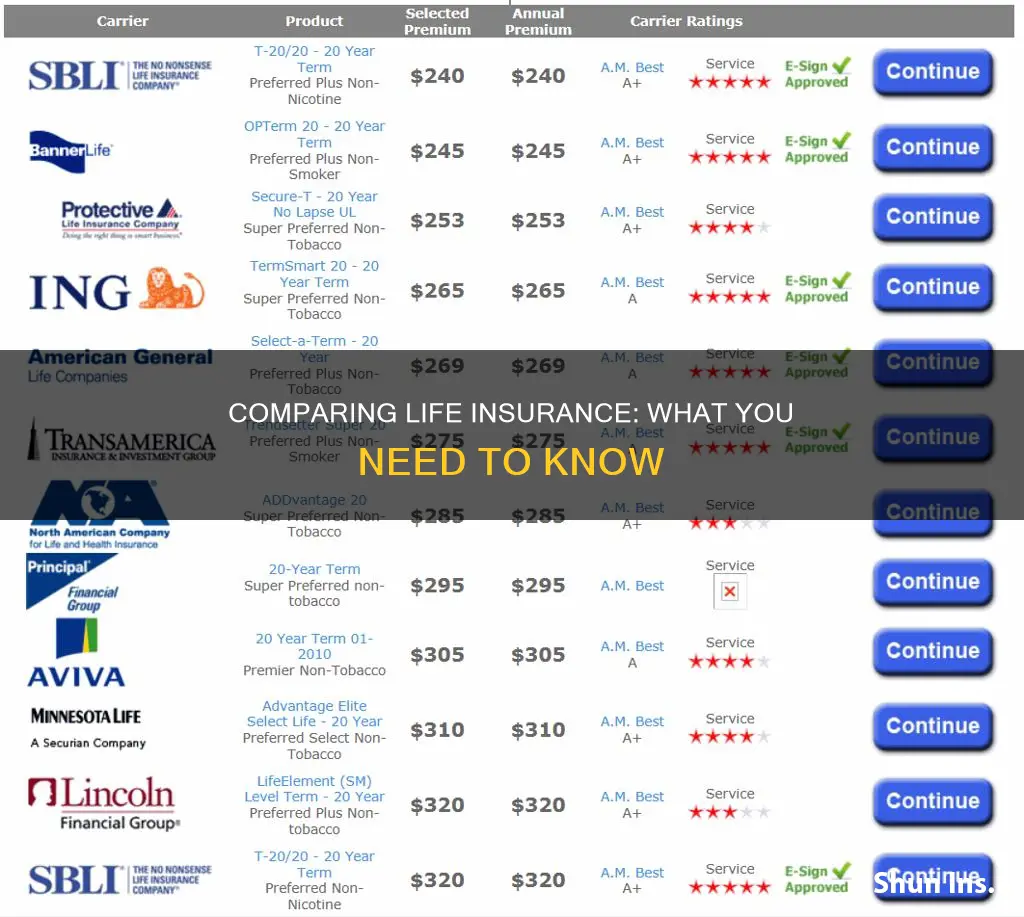

The average cost of life insurance is $26 a month, based on a 40-year-old buying a 20-year, $500,000 term life policy. However, life insurance rates can vary dramatically among applicants, insurers, and policy types. The cost of life insurance depends on multiple factors, such as age, gender, health, and lifestyle.

Age

Generally, younger people pay less for life insurance because the likelihood of death and serious illnesses is much lower. The longer you wait to buy life insurance, the more your rates will increase based on age alone.

Gender

Because women have longer life expectancies, they will almost always pay less than men of the same age and health.

Health

Insurers will look at any pre-existing conditions, as well as your blood pressure and cholesterol levels. They will also consider your height and weight.

Lifestyle

Smokers and heavy drinkers incur expensive premiums due to the increased risk of cancer and other related diseases.

Driving Record

If you have DUIs, DWIs, and major traffic violations on your record, your insurer might consider you a high-risk applicant and charge higher rates.

Occupation and Activities

If you have a hazardous or high-risk job, such as a police officer or race car driver, you can expect to pay more than someone with a desk job. Similarly, if you participate in risky activities like skydiving, you might be charged a higher premium.

