Healthcare insurance plays a critical role in ensuring individuals and families have access to affordable medical care while mitigating the financial risks associated with unexpected illnesses or injuries. Understanding how healthcare insurance works involves grasping key concepts such as premiums, deductibles, copayments, and coverage limits, which determine the extent of financial protection provided. Additionally, navigating the complexities of different insurance plans—whether employer-sponsored, government-funded, or private—requires careful consideration of individual health needs, budget constraints, and provider networks. As healthcare costs continue to rise, having adequate insurance coverage has become essential for maintaining both physical and financial well-being, making it crucial for individuals to educate themselves about their options and make informed decisions.

Explore related products

What You'll Learn

- Understanding Policy Types: HMO, PPO, EPO, and POS plans explained for tailored healthcare coverage

- Cost Factors: Premiums, deductibles, copays, and out-of-pocket maximums impact overall insurance expenses

- Network Coverage: In-network vs. out-of-network providers affect costs and care accessibility

- Essential Benefits: Coverage for hospitalization, prescriptions, preventive care, and mental health services

- Enrollment Periods: Open enrollment, special enrollment, and Medicaid/Medicare eligibility timelines

![]()

Understanding Policy Types: HMO, PPO, EPO, and POS plans explained for tailored healthcare coverage

Choosing the right healthcare insurance plan can feel like deciphering a foreign language. HMO, PPO, EPO, POS – these acronyms represent distinct approaches to managing your healthcare costs and access. Understanding their nuances is crucial for selecting a plan that aligns with your needs and budget.

Let's dissect these common policy types, highlighting their strengths, weaknesses, and ideal scenarios.

HMOs (Health Maintenance Organizations) prioritize cost-effectiveness and coordinated care. Imagine a tightly knit healthcare network where your primary care physician acts as your gatekeeper. You'll need referrals from them to see specialists within the network. This structured approach often results in lower premiums and out-of-pocket costs. HMOs are ideal for individuals who prioritize affordability, value preventive care, and are comfortable with a designated primary care provider managing their healthcare journey.

Think of it as a membership to a healthcare club with predefined rules and benefits.

PPOs (Preferred Provider Organizations) offer greater flexibility and choice. Unlike HMOs, PPOs allow you to visit any doctor or specialist within their network without a referral. You can also seek care outside the network, though at a higher cost. This flexibility comes at a price – PPOs typically have higher premiums and deductibles. They suit individuals who prioritize freedom of choice, require specialized care, or frequently travel and need access to a wider range of providers.

EPOs (Exclusive Provider Organizations) blend elements of HMOs and PPOs. Similar to HMOs, EPOs restrict coverage to in-network providers. However, they don't require referrals for specialists. This hybrid model offers lower premiums than PPOs while providing more flexibility than HMOs. EPOs are a good fit for those who want a balance between cost control and provider choice within a defined network.

POS (Point of Service) plans introduce an interesting twist. They combine features of HMOs and PPOs, allowing you to choose between in-network and out-of-network care. However, you'll pay less if you stay within the network and obtain referrals for specialists. POS plans offer a middle ground for those who want some flexibility but are willing to navigate a more complex system to manage costs.

Think of it as a choose-your-own-adventure approach to healthcare coverage.

Ultimately, the best policy type depends on your individual needs and priorities. Consider factors like your health status, budget, preferred level of provider choice, and tolerance for out-of-pocket expenses. Carefully review plan details, including deductibles, copays, and covered services, to make an informed decision. Remember, understanding these policy types is the first step towards securing tailored healthcare coverage that empowers you to take control of your health and well-being.

GM Restores Vision Insurance: A Welcome Move

You may want to see also

Explore related products

![]()

