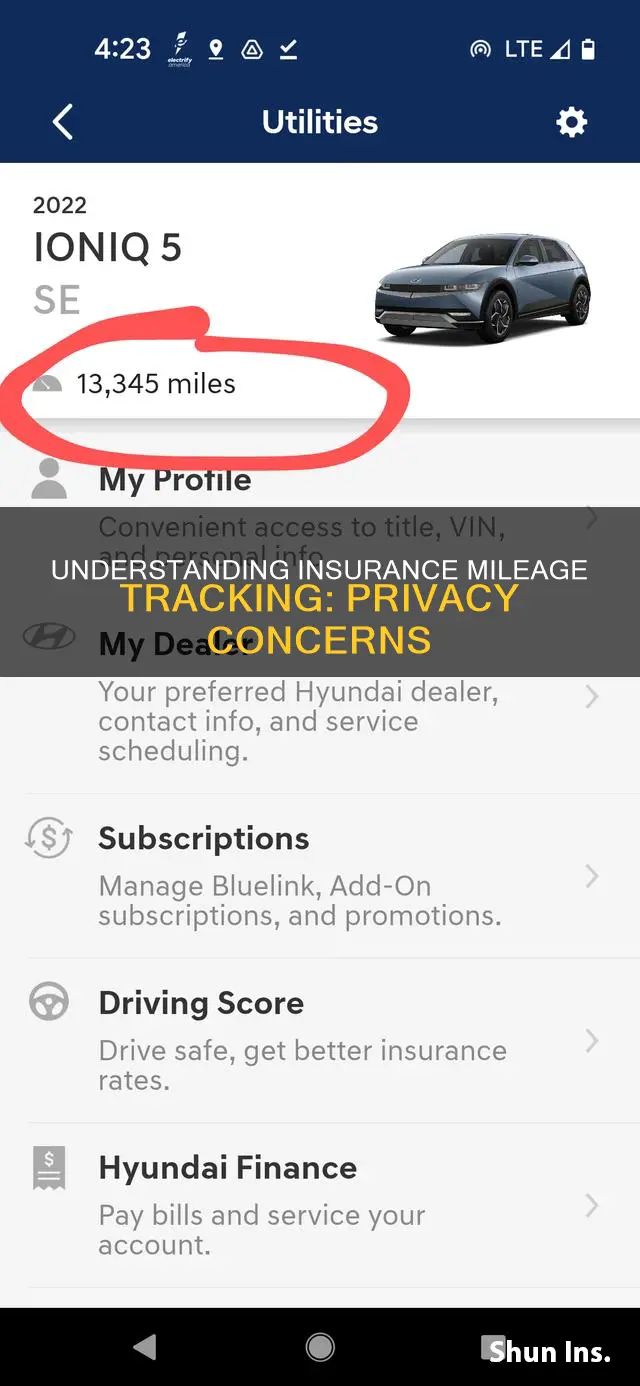

Car insurance companies ask for an estimated annual mileage when you apply for a policy. This is because the number of miles you drive is one of the most important factors in determining what you pay for auto insurance. The more you drive, the greater the odds of being in an accident, and the more likely you are to make a claim. Insurers can verify your annual mileage estimate by tracking your mileage directly through pay-as-you-drive or usage-based insurance programs, or by searching databases that include your mileage totals as reported by state inspection providers, car dealers, and repair shops. They can also confirm your mileage total if you sign up for a telematics program and agree to let them track your mileage in exchange for the opportunity to earn discounts.

