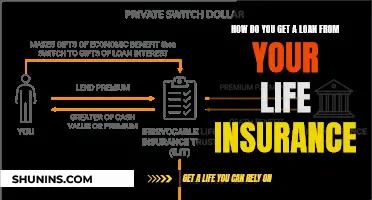

A life insurance trust is a legal agreement that allows a third party to manage the death benefit from a life insurance policy. It ensures that the policy's death benefit is distributed to beneficiaries according to the insured person's wishes and may also reduce any estate tax owed. There are two types of life insurance trusts: irrevocable life insurance trusts (ILIT) and revocable life insurance trusts. An ILIT cannot be changed or cancelled once created, and the assets in the trust will not be included in the grantor's gross estate for estate tax purposes. A revocable trust, on the other hand, offers more flexibility and control, but the death benefit value of the life insurance will be included in the grantor's gross estate for estate tax purposes.

| Characteristics | Values |

|---|---|

| Purpose | Estate planning, protecting assets, and protecting the financial future of beneficiaries |

| Types | Irrevocable life insurance trust (ILIT), revocable life insurance trust (RLIT) |

| Ownership | Trust owns the insurance policy |

| Management | Trustee manages the trust's benefits |

| Distribution | Trustee distributes funds according to the terms of the trust document |

| Timing | Funds can be released to beneficiaries as certain milestones are reached |

| Tax implications | May reduce estate tax, gift tax, and income tax |

| Protection | Can protect assets from creditors and shield beneficiaries from tax penalties |

| Control | Irrevocable trusts cannot be modified or canceled; revocable trusts can be amended or revoked |

| Beneficiaries | Useful for underage or special-needs children, and for structuring benefit payments |

| Formation | Requires an experienced legal professional or estate planning attorney |

Explore related products

$24.95 $24.95

What You'll Learn

![]()

Irrevocable Life Insurance Trusts (ILITs)

ILITs are set up between three legal parties: the grantor (who creates and funds the trust), the trustee (who manages the trust and pays insurance premiums), and the beneficiary/beneficiaries (who will receive the assets upon the grantor's death).

The grantor removes taxable assets from their estate and transfers them to the trust, a separate legal entity. The trustee then uses these assets to purchase a life insurance policy in the grantor's name, and continues to pay the premiums to keep the policy in force. When the grantor passes away, the death benefit is paid directly to the trust, which then distributes the proceeds to the named beneficiaries.

ILITs are an effective way to transfer wealth to beneficiaries outside of the taxable estate, and they also protect legacy assets from potential creditors. They can also be used to set aside assets for a family member with special needs without interfering with their eligibility for government benefits.

One downside of ILITs is that they are irrevocable. This means that the trust cannot be modified or terminated without legal action or the consent of the beneficiaries, as the assets are no longer the property of the grantor.

TiAA Life Insurance: Is It a Good Option?

You may want to see also

Explore related products

![]()

Revocable Life Insurance Trusts

A revocable life insurance trust is one of the two most common categories of trusts, the other being an irrevocable trust. The benefit of a revocable trust is that it gives greater control to the grantor over how beneficiaries receive assets after the grantor's death. It also offers protection from both the grantor's and the beneficiaries' potential future creditors, as well as potential transfer and income tax benefits, and greater privacy.

To set up a revocable life insurance trust, you will need to work with an estate planning attorney to create the trust document. You will need to consider who will act as the trustee of the trust and under what circumstances your beneficiaries will have access to the insurance proceeds. Once the trust document is drafted and signed by you and the trustee(s), you will need to obtain a change of ownership form from your insurance broker or company. After transferring ownership by completing and submitting the form, the trust will own the policy, and payments of the insurance proceeds to the trust will be excluded from your and your spouse's taxable estates.

You can also name the trust as the beneficiary of the policy. It is important to note that for the insurance proceeds to be outside of your estate, you must survive for more than three years from the date you transfer the policy into the trust. If you die within that period, the life insurance amount will be included in your estate for estate tax purposes. Additionally, the transfer of the life insurance policy into trust may be considered a gift and may use up a portion of your gift tax exemptions, so it is essential to consult with an attorney and tax advisor.

Once the policy is in the trust, you and the trustees must ensure that premiums are paid annually. This process will involve contributing the premium amount to the trust as a gift and notifying the trustees of the contribution. The trustees will then notify the beneficiaries of their right to withdraw their proportionate share of the contribution, allowing the contribution to qualify for the annual gift tax exclusion. After a waiting period, the trustee can pay the premium. This process will need to be repeated annually.

American Life Insurance: Social Security Requirements Explained

You may want to see also

Explore related products

![]()

Tax implications

Placing your life insurance in a trust can have significant tax implications, primarily related to inheritance tax.

Inheritance Tax

In the UK, if your total estate, which includes your life insurance, is worth more than £325,000, your beneficiaries may have to pay a 40% inheritance tax bill on the amount over that threshold. By placing your life insurance in a trust, it is no longer considered part of your estate for tax purposes, and your beneficiaries can avoid paying inheritance tax on the insurance payout. This can result in a larger payout for your loved ones and faster access to the funds, as they won't have to wait for the probate process to be completed.

However, it is important to note that there may be tax implications if you change the beneficiary of a life insurance policy held in trust. If you die within seven years of changing the beneficiary, inheritance tax may be due, especially if the new beneficiary is not your spouse or civil partner. The amount of tax charged decreases the longer you live after making the change.