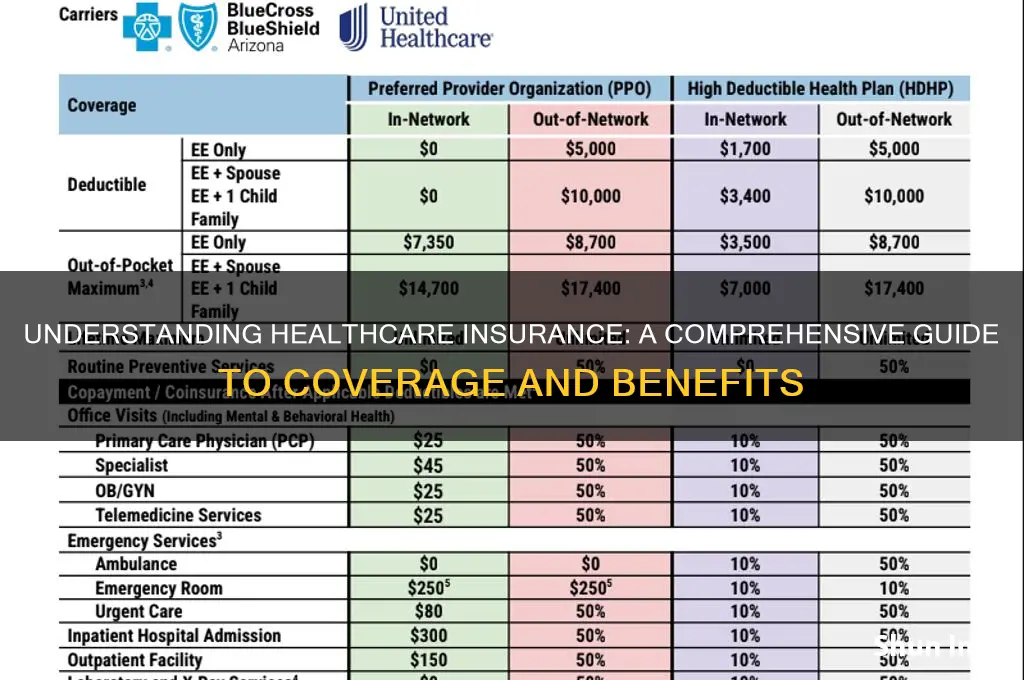

Cost Factors: Premiums, deductibles, copays, and out-of-pocket maximums impact overall insurance expenses

Healthcare insurance costs are a complex puzzle, with premiums, deductibles, copays, and out-of-pocket maximums as the key pieces. Understanding how these factors interact is crucial for managing your overall expenses. Let's break it down.

Premiums: The Foundation of Your Coverage

Imagine your premium as the monthly or annual fee that keeps your insurance policy active. It's like a membership fee, granting you access to the benefits outlined in your plan. Premiums vary widely based on factors such as age, location, and the level of coverage. For instance, a 30-year-old in Massachusetts might pay around $300-$500 per month for a mid-tier plan, while a family plan could range from $800 to $1,500. Lower premiums often come with higher deductibles and copays, so it’s a trade-off between upfront costs and potential out-of-pocket expenses later.

Deductibles: The First Hurdle in Coverage

Your deductible is the amount you must pay out of pocket before your insurance kicks in. Think of it as a threshold. For example, if your plan has a $2,000 deductible, you’ll cover the first $2,000 of medical expenses annually. Plans with lower premiums typically have higher deductibles, shifting more financial risk to you. For someone who rarely visits the doctor, a high-deductible plan might make sense, but it’s risky if unexpected medical needs arise.

Copays: Predictable Costs for Routine Care

Copays are fixed amounts you pay for specific services, like a doctor’s visit or prescription. For instance, a primary care visit might cost $25, while a specialist could be $50. Copays provide predictability for routine care but can add up if you need frequent services. Some plans also have coinsurance, where you pay a percentage of the cost (e.g., 20%) after meeting your deductible. Understanding these nuances helps you budget for ongoing healthcare needs.

Out-of-Pocket Maximums: Your Financial Safety Net

The out-of-pocket maximum is the most you’ll spend annually on covered services, excluding premiums. Once you hit this limit—say, $6,000 for an individual—your insurance covers 100% of additional costs. This cap protects you from catastrophic expenses, especially in cases of serious illness or injury. For example, a hospital stay costing $50,000 would only require you to pay up to your maximum, shielding you from financial ruin.

Balancing Act: Choosing the Right Plan

Selecting a plan requires weighing these cost factors against your health needs and budget. If you have chronic conditions or anticipate high medical usage, a plan with higher premiums but lower deductibles and copays might save you money. Conversely, healthy individuals may benefit from lower premiums and higher out-of-pocket costs. Tools like healthcare.gov or insurance brokers can help compare plans, ensuring you find the best fit for your situation.

By dissecting premiums, deductibles, copays, and out-of-pocket maximums, you can make informed decisions that align with your financial and health goals. It’s not just about finding the cheapest plan—it’s about finding the one that offers the most value for your unique needs.

Understanding Income Protection Insurance: Calculation Methods and Factors Explained

You may want to see also

Explore related products

![]()

Network Coverage: In-network vs. out-of-network providers affect costs and care accessibility

Healthcare insurance networks are a double-edged sword. While they offer negotiated rates and streamlined billing, they also restrict your choice of providers. Understanding the difference between in-network and out-of-network care is crucial for managing costs and accessing the right treatment.

In-network providers have agreements with your insurance company, meaning they've agreed to accept pre-negotiated rates for services. This translates to lower out-of-pocket costs for you, as your insurance plan typically covers a larger portion of the bill. For example, a routine checkup with an in-network doctor might cost you a $20 copay, while the same visit with an out-of-network doctor could result in a $100 bill after insurance adjustments.

Out-of-network providers haven't contracted with your insurance company, leading to higher costs. You'll likely face higher deductibles, coinsurance, and potentially even balance billing, where the provider charges you the difference between their full fee and what the insurance company reimburses. Imagine needing a specialized surgery: an in-network surgeon might cost you $500 out-of-pocket after insurance, while an out-of-network specialist could leave you with a $2,000 bill.

