Mortgage insurance protects the lender if the buyer stops making loan payments. It is usually required when homebuyers make a down payment of less than 20% of the home's value. The cost and other details vary by the type of loan. If you get a conventional loan, your lender could arrange mortgage insurance with a private company. Private mortgage insurance (PMI) rates vary by down payment amount and credit score but are generally cheaper than FHA rates for borrowers with good credit. Most private mortgage insurance is paid monthly, with little or no initial payment required at closing.

| Characteristics | Values |

|---|---|

| Who does mortgage insurance protect? | The lender, not the borrower. |

| When do you need to pay for mortgage insurance? | When you put down less than 20% of the purchase price of the home. |

| What type of insurance is it? | Private Mortgage Insurance (PMI) or Mortgage Insurance Premium (MIP). |

| How much does it cost? | Between 0.58% and 1.86% annually, or between 1% and 3% of the home's purchase price. |

| How do you pay? | Monthly, included in your mortgage payment. Or, in a lump sum at the start of the loan. |

| Can you avoid it? | Yes, if you put down a payment of 20% or more. |

| Can you cancel it? | Yes, once you've paid off more than 20% of the loan. |

| What about Federal Housing Administration (FHA) loans? | FHA loans require mortgage insurance, which is paid to the FHA. |

| What about U.S. Department of Agriculture (USDA) loans? | USDA loans are similar to FHA loans but typically cheaper. |

| What about Department of Veterans' Affairs (VA)-backed loans? | VA-backed loans do not require monthly mortgage insurance, but you pay an upfront "funding fee". |

Explore related products

$4.99 $14.99

What You'll Learn

![]()

Private mortgage insurance (PMI)

You can pay PMI with a one-time upfront premium at closing, or through both upfront and monthly premiums. The upfront premium is shown on your Loan Estimate and Closing Disclosure, while the monthly premium is included in your monthly mortgage payment. Lenders may offer multiple PMI options, so it is recommended to ask the loan officer to help you calculate the total costs and compare different options to find the best deal.

PMI can help you qualify for a loan that you may not otherwise be eligible for, but it increases the cost of your loan. You can request to cancel PMI when your mortgage balance reaches 80% of your home's value, or when you are halfway through your loan term. Federal law dictates that your mortgage lender must automatically end your PMI when your LTV ratio drops to 78% or when you are one month past the midpoint of your loan term.

To avoid PMI, you can consider saving up to make a 20% down payment, or look for a more affordable property where you can make a 20% down payment.

Reporting a House Break-In: When to Involve Insurance

You may want to see also

Explore related products

![]()

Conventional loans

When it comes to purchasing mortgage insurance for a conventional loan, there are a few things to keep in mind. Firstly, mortgage insurance, typically in the form of Private Mortgage Insurance (PMI), is usually required when the buyer makes a down payment of less than 20% of the home's value. This is because lenders consider low down payments to be riskier, and they want financial protection in case of foreclosure. PMI rates vary based on the down payment amount and credit score but are generally cheaper than FHA rates for borrowers with good credit.

However, some lenders may waive the PMI requirement if you agree to pay a higher interest rate or opt for an alternative financing package. Additionally, there are lenders who require mortgage insurance regardless of the loan amount, while others may offer loans up to a certain amount without needing mortgage insurance. Therefore, it is essential to understand your lender's specific policies and criteria.

If you opt for a conventional loan, your lender will typically arrange for mortgage insurance with a private company. Most PMI is paid monthly, with little to no initial payment required at closing. It is important to note that PMI protects the lender, not the borrower, in the event of missed loan payments.

There are ways to avoid paying PMI. One way is to make a 20% down payment, which can be challenging to save for. Another option is to explore alternative loan types, such as VA loans, which do not require PMI. Additionally, once your loan balance reaches 78% of the original value, you may be able to cancel your PMI.

Lucrative Rewards: Unveiling the Winner's Purse at the Farmers Insurance Tournament

You may want to see also

Explore related products

![]()

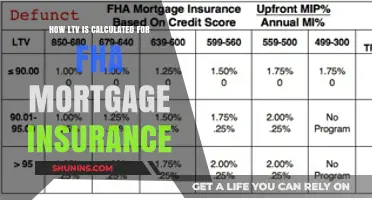

Federal Housing Administration (FHA) loans

FHA loans require mortgage insurance, which is paid to the FHA. This insurance includes an upfront cost, paid as part of the closing costs, and a monthly cost included in the monthly payment. Borrowers can choose to roll the upfront fee into their mortgage, but this increases the loan amount and overall costs. FHA mortgage insurance is mandatory for all FHA loans, and the cost is the same regardless of credit score, with a slight increase for down payments of less than 5%.