Estate Tax

In some countries, such as the US, placing your life insurance in a trust can also help reduce estate taxes for your family. By having a trust own your life insurance policy, you can shelter the insurance proceeds from estate taxes, preventing them from pushing your estate value over the tax exemption threshold. This is especially beneficial if you are not married or have a policy that only pays out on the death of the second spouse.

Equitable Life Insurance: Does It Cover Medicare in Florida?

You may want to see also

Explore related products

![]()

Benefits of a life insurance trust

A life insurance trust is a legal agreement where a life insurance policy is placed into a trust, removing it from the grantor's estate to provide asset protection, control over the distribution of proceeds, and estate tax benefits. Here are some benefits of a life insurance trust:

Protection from Creditors

Proceeds from life insurance are usually protected under state law, and creditors will not be able to access them. A life insurance trust adds another layer of protection, safeguarding beneficiaries from creditors and unforeseen divorce.

Management and Control of Assets

A life insurance trust ensures the management and distribution of life insurance funds according to the grantor's wishes. Without the trust, beneficiaries would receive the proceeds directly and could spend the funds however they wish.

Avoid Guardianship for Minors

In certain states, if a minor inherits a large sum of money, a guardianship must be established, which can be costly and court-intrusive. A life insurance trust allows the trust to be the beneficiary, and the proceeds can be administered for the minor's benefit without court intervention.

Maintain or Qualify for Government Benefits

If a beneficiary is disabled and receiving government assistance, a life insurance trust can be set up with special needs provisions to protect their interests and ensure they continue to receive government benefits.

Reduce Federal Estate Tax

Life insurance trusts can help reduce federal estate tax liability. The death benefit amount is typically included in the policyholder's estate value, but a life insurance trust separates it, protecting it from additional taxes.

Flex Term Rider: Enhancing Your Life Insurance Coverage

You may want to see also

Explore related products

![]()

Who should use a life insurance trust

A life insurance trust is a legal vehicle that allows a third party (called a trustee) to hold and manage assets in a way that serves the interests of one or more beneficiaries. It is a type of living trust designed to hold ownership of a life insurance policy.

There are two basic types of life insurance trusts: irrevocable and revocable. An irrevocable life insurance trust (ILIT) is a trust that holds a life insurance policy on behalf of the policyholder for the eventual disbursement to beneficiaries. It is generally used to reduce estate tax liability and cannot be modified or cancelled once established. A revocable life insurance trust (RLT), on the other hand, gives the grantor more control over their assets as it can be changed, amended, or terminated at any time.

- Estate Taxes: If you are concerned about estate taxes, a life insurance trust can help reduce the tax liability on your estate. By transferring ownership of your life insurance policy to a trust, you can exclude the policy from your taxable estate, potentially saving your loved ones a significant amount of money.

- Control Over Proceeds: A life insurance trust allows you to control how and when the proceeds are distributed to the beneficiaries. You can dictate that the trustee distribute the proceeds monthly, annually, or upon reaching certain milestones. This can be especially useful if you have concerns about the age, maturity level, or debt level of the beneficiaries.

- Preservation of Government Benefits: A life insurance trust can help preserve the eligibility of beneficiaries who receive asset-dependent benefits from the government, such as Medicaid. By controlling the distribution of proceeds, the trust can ensure that the beneficiaries remain within the eligibility thresholds for these benefits.

- Asset Protection: A life insurance trust can limit the amount of funds that creditors can pursue, providing protection for your assets.

- Planning for Generational Legacies: A life insurance trust can provide for future generations, including those who haven't yet been born, and help them inherit wealth in a tax-efficient manner.

- Special Needs Beneficiaries: If you have a special needs child who will require long-term care, a life insurance trust can be an effective tool to manage and control funds for their care. The trustee can manage the funds and pay them out according to your wishes, helping to preserve the child's eligibility for essential government benefits.

It is important to note that life insurance trusts may not be necessary or beneficial for everyone. They can be expensive to form and can create additional tax and legal complexities. As such, it is generally recommended for individuals with substantial wealth or specific estate planning objectives, such as leaving money to underage or special-needs children. Consulting with an experienced financial professional or estate planning attorney can help determine if a life insurance trust is the right choice for your situation.

Life Insurance Options Post-Mastectomy: What You Need to Know

You may want to see also

Frequently asked questions

A life insurance trust is a legal agreement that allows a third party to manage the death benefit from a life insurance policy. A trust ensures that your policy's death benefit is distributed to your beneficiaries according to your wishes. It also exempts the funds from probate and may reduce any estate tax owed.

A life insurance trust can provide a number of benefits. If you have substantial wealth, it may help shield your beneficiaries from having to pay estate taxes on life insurance proceeds, helping to preserve family wealth across generations. It can also help ensure that your loved ones are taken care of when and how you want after you pass away, especially if they cannot manage assets on their own. Finally, when life insurance and other assets are placed in a trust, they bypass the often lengthy and burdensome probate process that ordinary wills are subjected to.

Generally speaking, once established, irrevocable trusts cannot be changed. So, for example, if you think you may need to access the cash value of your life insurance policy at some point in the future, then putting it in an irrevocable life insurance trust may not be your best option. A revocable trust can be changed, but there may be significant legal fees for doing so. That’s why trusts are most often used by those with significant wealth and specific estate planning objectives, as opposed to others whose financial needs may change.