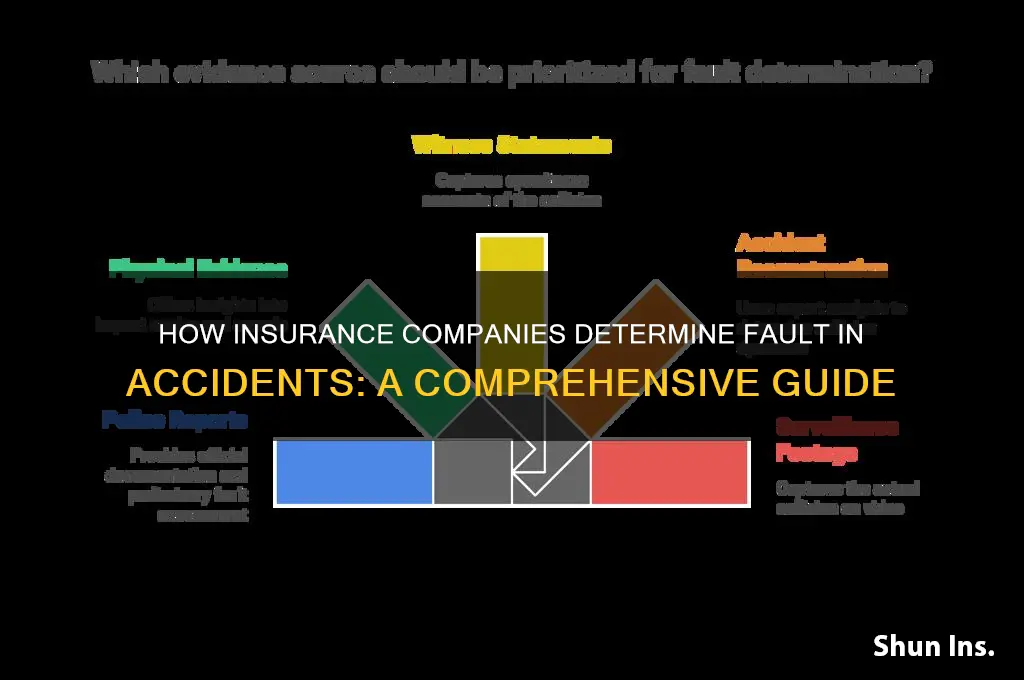

Determining fault is a critical process in insurance claims, as it directly impacts liability and compensation. Insurance companies typically assess fault by examining evidence such as police reports, witness statements, photos, and applicable traffic laws. They may also rely on accident reconstruction experts or surveillance footage to piece together the sequence of events. In no-fault states, the process differs, as each party’s insurance covers their own damages regardless of fault, though fault may still be determined for severe injuries or property damage. Ultimately, the insurer’s decision is based on a thorough investigation to ensure fairness and adherence to legal and policy guidelines.

| Characteristics | Values |

|---|---|

| Police Reports | Official accident reports filed by law enforcement detailing the incident and initial fault assessment. |

| State Traffic Laws | Fault is determined based on violation of traffic laws (e.g., running a red light, speeding). |

| Witness Statements | Accounts from bystanders or other drivers involved in the accident. |

| Photographic Evidence | Photos or videos of the accident scene, vehicle damage, and road conditions. |

| Vehicle Damage Location | Damage location (e.g., rear-end collisions often indicate fault of the trailing driver). |

| Driver Statements | Admissions of fault or descriptions of the incident from involved drivers. |

| Surveillance Footage | Video evidence from nearby cameras (e.g., traffic cameras, dashcams, or business security). |

| Accident Reconstruction | Expert analysis to recreate the accident and determine fault based on physics and evidence. |

| Insurance Claims History | Past claims and driving records of involved parties may influence fault determination. |

| No-Fault States | In no-fault states, fault is less relevant as each driver’s insurance covers their own damages. |

| Comparative Negligence | Fault is shared among parties based on their degree of responsibility in at-fault states. |

| Medical Records | Injuries sustained can help establish the severity of the accident and potential fault. |

| Weather and Road Conditions | External factors like weather, road conditions, or visibility may impact fault assessment. |

| Vehicle Maintenance Records | Fault may be assigned if a vehicle malfunction (e.g., brake failure) caused the accident. |

| Insurance Adjuster Investigation | Adjusters review all evidence to make a final fault determination for claims processing. |

Explore related products

What You'll Learn

- Accident Reports: Police and witness statements provide critical details to assess liability

- State Laws: Fault determination varies by jurisdiction, following no-fault or at-fault rules

- Evidence Review: Photos, videos, and damage assessments help reconstruct the accident

- Driver Statements: Accounts from involved parties are evaluated for consistency and credibility

- Claims History: Past claims and driving records may influence fault determination

![]()

Accident Reports: Police and witness statements provide critical details to assess liability

Police and witness statements serve as the backbone of accident investigations, offering a factual foundation for insurance companies to determine fault. These reports are not mere formalities; they are detailed narratives that capture the sequence of events, contributing factors, and the actions of all parties involved. For instance, a police report might note the speed of the vehicles, road conditions, and whether traffic laws were violated, while witness statements can provide additional perspectives on what transpired. Together, they create a multi-dimensional view of the accident, enabling insurers to reconstruct the scene with greater accuracy. Without these documents, insurers would often rely solely on the conflicting accounts of the drivers, making fault determination a speculative exercise rather than an evidence-based process.

Consider the role of police reports in a hypothetical scenario: a two-car collision at an intersection. The officer’s report includes diagrams, timestamps, and citations for running a red light. This objective documentation carries significant weight in the insurer’s assessment, as it is less likely to be biased compared to the drivers’ versions of events. Witness statements, on the other hand, can corroborate or challenge the police findings. For example, a bystander might recall seeing one driver texting moments before the crash, adding a layer of detail that the police report may not capture. Insurers analyze these accounts to identify consistencies and discrepancies, piecing together a reliable narrative that informs their liability decision.

However, relying on accident reports is not without challenges. Police officers may make errors in their assessments, and witnesses can have imperfect memories or biased viewpoints. Insurers must critically evaluate the credibility of these sources, cross-referencing them with physical evidence like skid marks, vehicle damage, and surveillance footage. For instance, if a witness claims a driver was speeding but the skid marks suggest otherwise, the insurer may discount that part of the statement. This meticulous process ensures that fault is assigned based on the most reliable information available, reducing the likelihood of disputes or litigation.

Practical tip: If you’re involved in an accident, ensure the police report is thorough by providing detailed information to the officer and requesting a copy for your records. Encourage witnesses to stay at the scene and share their contact information with both the police and your insurer. The more comprehensive the reports, the clearer the liability picture becomes. For example, noting the weather conditions, visibility, and the exact positions of the vehicles can significantly aid the insurer’s analysis. Proactive steps like these can expedite the claims process and reduce ambiguity in fault determination.

In conclusion, accident reports are indispensable tools for insurers in assessing liability. They transform subjective accounts into objective evidence, providing a structured framework for fault determination. While not infallible, police and witness statements, when combined with other evidence, offer the best available means to reconstruct accidents and assign responsibility fairly. Understanding their role empowers policyholders to engage more effectively with the claims process, ensuring their side of the story is accurately represented.

Scooter Insurance Requirements: What You Need to Know Before Riding

You may want to see also

Explore related products

![]()

State Laws: Fault determination varies by jurisdiction, following no-fault or at-fault rules

In the United States, the determination of fault in an accident is not a one-size-fits-all process. A critical factor shaping this determination is the state in which the accident occurs. State laws dictate whether a no-fault or at-fault system governs the aftermath of a collision, significantly impacting how insurance companies handle claims and assign responsibility.

Understanding these jurisdictional differences is crucial for drivers, as it directly affects their financial liability and the process of seeking compensation after an accident.

No-Fault States: A Focus on Personal Coverage

In no-fault states, such as New York, Florida, and Michigan, the emphasis is on personal injury protection (PIP) insurance. Regardless of who caused the accident, each driver's insurance company covers their own medical expenses and lost wages up to a certain limit, typically ranging from $10,000 to $50,000, depending on the state. This system aims to streamline the claims process and reduce litigation. However, it also means drivers in no-fault states may have limited options for pursuing compensation for pain and suffering or other non-economic damages unless their injuries meet specific severity thresholds.

For instance, in New York, a driver can only step outside the no-fault system and sue for additional damages if they suffer a "serious injury" as defined by state law, which includes fractures, disfigurement, or permanent loss of use of a body organ.

At-Fault States: Assigning Responsibility and Liability

In contrast, at-fault states, which constitute the majority in the U.S., follow a traditional tort-based system. Here, the driver deemed responsible for the accident is liable for the damages incurred by the other party. Insurance companies in these states conduct thorough investigations to determine fault, relying on police reports, witness statements, and physical evidence. The at-fault driver's insurance company then covers the injured party's medical bills, property damage, and other losses.

Comparative Fault: Sharing Responsibility

Some at-fault states further complicate matters by employing comparative fault rules. These rules allow for the apportionment of fault between the parties involved. For example, if Driver A is found 70% at fault and Driver B is 30% at fault, Driver A's insurance would cover 70% of Driver B's damages, and vice versa. This system encourages a more nuanced approach to fault determination, recognizing that accidents often result from the actions of multiple parties.

Practical Implications for Drivers

The variation in state laws highlights the importance of understanding your local regulations. Drivers should familiarize themselves with their state's fault system and insurance requirements. In no-fault states, ensuring adequate PIP coverage is essential, while in at-fault states, maintaining sufficient liability insurance is crucial. Additionally, documenting accidents thoroughly, regardless of the state, is vital. This includes taking photos, exchanging information with other drivers, and filing a police report, as these details can significantly influence the fault determination process.

In conclusion, the determination of fault by insurance companies is intricately tied to state laws, with no-fault and at-fault systems presenting distinct approaches to handling accident claims. Being aware of these jurisdictional differences empowers drivers to navigate the post-accident process more effectively and make informed decisions regarding their insurance coverage.

Whole Life Insurance Dividends: What, Why, and How?

You may want to see also

Explore related products

![]()

Evidence Review: Photos, videos, and damage assessments help reconstruct the accident

Visual evidence is the cornerstone of accident reconstruction in insurance claims. Photos and videos capture the immediate aftermath, preserving critical details that may fade from memory or be misremembered. A single image can reveal skid marks, vehicle positions, traffic signals, and road conditions—all vital clues for determining fault. For instance, a photo showing a car’s crumpled hood and the other vehicle’s undamaged side panel can strongly suggest which driver was at fault. Similarly, dashcam footage can provide an unbiased, real-time account of the collision, eliminating guesswork and reducing disputes. Without such evidence, insurers often rely on conflicting statements, making resolution slower and less accurate.

Damage assessments, conducted by trained professionals, complement visual evidence by providing a technical analysis of the accident. These assessments evaluate the extent and type of damage to vehicles, such as point of impact, severity, and direction of force. For example, a rear-end collision typically results in damage to the rear bumper of the leading vehicle and the front bumper of the trailing vehicle. By cross-referencing this data with photos and videos, insurers can corroborate or challenge claims. A damage report might reveal that a vehicle’s damage is inconsistent with the driver’s account, raising questions about their credibility. This scientific approach adds objectivity to the fault determination process.

While photos and videos are powerful tools, their effectiveness depends on quality and context. Blurry images or footage taken from a poor angle may obscure key details, hindering the investigation. To maximize utility, take multiple photos from various angles, including close-ups of damage and wide shots of the scene. If possible, capture timestamps and geotags to establish when and where the accident occurred. For videos, ensure the recording is uninterrupted and includes audio, as sounds like screeching tires or honking horns can provide additional context. Properly collected visual evidence not only speeds up claims processing but also strengthens the insurer’s ability to make a fair determination.

Despite the value of evidence review, it’s not without challenges. Disputes can arise when one party claims evidence was tampered with or when multiple pieces of evidence contradict each other. In such cases, insurers may turn to accident reconstruction experts who use physics, engineering, and computer simulations to recreate the event. These experts analyze factors like vehicle speed, braking distance, and road friction to validate or refute claims. While this step is costly and time-consuming, it’s often the final arbiter in complex cases. Ultimately, the combination of visual evidence, damage assessments, and expert analysis ensures a thorough and impartial fault determination.

Self-Insurance in Michigan: A Step-by-Step Guide for Residents

You may want to see also

Explore related products

![]()

Driver Statements: Accounts from involved parties are evaluated for consistency and credibility

In the aftermath of a car accident, driver statements serve as the first layer of evidence for insurance companies. These accounts, provided by the involved parties, are not taken at face value. Instead, they undergo rigorous scrutiny to assess their consistency and credibility. For instance, if one driver claims the light was red while another insists it was green, the insurer will cross-reference these statements with other evidence, such as traffic camera footage or witness testimonies. This process is critical because conflicting or unreliable statements can significantly delay claim resolution or lead to incorrect fault determinations.

