The loan-to-value (LTV) ratio is a lending risk assessment ratio that financial institutions and lenders examine before approving a mortgage. It is calculated by dividing the loan balance by the current value of the property and then multiplying the result by 100. Lenders commonly use the LTV ratio to determine a borrower's eligibility for a loan. FHA loans are mortgages designed for low-to-moderate-income borrowers and require mortgage insurance to guarantee a lender's losses if a homeowner defaults on an FHA loan. This insurance is called a mortgage insurance premium (MIP) and is required regardless of the LTV ratio.

| Characteristics | Values |

|---|---|

| LTV Calculation | Divide the loan balance by the current value of the property, then multiply the result by 100 |

| LTV for FHA Loans | Up to 96.5% |

| Down Payment for FHA Loans | 3.5% |

| Minimum Credit Score for FHA Loans | 500-579 for an LTV of 90%; 580 for an LTV of 96.5% |

| Mortgage Insurance for FHA Loans | Mortgage Insurance Premium (MIP) |

| Mortgage Insurance Premium (MIP) for FHA Loans | 1.75% of the base loan amount |

| Mortgage Insurance Premium (MIP) for FHA Loans with Case Numbers Assigned After June 3, 2013 | Annual MIP |

Explore related products

What You'll Learn

- FHA loans require mortgage insurance to protect lenders against borrower default

- LTV ratio is calculated by dividing loan balance by property value

- LTV ratios above 80% are considered high and may require mortgage insurance

- FHA loans allow an initial LTV ratio of up to 96.5%

- FHA mortgage insurance is more expensive than private mortgage insurance

![]()

FHA loans require mortgage insurance to protect lenders against borrower default

FHA loans are mortgages designed for low- to moderate-income borrowers. They are issued by an FHA-approved lender and insured by the Federal Housing Administration (FHA). FHA loans are a good option for first-time homebuyers who may not have saved enough for a large down payment. Even borrowers who have suffered from bankruptcy or foreclosures may qualify for an FHA-backed mortgage.

The FHA requires both upfront and ongoing mortgage insurance premiums. The upfront MIP payment is equal to 1.75% of the total loan value. For example, if you borrow $150,000 for your mortgage, you will make an upfront payment of $2,500. The ongoing MIP is paid monthly and is included in your monthly payment. The amount you pay depends on your loan amount and loan term.

FHA loans allow an initial LTV ratio of up to 96.5%, but they require MIP for as long as you have that loan. The LTV ratio is a lending risk assessment ratio that financial institutions and other lenders examine before approving a mortgage. A good LTV ratio should be no greater than 80%. Anything above 80% is considered a high LTV, which may require private mortgage insurance.

Pet Insurance: Is It Worth the Cost for Older Dogs?

You may want to see also

Explore related products

![]()

LTV ratio is calculated by dividing loan balance by property value

The loan-to-value (LTV) ratio is a lending risk assessment ratio that financial institutions and other lenders examine before approving a mortgage. It is calculated by dividing the loan balance by the current value of the property, then multiplying the result by 100. For example, if you buy a home that appraises for $100,000, but the owner is willing to sell it for $90,000, and you make a $10,000 down payment, your loan is for $80,000, which results in an LTV ratio of 80% (i.e., 80,000/100,000 x 100).

LTV ratios are important because they affect mortgage approval, interest rates, and even long-term financial opportunities as a homeowner. A lower LTV ratio is generally considered better, as it requires borrowers to come up with larger down payments, which makes them less risky to lenders. Most lenders offer mortgage and home equity applicants the lowest possible interest rates when the LTV ratio is at or below 80%. Mortgages become more expensive for borrowers with higher LTVs, and an LTV above 95% is often considered unacceptable.

FHA loans are mortgages designed for low-to-moderate-income borrowers. They are issued by an FHA-approved lender and insured by the Federal Housing Administration (FHA). FHA loans require a lower minimum down payment and credit scores than many conventional loans. They allow an initial LTV ratio of up to 96.5%require a mortgage insurance premium (MIP) that lasts for as long as you have that loan. Many people decide to refinance their FHA loans once their LTV ratio reaches 80% in order to eliminate the MIP requirement.

FHA mortgage insurance is a government guarantee to pay a lender's losses if you default on a loan. It is required regardless of your down payment amount. Premiums are based on various factors, including your loan amount and loan term.

AE Zone Homes: Insurable?

You may want to see also

Explore related products

![]()

LTV ratios above 80% are considered high and may require mortgage insurance

The loan-to-value (LTV) ratio is a lending risk assessment ratio that financial institutions and other lenders examine before approving a mortgage. It is calculated by dividing the loan balance by the current value of the property and then multiplying the result by 100. Lenders commonly use the LTV ratio to determine a borrower's eligibility for a loan. The higher the LTV, the more risk to the lender, and the more expensive mortgages become for borrowers.

FHA loans are mortgages designed for low-to-moderate-income borrowers. They are issued by an FHA-approved lender and insured by the Federal Housing Administration (FHA). FHA loans require a lower minimum down payment and credit score than many conventional loans. They allow an initial LTV ratio of up to 96.5%mortgage insurance premium (MIP) that lasts for as long as the borrower has that loan, regardless of how low the LTV ratio eventually goes. FHA mortgage insurance is generally more expensive than PMI on a conventional loan, and it's required regardless of the down payment amount.

Many people decide to refinance their FHA loans once their LTV ratio reaches 80% in order to eliminate the MIP requirement. Refinancing can help borrowers get a better deal, improve their credit scores, or avoid defaulting on their loans.