Type of Life Insurance

Term life insurance is the least expensive because it lasts a set number of years and does not build cash value. Permanent life insurance, on the other hand, typically lasts a lifetime and includes a cash value component, making it substantially more expensive than term life insurance.

Life Insurance and PNC Bank: What You Need to Know

You may want to see also

Explore related products

![]()

Life insurance for people with pre-existing conditions

A pre-existing condition is a medical issue that has been diagnosed or treated before applying for an insurance policy. While it doesn't disqualify you from getting life insurance, it can make your search for a quote more challenging and expensive. The impact of a pre-existing condition on your life insurance premium depends on its severity. The more severe the condition, the more you can expect it to impact your premium.

Types of Life Insurance for People with Pre-Existing Conditions

Term Life Insurance

Term life insurance policies have more affordable premiums and large death benefits, but coverage only lasts 10 to 30 years. This type of policy may be suitable if you want the most coverage for your budget.

Guaranteed Issue Life Insurance

A guaranteed issue life insurance policy never denies applicants. There are no medical questions or exams, but the coverage is limited, and the premiums are higher. This type of policy guarantees acceptance as long as you are within a certain age range.

Group Life Insurance

Group life insurance is a term life insurance policy offered by some employers as part of their benefits package. Employers tend to offer limited coverage, usually not more than $50,000 in death benefits, but the premiums can be favourable and easy to manage.

Whole Life Insurance

People with pre-existing conditions could still qualify for whole life insurance, but the premiums can be much higher. This type of insurance lasts for the person's entire life and offers a cash value growth component, allowing the policyholder to build wealth.

Tips for Buying Life Insurance with a Pre-Existing Condition

- Stick to your treatment plan: Demonstrating adherence to your treatment plan shows the insurer that you are managing your condition. Provide proof of regular visits to your healthcare provider, taking prescribed medication, and following medical advice.

- Exercise regularly: Regular exercise keeps you healthy and can reduce the risks or symptoms associated with your pre-existing condition. Evidence of regular exercise can convince an insurer that you are managing your health.

- Lose weight if overweight: Losing weight can increase your chances of approval if it helps you achieve a healthy weight, leading to positive health effects such as reduced blood pressure and better blood sugar control. However, being underweight can also lead to health risks that may affect approval.

- Shop around for insurance: Insurance coverage costs and terms can vary between insurers. Shopping around can help you find insurers willing to offer coverage despite pre-existing conditions and allow you to compare quotes to choose the best rates and terms.

- Apply for coverage earlier in life: Life insurance typically becomes more expensive as you get older. Applying for coverage earlier in life, such as in your 20s or 30s, can help lock in more affordable rates for a longer period.

- Share improvements in your health: Communicate any improvements in your health to your insurer. They may adjust your premium if they see that your health condition has improved or been eliminated.

- Be honest about your condition: Lying about or omitting information regarding your pre-existing condition on your application can lead to serious consequences, including policy cancellation, claim denial, or being recorded in the MIB Group insurance database, which may hurt your chances with other insurers.

What to Do if You've Been Denied Life Insurance Coverage

- Wait and re-apply after your condition improves: Focus on following your treatment plan, exercising regularly, and maintaining a healthy lifestyle. Document your health improvements and consider re-applying after a significant period, as insurers prefer to see a longer history of improvements.

- Appeal the denial: In some cases, denials may be due to errors or missing medical information. Provide correct and additional evidence to support your case and reduce your perceived risk.

- Work with an insurance broker: Brokers specialise in helping clients find life insurance and are incentivised to work hard on your behalf.

- Explore guaranteed issue life insurance: Guaranteed issue life insurance approves all applicants, with no exams or medical questions. Consider this option if the smaller death benefit and cash value component suit your needs.

Life Insurance and Drug Use: What's the Verdict?

You may want to see also

Frequently asked questions

You can get a life insurance quote online or by phone. You will need to provide some personal details such as your age, health, and the type of coverage you require.

This will depend on your financial obligations and resources. You should consider any debts, mortgage payments, income replacement needs, and funeral costs. You should also take into account any existing life insurance coverage you may have.

There are two main types of life insurance: Permanent Life Insurance and Term Life Insurance. Permanent life insurance provides coverage for your entire life, while term life insurance only provides coverage for a specific period. You should choose the type of plan that best suits your needs.