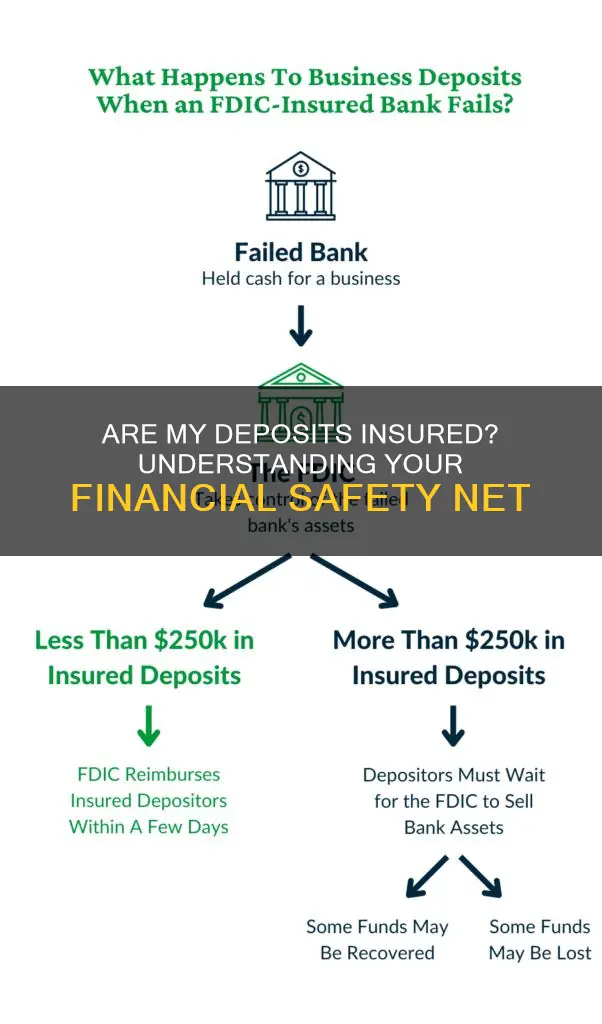

It is important to know whether your deposits are insured by the Federal Deposit Insurance Corporation (FDIC) in case your bank fails. The FDIC's deposit insurance covers checking accounts, savings accounts, and certificates of deposit (CDs), up to $250,000 per depositor, per account type, per institution. To check if your deposits are insured, you can use the FDIC's online Electronic Deposit Insurance Estimator, call the FDIC at 1-877-275-3342, or look for official FDIC signage at banking locations.

| Characteristics | Values |

|---|---|

| How to check if deposits are insured | Use the Federal Deposit Insurance Corporation's (FDIC) online Electronic Deposit Insurance Estimator, call the FDIC at 1-877-275-3342, or look for official FDIC signage at banking locations |

| Deposit insurance coverage | $250,000 per depositor, per account type, per institution; $500,000 for joint accounts; $1,250,000 for trust accounts |

| What is covered | Checking accounts, savings accounts, retirement accounts, certificates of deposit (CDs), money market deposit accounts (MMDAs) |

| What is not covered | Investments (e.g. stocks, bonds, mutual funds, crypto), lost or stolen prepaid cards, prepaid card provider bankruptcy |

Explore related products

What You'll Learn

![]()

Using the Federal Deposit Insurance Corporation's (FDIC) online tools

The Federal Deposit Insurance Corporation (FDIC) provides several online tools and resources to help individuals determine if their deposits are insured and understand the extent of their deposit insurance coverage. Here are some key tools provided by the FDIC:

Electronic Deposit Insurance Estimator:

The FDIC offers an online Electronic Deposit Insurance Estimator on its website. This tool allows individuals to input information about their deposit accounts and determine if their deposits are insured by the FDIC. It provides an estimate of the coverage based on the account type, balance, and other factors. This estimator helps individuals understand if their deposits are within the FDIC insurance limits.

Bank Find Website:

The FDIC also provides a "Bank Find" website or tool, which allows individuals to verify if their bank or savings association is FDIC-insured. By using this tool, individuals can confirm that their financial institution is backed by FDIC deposit insurance. This tool can provide peace of mind and assurance that deposits are protected.