Insuring Your New Home: When to Start

You may want to see also

Explore related products

![]()

FHA loans allow an initial LTV ratio of up to 96.5%

FHA loans are mortgages designed for low-to-moderate-income borrowers. They are issued by an FHA-approved lender and insured by the Federal Housing Administration (FHA). FHA loans require a lower minimum down payment and credit scores than many conventional loans.

The LTV ratio is a lending risk assessment ratio that financial institutions and other lenders examine before approving a mortgage. The higher the LTV, the more risk to the lender, and the more expensive the mortgage becomes for the borrower. A lower LTV indicates that the borrower is a safer bet and may result in lower interest rates.

FHA loans require a mortgage insurance premium (MIP) to offset the risk to the lender. This insurance is required regardless of the LTV ratio and must be paid upfront and on a monthly basis for as long as the loan is in place. Many people choose to refinance their FHA loans once their LTV ratio reaches 80% in order to eliminate the MIP requirement.

Critical Illness Insurance: Is MetLife's Plan Worth the Cost?

You may want to see also

Explore related products

![]()

FHA mortgage insurance is more expensive than private mortgage insurance

FHA loans are mortgages designed for low-to-moderate-income borrowers. They are issued by an FHA-approved lender and insured by the Federal Housing Administration (FHA). FHA loans require a lower minimum down payment and credit score than many conventional loans.

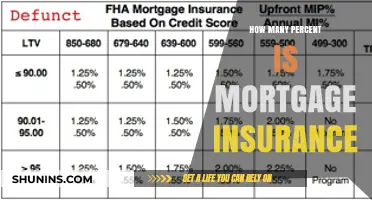

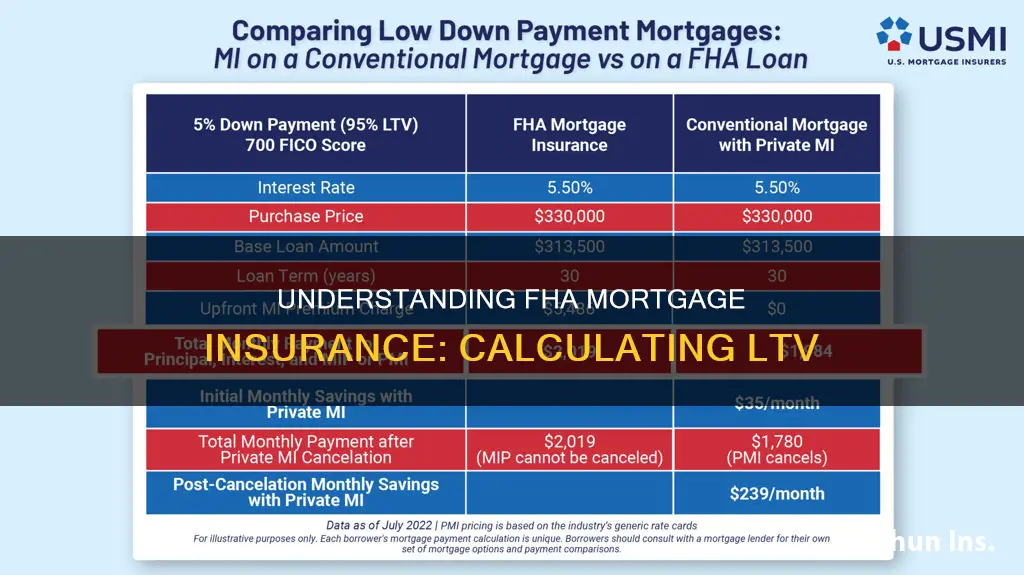

FHA loans require both upfront and ongoing mortgage insurance premiums (MIP). This is an additional payment made to secure the mortgage loan, protecting FHA-approved lenders against losses if a homeowner defaults on an FHA loan. The upfront MIP payment is 1.75% of the total loan value, and the annual MIP is 55 basis points for loans endorsed before June 11, 2012.

Private mortgage insurance (PMI) is required on a conventional mortgage with a down payment below 20%. The cost of PMI varies based on factors like credit score and down payment amount, typically ranging from 0.5% to 2% of the loan amount. For FHA loans, the upfront MIP is a flat rate of 1.75% of the base loan amount, and ongoing MIP is required regardless of the down payment amount. As a result, FHA mortgage insurance is generally more expensive than PMI on a conventional loan.

It's important to note that FHA mortgage insurance requirements have changed over time. Before 2013, MIP worked similarly to PMI, and lenders would cancel MIP once the borrower reached 22% equity in their home. Today, FHA lenders no longer cancel MIP based on home equity percentage, and borrowers may need to pay MIP for the life of the loan.

While FHA mortgage insurance is more expensive, it offers benefits such as flexible programs and low down payment options, making it a popular choice for first-time homebuyers. However, those considering an FHA loan should carefully weigh the costs and benefits against those of conventional loans to determine the best option for their financial situation.

Strategies to Bypass PMI Mortgage Insurance

You may want to see also

Frequently asked questions

LTV stands for loan-to-value ratio. It is a lending risk assessment ratio that financial institutions and other lenders examine before approving a mortgage.

To calculate the LTV of a home, divide the loan balance by the current value of the property, then multiply the result by 100. For example, if you buy a home that appraises for $100,000 but the owner is selling it for $90,000, and you make a $10,000 down payment, your loan is for $80,000, which results in an LTV ratio of 80% (i.e. 80,000/100,000 x 100).

FHA loans require a lower minimum down payment and credit score than many conventional loans. FHA loans allow an initial LTV ratio of up to 96.5%, but they require a mortgage insurance premium (MIP) that lasts for as long as you have that loan. The mortgage insurance protects FHA-approved lenders against losses if you default on your mortgage payments.