| Characteristics | Values |

|---|---|

| How do insurance companies know how many miles? | Insurance companies ask for an estimated annual mileage when you buy a policy. |

| How often do insurance companies ask for mileage? | They only technically have to ask every three years. |

| How do insurance companies verify mileage? | They verify mileage by searching databases, including mileage totals as reported by state inspection providers, car dealers, and repair shops. They can also confirm mileage totals if you sign up for a telematics program and agree to let them track your mileage. |

| How does mileage impact insurance rates? | Mileage is one of the factors that insurance companies consider when determining insurance rates. If you drive fewer miles per year, you pose less risk to your insurer and will pay less. |

| What happens if you go over the estimated mileage? | Going over your estimated mileage could mean your car insurance gets invalidated. |

| What happens if you drive less than the estimated mileage? | If you are driving less than your estimated mileage, you might save money on your insurance premiums by contacting your insurance agent or company and letting them know about the change. |

| How to calculate annual mileage? | There are several ways to calculate annual mileage, including using an odometer, MOT certificates, or a mileage calculator. |

Explore related products

![]()

Mileage estimates

Insurers may request MOT certificates, which detail the total mileage at the time of the MOT test and provide a three-year mileage history. They can also refer to databases that include mileage totals reported by state inspection providers, car dealers, and repair shops. Additionally, some insurers offer telematics or usage-based insurance programs, where they directly track a vehicle's mileage in exchange for potential discounts.

It is important to update your insurer if your driving habits change. For instance, if you start working from home or retire, your annual mileage is likely to decrease, and updating your insurer may result in lower premiums. Some insurers offer low-mileage discounts or pay-as-you-go insurance plans, where you pay a monthly flat fee and are charged per mile driven.

While insurers may not actively investigate every customer's mileage, they are likely to scrutinize it in the event of a claim. Providing an accurate estimate and updating your insurer about any changes in your driving habits can help ensure that your insurance remains valid and that you are paying appropriate rates.

Understanding Your HealthSource Insurance Coverage: What You Need to Know

You may want to see also

Explore related products

![]()

Mileage tracking

There are several methods for insurance companies to track and verify customers' mileage. One common approach is to rely on databases and records, such as DMV records, state inspection providers, car dealers, and repair shops. These sources can provide mileage totals and historical data, allowing insurers to cross-reference and confirm the accuracy of the provided estimates. Additionally, some insurers offer telematics or pay-as-you-drive programs, where customers agree to direct mileage tracking through devices like black boxes in exchange for potential discounts.

Insurers may also utilise MOT certificates, which detail a vehicle's total mileage and provide a three-year mileage history. By comparing yearly differences, insurers and customers can estimate annual mileage more accurately. Another method is to use mileage calculators, which help estimate mileage for insurance purposes. These calculators consider various factors, including the number of named drivers on the policy and the miles travelled for work purposes, ensuring a more comprehensive understanding of the vehicle's usage.

It is worth noting that insurance companies don't routinely investigate every customer's mileage. However, they may conduct a thorough review if a claim is made. Customers should be diligent in updating their mileage estimates with their insurers, especially if their driving habits change due to working from home, retirement, or other factors. By providing accurate and up-to-date mileage information, customers can avoid unexpected issues and ensure their insurance coverage remains valid.

Spouse as Insurance Dependent?

You may want to see also

Explore related products

![Vyncs - GPS Tracker for Vehicles, [No Monthly Fee], 4G LTE, Vehicle Location, Trip History, Driving Alerts, GeoFence, Fuel Economy, OBD Fault Codes, USA-Developed, Family or Fleets](https://m.media-amazon.com/images/I/71LGg1eePQL._AC_UY218_.jpg)

![]()

Low-mileage discounts

The number of miles you drive each year can have a significant impact on your car insurance rates. While insurance companies are not likely to investigate every customer's mileage, they will certainly check when you try to claim. Therefore, it is important to provide accurate and up-to-date mileage information to your insurer.

In New York, for example, drivers can qualify for low-mileage insurance discounts by maintaining an annual mileage below 12,000 miles, with maximum discounts for under 7,500 miles. Top insurers like Metromile, Nationwide, Allstate, and Progressive offer competitive low-mileage discounts.