Online Resources and FAQs:

The FDIC website offers extensive online resources, including frequently asked questions (FAQs) about deposit insurance coverage. These resources cover a range of topics, such as finding insured banks, understanding deposit account types, and explaining the FDIC's role in the event of bank failure. The FAQs provide clear and detailed information to help individuals navigate the complexities of deposit insurance.

Webinars and Training Programs:

In addition to its online tools, the FDIC hosts educational webinars and provides training programs for bankers. These webinars cover a range of topics, from basic deposit insurance information to advanced insurance topics. By participating in these webinars, individuals can enhance their understanding of deposit insurance and make more informed decisions about their financial choices.

Toll-Free Telephone Support:

While not strictly an online tool, the FDIC also offers a toll-free telephone number, 1-877-275-3342 (1-877-ASK-FDIC), where individuals can call to determine their deposit insurance coverage. This support line allows individuals to ask specific questions and receive personalized assistance in understanding their deposit insurance.

By utilizing these online tools and resources provided by the FDIC, individuals can confidently assess whether their deposits are insured and gain a clearer understanding of their financial protection. These tools empower people to make informed decisions and ensure the safety of their hard-earned money.

Social Insurance Programs: A Safety Net

You may want to see also

Explore related products

![]()

Calling the FDIC

If you're unsure whether your deposits are insured, one option is to call the FDIC. Here's some information to guide you through the process:

When calling the FDIC, you can inquire about deposit insurance coverage and ask questions regarding your specific account or financial institution. The FDIC can provide you with accurate and up-to-date information on insurance limits, coverage rules, and any changes or updates to their policies. They can also clarify any doubts you may have about the insurance status of your deposits.

To effectively communicate your concern, be prepared to provide specific details about your account and financial institution. Have the following information ready before placing the call:

- Account Information: Know your account type (checking, savings, certificate of deposit, etc.) and the balance of your deposits.

- Financial Institution Details: Have the name, location, and FDIC certificate number of your bank or financial institution. You can find the FDIC certificate number on your bank statements or by searching the FDIC's BankFind database.

- Personal Information: Be ready to provide your name, contact information, and any other relevant details that may be requested to verify your account or ownership of the deposits.

When you call the FDIC, follow these steps to ensure a smooth process:

- Dial the FDIC's Consumer Hotline: The FDIC can be reached at 1-877-ASK-FDIC (1-87Rkthe FDIC32). This hotline is specifically designated for consumers with questions or concerns about deposit insurance.

- Provide Necessary Information: When connected, explain the nature of your call and provide the account and financial institution details you've prepared. Be as specific as possible to facilitate a quick and accurate response.

- Ask Questions and Clarifications: Don't hesitate to ask questions and seek clarifications on any aspect of deposit insurance that you're unsure about. The FDIC representatives are there to provide you with accurate and reliable information.

- Take Notes: During the call, take notes on the responses and any important information provided by the FDIC representative. Note down dates, names, reference numbers, or any other relevant details mentioned during the conversation.

- Follow Up, if Needed: In case your inquiry is complex or requires further investigation, the FDIC may need additional time to provide a comprehensive response. Take note of the expected response time and the appropriate contact information for following up on your inquiry.

Remember, the FDIC is a reliable source of information regarding deposit insurance. Their representatives are knowledgeable and can provide you with accurate guidance on insurance coverage and limits. Don't hesitate to call them if you have any doubts or concerns about the safety of your deposits.

The Insurance Conundrum: Paid in Full, Yet Bills Remain

You may want to see also

Explore related products

![]()

Looking for FDIC signage at banking locations

The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance for checking accounts, savings accounts, certificates of deposits, and more. The FDIC insurance limit is $250,000 per depositor, per account type, per institution.

There are a few ways to check if your bank is FDIC-insured. One way is to look for official FDIC signage at banking locations. The FDIC provides official teller signage to financial institutions whose deposits are insured. These signs are provided as decals that can be affixed to hard surfaces and plastic counter signs. The FDIC encourages all insured depository institutions to post these signs to increase depositor awareness of the deposit insurance coverage. Banks can order these signs through the FDIC Online Catalog, and they can also request an electronic image of the official teller sign by faxing or emailing a request using bank letterhead. The FDIC has also extended the compliance date for the new signage and advertising rule to May 1, 2025, to give financial institutions more time to implement the new requirements.