To qualify for an FHA loan, borrowers must meet certain criteria. A minimum down payment of 3.5% of the purchase price is required, though this can be as low as 3.5% with a higher credit score. Lenders will also ask for evidence of recent and steady employment, with tax returns and pay stubs as documentation. The total mortgage payments, property taxes, insurance premiums, and any association fees must generally be less than 31% of the borrower's gross income (known as the front-end ratio). Additionally, the mortgage payment and all other monthly consumer debts (the back-end ratio) should be less than 43% of the gross income.

FHA loans provide an opportunity for homebuyers who might otherwise struggle to obtain a loan to achieve homeownership. By insuring the loan, the FHA reduces the risk to lenders and makes it more accessible for borrowers to get approved.

Disability Insurance: Is Private Coverage Necessary?

You may want to see also

Explore related products

![]()

U.S. Department of Agriculture (USDA) loans

USDA loans are a type of mortgage loan backed by the U.S. Department of Agriculture under its Rural Development program. They are meant for low- to moderate-income home buyers and come with no down payment, lower mortgage insurance, and interest rates that are below market rates due to government subsidies.

To qualify for a USDA loan, your household income must fall under the set limits, and the home must be your primary residence in an eligible rural area. The USDA loan program doesn't allow cash-out refinancing, and there is no set loan limit; your income and ability to repay will determine how much you can borrow. USDA loans are only available as 30-year fixed-rate mortgages, and they don't come with traditional mortgage insurance.

However, USDA loans do include two guarantee fees that fund the program and protect lenders. There is a one-time upfront fee, usually 1% of the loan amount, which can be paid upfront or rolled into the loan balance. There is also an annual guarantee fee of 0.35% of the remaining principal, split into monthly payments and included in your monthly mortgage payment.

USDA loans often take longer to close than other mortgages, typically requiring two to three weeks more, as they need final approval from the U.S. Department of Agriculture.

Understanding No-Fault Insurance: Wage Verification Report

You may want to see also

Explore related products

![]()

Cancelling mortgage insurance

Mortgage insurance is a safeguard for the lender in case the borrower defaults on the loan. It is usually required if the down payment is less than 20% of the purchase price. There are several ways to cancel your mortgage insurance, depending on the type of loan you have.

If you have a conventional loan, you can cancel your private mortgage insurance (PMI) once your mortgage's loan-to-value (LTV) ratio reaches 78% of the home's purchase price. This is known as the midpoint of your loan's amortization schedule. You can also cancel PMI if your home's value increases, but you will need to pay for a home appraisal to verify the new market value.

If you have a Federal Housing Administration (FHA) loan, you pay a mortgage insurance premium (MIP). MIP is usually required for the life of the loan, but there are exceptions. If you take out an FHA loan with a down payment of at least 10%, you will only pay MIP for 11 years. You can also refinance to a conventional loan to get rid of MIP.

For VA-backed loans, which are intended for servicemembers, veterans, and their families, there is no monthly mortgage insurance premium. However, you pay an upfront "funding fee," which can be rolled into your mortgage. Once you've paid off some of your loan, you may be eligible to cancel your mortgage insurance and won't have to pay the monthly cost.

Title Lock Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage insurance is a type of insurance that protects the lender in case the borrower is unable to make their mortgage payments. It is usually required when the borrower makes a down payment of less than 20% of the home's value.

The process of purchasing mortgage insurance will depend on the type of loan you have. If you have a conventional loan, your lender will arrange for mortgage insurance with a private company, and you will pay the premiums monthly. If you have a Federal Housing Administration (FHA) loan, your mortgage insurance premiums are paid to the FHA, and you will pay an upfront cost as well as a monthly cost.

The cost of mortgage insurance varies depending on the loan type, down payment amount, credit score, and mortgage amount. Typically, you can expect to pay between 0.58% and 1.86% of your mortgage loan amount annually for private mortgage insurance (PMI). For FHA loans, you will pay an upfront cost of 1.75% of the loan amount and an average of 0.85% of the loan amount monthly.