Pay-per-mile Insurance

Pay-per-mile insurance, also called pay-as-you-go or usage-based insurance, is another option for low-mileage drivers. With this type of policy, you pay a monthly base rate plus an additional fee for every mile you drive. Some pay-per-mile insurance policies also track driving habits like phone usage, hard braking, and fast acceleration, which can further impact your rates.

Tips for Maximizing Savings

To maximize your savings, consider the following:

- Shop around: Compare quotes from multiple insurers to find the best rates and coverage options for your low annual mileage.

- Bundle policies: Combining auto coverage with other types of insurance, such as home insurance, can often result in significant multi-policy discounts.

- Take additional safety courses: Completing an approved accident prevention or defensive driving course can reduce your premiums.

- Review your coverage: Depending on the age of your car, you may be able to drop comprehensive and collision coverage.

Understanding the Fundamentals: Unraveling the Key Attributes of Term Insurance

You may want to see also

Explore related products

![]()

Mileage refunds

In the UK, you can claim tax relief for expenses of employment, such as mileage tax relief for using your own car for work. This is known as the Approved Mileage Allowance Payment (AMAP) rates. If you are not getting the full AMAP rates back from your employer, you can claim the difference from HMRC as a work mileage tax rebate.

To claim a mileage tax rebate, you need to keep records of all the essential work travel expenses you are claiming for. You can use a P87 form or a self-assessment tax return to claim tax relief on your mileage. It is recommended to have your complete mileage records ready in case HMRC requests them and to keep them for six tax years.

It is important to note that a daily commute to a permanent workplace does not qualify for a work mileage tax rebate. Additionally, if you have a named driver on your policy, you need to include the miles they travel in your total annual mileage.

Understanding Insurance: Copay Clauses and Their Implications

You may want to see also

Explore related products

![]()

Mileage fraud

Odometer fraud, also known as "busting miles" in the US or "clocking" in the UK, Ireland, and Canada, is a serious crime that involves disconnecting, resetting, or altering a vehicle's odometer to reduce the number of miles indicated. This fraudulent practice costs American car buyers more than $1 billion annually, as they unknowingly purchase vehicles that have been driven significantly more than indicated, leading to unexpected repairs and maintenance costs.

The National Highway Traffic Safety Administration (NHTSA) estimates that over 450,000 vehicles are sold each year with false odometer readings. To combat this, the Office of Odometer Fraud Investigation, comprising four regional offices, works to increase public awareness, assist consumers with criminal investigations, and protect consumers from odometer fraud. Their investigations have resulted in over 250 criminal convictions across more than 30 states, with prison sentences ranging from one month to ten years and fines and restitutions totaling millions of dollars.

Odometer fraud is challenging to detect, especially with digital odometers that have no visible moving parts. However, there are some ways to identify potential fraud, such as obtaining the vehicle's title or certificate of registration, which contains odometer history, or by contacting the vehicle's former owners and conducting a detailed mechanical inspection.

While insurance companies do not routinely investigate every customer's mileage, they will scrutinize it closely if a claim is made. This is because the number of miles driven is a significant factor in determining insurance rates and premiums. Some insurers even offer refunds if your mileage is lower than initially estimated. Therefore, it is essential to provide accurate mileage information to your insurer and update them if your driving habits change.

Podiatry: Specialist or Not?

You may want to see also

Frequently asked questions

Insurance companies ask for an estimated annual mileage when you buy a policy. They can also track your mileage directly through pay-as-you-drive or usage-based insurance programs. Some insurers might also confirm your mileage total by searching databases that include your mileage totals as reported by state inspection providers, car dealers, and repair shops.

When a car insurance company has an accurate picture of how many miles you drive, it can set rates that more accurately reflect your driving behavior, which then might lead to lower premiums.

Going well over your annual mileage could mean your car insurance gets invalidated. If you think you will go over your mileage, you can phone your insurance company and ask to extend your mileage.

If you are driving significantly less than in the past, you might save money on your car insurance premiums by contacting your insurance agent or company and letting them know about the change. Some insurers are offering refunds if your mileage is less than you originally thought.