The FDIC official sign, with its black and gold design, has been displayed at bank branch teller windows since the 1930s and has given bank customers confidence that their deposited funds are safe. The official sign must be displayed continuously, clearly, and conspicuously, ensuring that it is large enough to be legible. This requirement also applies to ATMs that receive deposits, and the FDIC provides flexibility for ATMs that do not offer access to non-deposit products.

In addition to looking for FDIC signage at banking locations, you can also use the FDIC's Bank Find website or call the agency at 1-877-275-3342 (1-877-ASK-FDIC) to determine your deposit insurance coverage.

Understanding Transamerica's Annual Renewable Term Life Insurance: Flexibility and Protection

You may want to see also

Explore related products

$51.19 $63.99

![]()

Checking if your bank is insured

It is essential to know if your bank is insured to protect your money in the event of a bank failure. The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance to protect your money in such cases. FDIC insurance covers all deposit accounts at insured banks up to a limit of $250,000 per depositor, per bank, and per ownership category. This includes the principal and any accrued interest through the date of an insured bank's closing.

To check if your bank is FDIC-insured, you can use the FDIC's Bank Find website or its online Electronic Deposit Insurance Estimator. The FDIC also provides a toll-free number, 1-877-275-3342 or 1-877-ASK-FDIC, which you can call to determine your deposit insurance coverage or ask any specific deposit insurance questions. Additionally, you can look for official FDIC signage at banking locations.

It is important to note that FDIC insurance does not cover all types of accounts or investments. While it covers checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs), it does not insure investment products such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities. Therefore, it is crucial to understand what is and isn't covered by FDIC insurance and to review your account balances and the applicable FDIC rules.

In summary, by using the FDIC's online tools or contacting them directly, you can easily check if your bank is FDIC-insured. However, it is also important to understand the coverage limits and exclusions to ensure your deposits are adequately protected.

Taiwan: Nearly Universal Health Insurance Coverage

You may want to see also

Explore related products

![]()

Understanding the deposit insurance coverage limit

The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance for checking accounts, savings accounts, certificates of deposit (CDs), and more. FDIC insurance is automatic for eligible accounts at FDIC-insured banks, and there is no need to apply for it separately. The standard deposit insurance amount is $250,000 per depositor, per FDIC-insured bank, per ownership category. This limit applies to various account types, including single accounts, joint accounts, retirement accounts, and trust accounts.

For single accounts, the FDIC insurance covers up to $250,000 per depositor, per bank, regardless of the number of accounts held by the same person at the same bank. This includes accounts with no beneficiaries, such as those held in one person's name only or established for a minor by a guardian.

In the case of joint accounts, the coverage limit can double to $500,000, assuming the account meets certain requirements. Each co-owner's share of the account is insured up to $250,000.

Retirement accounts, such as IRAs and 401(k)s, are also covered up to $250,000 per owner, per bank. This includes accounts where the owner has the right to direct how the money is invested.

Trust accounts, including both revocable and irrevocable trusts, have a more complex calculation. The FDIC uses the formula: Number of Owners x Number of Beneficiaries x $250,000, with a maximum of $1,250,000 per owner for all trust accounts combined.

It is important to note that FDIC insurance does not cover all financial products offered by banks. For example, investments in stocks, bonds, mutual funds, and cryptocurrency are not insured. Additionally, FDIC insurance only applies if the bank fails; it does not cover lost or stolen funds or if the bank declares bankruptcy.

VA Insurance: Millions Covered

You may want to see also

Frequently asked questions

Your deposits are insured only if your bank has Federal Deposit Insurance Corporation (FDIC) deposit insurance. You can use the FDIC's online Electronic Deposit Insurance Estimator to find information about your insured deposits. You can also call the FDIC at 1-877-275-3342 or look for official FDIC signage at banking locations.

The standard deposit insurance amount is \$250,000 per depositor, per FDIC-insured bank, per ownership category. If you open a joint account with your spouse, the coverage limit doubles to \$500,000, assuming the account meets several requirements.

FDIC deposit insurance covers checking accounts, savings accounts, certificates of deposit (CDs), retirement accounts, and more. FDIC insurance covers traditional deposit accounts, but it does not cover your investments in things like stocks, bonds, mutual funds, and crypto.

You can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool.