Life insurance policies can grow in value over time, and permanent life insurance includes a death benefit on top of a cash value accumulation. This cash value is a crucial component of variable universal and universal life insurance policies, representing the savings component of the policy. It is built up by splitting premium payments into three categories: the cost of insurance, fees and overhead, and cash value. The leftover portion of the premium, after the cost of insurance and fees, is used to build up the policy's cash value, which can then be invested by the insurance company. This cash value can be used to pay premiums, or the policyholder can borrow against it, and it can be invested in stocks, bonds, or mutual funds.

| Characteristics | Values |

|---|---|

| How it works | A portion of the premium payments made by the policyholder is allocated after deducting the cost of insurance. The remaining amount is credited to the savings account, which grows over time. |

| Calculation | Accumulated value is calculated as the sum or total of the initial investment, plus interest earned to date. |

| When it begins to build | When the policyholder starts paying a monthly premium. |

| Borrowing against the accumulated value | Policyholders can borrow against the accumulated value while keeping the policy intact. |

| Surrendering the policy | Policyholders can surrender the policy to the insurance company and receive the cash surrender value in return, minus any surrender charges. |

| Tax implications | Accumulated value is tax-deferred as long as the policyholder keeps the insurance contract valid. |

| Investment options | Policyholders may be able to invest the accumulated value across multiple investment options, such as stocks, bonds, or mutual funds. |

| Impact on overall policy performance | Accumulated value can impact the overall performance of the policy, so policyholders should regularly review it and consult with financial professionals. |

Explore related products

What You'll Learn

- The accumulation value is the total amount of investment, including the initial investment and any interest earned

- Accumulation value is calculated as the sum of the initial investment and interest earned to date

- Accumulation value is important as it represents the savings component of a life insurance policy

- Accumulation value can be used to cover policy expenses, pay premiums, or take out a loan

- Accumulation value is dependent on factors such as policy performance, investment returns, and associated fees

![]()

The accumulation value is the total amount of investment, including the initial investment and any interest earned

Life insurance policies can provide a death benefit to your loved ones in the event of your untimely passing. However, certain types of life insurance policies, such as whole life insurance, universal life insurance, and variable life insurance, also offer a cash value component, allowing you to accumulate wealth over time. This accumulation value is the total amount of investment, including the initial investment and any interest earned.

When you pay your premiums for a cash value life insurance policy, your payments are divided into three categories. A portion of your premium is allocated to the policy's death benefit, which is based on factors such as your age and health. Another portion covers the insurance company's operating costs and profits. The remaining portion contributes to the policy's cash value, which forms the accumulation value.

Over time, as you continue to pay premiums and earn interest, the accumulation value grows. This value can be thought of as a forced savings account, which the policyholder can borrow against while keeping the policy intact. The accumulation value can also be used to pay premiums, create an investment portfolio, or supplement retirement income.

It's important to note that the accumulation of cash value in a life insurance policy can take several years. In the early years of the policy, a higher percentage of your premium is allocated to the cash value, but as you grow older, the cost of insuring your life increases, resulting in a larger portion of the premium being applied to insurance costs. Additionally, different policies accumulate cash value at different rates, depending on factors such as current interest rates and investment performance.

The accumulation value of a life insurance policy is a valuable feature that provides not only protection but also opportunities for wealth accumulation and tax advantages. By understanding how the accumulation value works, policyholders can make informed decisions about managing their financial goals and needs.

Terminating Irrevocable Life Insurance Trusts: Is It Possible?

You may want to see also

Explore related products

$8.99

$15.95

![]()

Accumulation value is calculated as the sum of the initial investment and interest earned to date

Accumulated value, also known as the accumulated amount or cash value, is the total amount an investment currently holds, including the capital invested and the interest it has earned to date. In life insurance, the accumulated value is the total acquired value of a whole life insurance policy.

When a policyholder starts paying their monthly premiums, the insurance company takes those payments and divides them into two portions. The first portion covers the basic insurance policy costs, while the second portion acts as an investment that accumulates cash value, which is placed in an internal account by the insurance company. Over time, the cash value in a whole life insurance policy grows at a fixed rate determined by the policy's terms.

The accumulated value of a life insurance policy can be calculated as the sum of the initial investment and the interest earned to date. This value represents the total amount of investment, including the capital invested and any earned interest. The interest earned on the investment contributes to the steady growth of the policy's cash value over time.

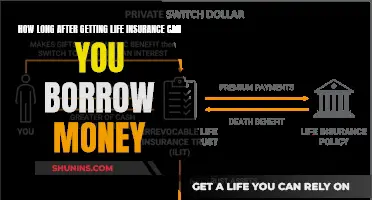

The accumulated value in a life insurance policy is important as it can be thought of as a forced savings account, which the policyholder can borrow against while keeping the policy intact. Policyholders can also use the accumulated value to pay their policy premiums, create an investment portfolio, or supplement their retirement income.

It is worth noting that the accumulated value is subject to various factors, such as policy performance, investment returns, and fees associated with the life insurance policy. Policyholders should regularly review their accumulation value and consult with financial professionals or insurance advisors to make informed decisions about managing their financial goals.

Uncovering a Relative's Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Accumulation value is important as it represents the savings component of a life insurance policy

Accumulation value is a crucial component of life insurance policies, representing the savings element of the policy. It is important because it enables policyholders to build up a sum of money that can be utilised in various ways, such as borrowing against it or investing it to achieve financial goals.

When an individual purchases a life insurance policy, they start paying monthly premiums. The insurance company divides these premium payments into two portions. The first portion covers the basic costs of the insurance policy, while the second portion acts as an investment that accumulates cash value. This cash value is placed in an internal account by the insurance company and forms the accumulation value.

The accumulation value is significant as it represents the savings component of the life insurance policy. It is the amount of money that the policyholder can access and use while keeping the policy intact. The policyholder can borrow against the accumulation value, similar to a forced savings account, providing them with financial flexibility. This feature is especially beneficial if the policyholder encounters unexpected expenses or wishes to invest in other opportunities.

Additionally, the accumulation value grows over time. As the policyholder continues to pay premiums, the accumulation value increases. This growth is influenced by factors such as policy performance, investment returns, and fees associated with the policy. Policyholders can further enhance the growth of their accumulation value by investing it in various options, such as stocks, bonds, or mutual funds.

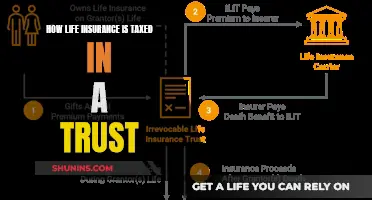

Moreover, the accumulation value serves as the foundation for calculating the Cash Surrender Value. If a policyholder chooses to surrender or terminate their policy before its maturity date, they will receive the Cash Surrender Value, which is based on the accumulation value minus any applicable surrender charges. This provides policyholders with the option to access a lump sum of money by cancelling their policy.

In summary, the accumulation value in a life insurance policy is important as it represents the savings component. It allows policyholders to borrow against their policy, provides financial flexibility, grows over time, and forms the basis for calculating the Cash Surrender Value. Understanding and regularly reviewing the accumulation value is crucial for policyholders to make informed decisions and effectively manage their financial goals.

Dave Ramsey's Take on Life Insurance

You may want to see also

Explore related products

![]()

Accumulation value can be used to cover policy expenses, pay premiums, or take out a loan

Accumulation value, also referred to as accumulated amount or cash value, is an important component of variable universal and universal life insurance policies. It is the total amount of investment, including the capital invested and any interest earned. In the context of life insurance, it is the total acquired value of a whole life insurance policy.

Accumulation value can be used in several ways. One option is to cover policy expenses, ensuring that the policyholder can continue to benefit from the coverage provided. Additionally, the accumulated value can be utilised to pay premiums, reducing the need for out-of-pocket expenses to maintain the policy. Policyholders can also borrow against their accumulated value, providing them with financial flexibility while keeping the policy intact. This is similar to using the accumulated value as collateral for a loan, which can result in more favourable loan terms and lower interest rates.

The ability to use the accumulated value to cover expenses, pay premiums, or secure a loan provides policyholders with financial flexibility and can be particularly useful in times of financial need. It is worth noting that the specific terms and conditions of a policy may impact how the accumulated value can be utilised, so it is important for policyholders to carefully review their policies. Consulting with a financial professional or insurance advisor can help policyholders make informed decisions about managing their accumulated value in alignment with their financial goals.

Life Insurance and Globulin: Understanding the Rating Connection

You may want to see also

Explore related products

![]()

Accumulation value is dependent on factors such as policy performance, investment returns, and associated fees

Accumulation value is the total amount an investment currently holds, including the capital invested and the interest earned to date. In the context of life insurance, it is also known as the cash value or accumulated amount. This value begins to accumulate when the policyholder starts paying the monthly premiums. The premium payments are divided into two portions by the insurance company: the first portion covers the basic insurance policy costs, while the second portion acts as an investment that accumulates cash value, which is placed in an internal account.

The accumulation value of a life insurance policy is influenced by various factors, such as policy performance, investment returns, and associated fees. Policy performance refers to how well the insurance policy is doing in terms of its financial returns. Different policies accumulate cash value in different ways, depending on the type of policy and the individual life insurance company. Whole life policies, for example, provide "guaranteed" fixed cash value accounts that grow according to a formula determined by the insurance company, while universal life policies accumulate cash value based on current interest rates and investments.

Investment returns also play a crucial role in determining the accumulation value. The money allocated to the cash value account is typically invested by the insurance company, and the returns on these investments contribute to the growth of the accumulation value. The rate of return can be fixed, as in the case of whole life insurance, or variable, depending on how the premium payments are invested, as with universal life insurance.

Associated fees, such as policy expenses and surrender charges, can impact the accumulation value. In the early years of a policy, a larger portion of the premium payments may go towards covering these fees and basic insurance policy costs, leaving less money to accumulate in the cash value account. Additionally, there may be fees associated with withdrawing or borrowing against the accumulation value, which can reduce the total amount available to the policyholder.

It is important for policyholders to regularly review their accumulation value and understand how it is impacted by these various factors. By consulting with financial professionals or insurance advisors, policyholders can make informed decisions about managing their financial goals and maximising the accumulation value of their life insurance policies.

Life Insurance Payouts: Are Arizonans Taxed on Benefits?

You may want to see also

Frequently asked questions

The accumulated value is the total amount an investment currently holds, including the capital invested and the interest it has earned to date.

The accumulated value of a life insurance policy is calculated as the sum of the initial investment and the interest earned to date. It is similar to a forced savings account, which the policyholder can borrow against while keeping the policy intact.

The accumulated value of a life insurance policy grows over time as the policyholder pays their premiums. A portion of the premium payments is allocated to the policy's savings component after deducting the cost of insurance. This remaining amount is then credited to a savings account, which grows over time.

Yes, it is possible to sell your life insurance policy for its accumulated value. This can be done by surrendering the policy to the insurance company or selling it to a third party in the secondary market. However, it is important to note that there may be surrender charges and other fees associated with terminating the policy before its maturity date, which can reduce the cash surrender value.

The accumulated value in a life insurance policy offers several benefits. It can be used as a source of funds for loans, paying premiums, or investing. It also provides tax advantages as the value accumulates on a tax-deferred basis. Additionally, the accumulated value can be used to strike a balance between protection and accumulation, depending on the policyholder's individual goals.