Evaluating consistency involves comparing each driver’s account to itself and to other available evidence. Insurers look for discrepancies in details like speed, location, or sequence of events. For example, a driver who initially states they were traveling at 30 mph but later mentions 45 mph raises red flags. Similarly, credibility is assessed by examining the clarity, plausibility, and emotional tone of the statement. A driver who provides a calm, detailed account without exaggerations is often deemed more credible than one who appears agitated or omits key details. Practical tip: When giving a statement, stick to the facts, avoid speculation, and remain composed to enhance your credibility.

The role of driver statements is not just to assign blame but to reconstruct the accident accurately. Insurers use these accounts as a foundation, layering them with physical evidence, police reports, and expert analysis. For example, if a driver claims the other party was texting, but there’s no phone record or witness to support this, the statement’s weight diminishes. Conversely, a consistent account backed by skid marks or vehicle damage can strengthen a claim. This multi-faceted approach ensures fault is determined fairly, even when statements alone are insufficient.

One cautionary note: drivers should be aware that their statements can be legally binding. Misrepresenting facts, even unintentionally, can lead to denied claims or legal repercussions. For instance, a driver who admits fault out of guilt, only to later realize the other party was speeding, may face challenges in retracting their statement. To avoid such pitfalls, drivers should take time to gather their thoughts and review the scene before providing an account. If unsure about specific details, it’s better to state that clearly rather than guess.

In conclusion, driver statements are a pivotal yet complex component of fault determination. Their value lies in their ability to provide immediate, firsthand perspectives, but their limitations require careful validation. By understanding how insurers evaluate these accounts, drivers can better prepare themselves to provide accurate, credible statements that contribute to a fair and efficient claims process. Remember, clarity and honesty are your best tools in this critical moment.

Annuities: Are They Safe From Theft?

You may want to see also

![]()

Claims History: Past claims and driving records may influence fault determination

Insurance companies often scrutinize an individual's claims history and driving record when determining fault in an accident. This practice is rooted in the principle that past behavior can predict future actions. For instance, a driver with multiple at-fault claims or traffic violations is statistically more likely to be involved in future incidents. Insurers use this data to assess risk and allocate fault, even if the current accident’s circumstances seem ambiguous. A single speeding ticket might not sway the decision, but a pattern of reckless driving could significantly influence the outcome.

Consider a scenario where two drivers collide at an intersection. Driver A has a clean record, while Driver B has filed three at-fault claims in the past five years. Even if the police report doesn’t clearly assign blame, the insurer might lean toward Driver B being at fault based on their history. This approach isn’t about punishment but about leveraging data to make informed decisions. However, it’s crucial for policyholders to understand that past claims don’t automatically determine fault—they’re one piece of a larger puzzle.

To mitigate the impact of a claims history, drivers can take proactive steps. For example, enrolling in defensive driving courses can improve skills and sometimes reduce the weight of past infractions. Additionally, maintaining a claim-free record for several years can gradually lessen the influence of previous incidents. Insurers often review the timing and frequency of claims, so a single claim from a decade ago carries less weight than multiple recent ones. Practical tip: Review your driving record annually for inaccuracies and dispute any errors, as these can unfairly skew fault determinations.

Comparatively, claims history is treated differently across jurisdictions and insurers. In no-fault states, where drivers rely on their own insurance regardless of fault, past claims might still affect premiums but have less bearing on fault allocation. In contrast, tort-based systems heavily rely on fault determination, making claims history a critical factor. Understanding these nuances can help drivers navigate the claims process more effectively. For instance, a driver in a no-fault state might focus on minimizing premium increases rather than disputing fault.

Ultimately, while claims history and driving records can influence fault determination, they aren’t the sole deciding factors. Insurers also consider accident specifics, witness statements, and applicable laws. Policyholders should remain vigilant about their driving behavior and claims submissions, as these actions create a narrative that insurers reference in future incidents. By staying informed and proactive, drivers can better manage how their history impacts fault determinations and, consequently, their insurance outcomes.

Understanding Actual Cash Value in Life Insurance Policies

You may want to see also

Frequently asked questions

The insurance company determines fault by reviewing police reports, witness statements, photos, and other evidence. They may also use state traffic laws and accident reconstruction experts to assess liability.

The police report is a critical piece of evidence as it includes the officer’s observations, statements from involved parties, and sometimes a preliminary determination of fault. Insurance companies heavily rely on it but may conduct their own investigation.

Yes, insurance companies can disagree on fault, especially in complex cases. If this happens, they may negotiate or involve a third-party arbitrator. In some cases, the matter may go to court for resolution.

In states with comparative negligence laws, fault can be shared between parties. The insurance company will assign a percentage of fault to each driver based on their contribution to the accident, which impacts claim payouts accordingly.