However, there are situations where venturing out-of-network might be necessary. If you require a specific specialist not available within your network, or if you're seeking a second opinion, out-of-network care might be your only option. Some plans offer partial coverage for out-of-network services, but it's essential to understand the specifics of your plan's out-of-network benefits before making a decision.

Remember, network coverage directly impacts both your wallet and your access to care. Carefully review your insurance plan's provider directory, understand your out-of-network benefits, and don't hesitate to contact your insurance company for clarification. Making informed choices about in-network versus out-of-network care empowers you to navigate the healthcare system effectively and ensure you receive the care you need at a cost you can afford.

Understanding Contingent Cargo Insurance: Coverage, Benefits, and Importance

You may want to see also

Explore related products

![]()

Essential Benefits: Coverage for hospitalization, prescriptions, preventive care, and mental health services

Healthcare insurance plans often highlight essential benefits as their cornerstone, but what does this truly entail for policyholders? At its core, essential benefits encompass four critical areas: hospitalization, prescriptions, preventive care, and mental health services. These are not optional add-ons but mandated coverage under the Affordable Care Act (ACA), ensuring individuals receive comprehensive care without financial strain. For instance, hospitalization coverage includes not just the cost of a hospital stay but also surgeries, intensive care, and emergency room visits, which can otherwise lead to crippling debt. Understanding these benefits is the first step in maximizing your insurance value.

Prescription drug coverage is another vital component, yet it’s often misunderstood. Plans typically categorize medications into tiers, with generic drugs costing less than brand-name or specialty medications. For example, a 30-day supply of a generic cholesterol-lowering drug might cost $10, while a brand-name equivalent could be $50 or more. To save money, ask your doctor if a generic alternative is available or use mail-order pharmacies for long-term prescriptions. Additionally, some plans offer dosage flexibility, such as a 90-day supply for chronic conditions, reducing out-of-pocket costs over time.

Preventive care is a proactive approach to health, covering services like vaccinations, screenings, and check-ups at no additional cost. For adults, this includes annual physicals, cancer screenings (e.g., mammograms for women over 40, colonoscopies for those over 50), and immunizations like the flu shot. For children, it covers developmental screenings, vision and hearing tests, and vaccinations such as the MMR (measles, mumps, rubella) vaccine. Taking advantage of these services can detect health issues early, often when they’re most treatable, and prevent costly treatments down the line.

Mental health services, once overlooked, are now recognized as essential to overall well-being. Coverage includes therapy sessions, psychiatric consultations, and medication management for conditions like depression, anxiety, and bipolar disorder. For example, a typical plan might cover 20 outpatient therapy sessions per year, with a copay of $20–$40 per visit. Inpatient care for severe cases, such as hospitalization for suicidal ideation, is also covered, though it may require prior authorization. Advocates emphasize the importance of parity, meaning mental health coverage should be on par with physical health benefits, ensuring equal access to care.

In practice, these essential benefits work together to provide a safety net for individuals and families. Consider a scenario where a 45-year-old develops chest pain: hospitalization coverage ensures they can undergo diagnostic tests and treatment without financial worry. Follow-up prescriptions for blood pressure medication are covered, preventive care includes a cholesterol screening to avoid future issues, and mental health services address the stress of the experience. By understanding and utilizing these benefits, policyholders can navigate the healthcare system more effectively, ensuring both physical and financial health.

Voya Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Enrollment Periods: Open enrollment, special enrollment, and Medicaid/Medicare eligibility timelines

Understanding enrollment periods is crucial for securing healthcare coverage without facing penalties or gaps in care. Open Enrollment typically runs from November 1 to December 15 each year, though some states extend this window. During this time, individuals can enroll in or change their health insurance plans without needing a qualifying event. Missing this period often means waiting a full year, unless you qualify for Special Enrollment. This exception allows changes outside the open window due to life events like marriage, birth of a child, loss of other coverage, or relocation. Each event triggers a 60-day window to act, so prompt action is essential.

Medicaid and Medicare operate on different timelines. Medicaid enrollment is year-round, as it’s based on income and eligibility, not a fixed period. Applications are processed through state agencies, and approval can take up to 45 days, though expedited decisions are possible for urgent cases. Medicare, on the other hand, has specific enrollment phases. Initial Enrollment begins three months before your 65th birthday month and ends three months after, totaling a seven-month window. Missing this can result in late penalties. Medicare Advantage and Part D plans follow annual open enrollment from October 15 to December 7, mirroring private insurance timelines but with distinct rules.

Comparing these systems highlights their flexibility and rigidity. While open enrollment for private plans is strict, special enrollment and Medicaid’s year-round access provide safety nets. Medicare’s structure combines fixed and flexible periods, balancing predictability with adaptability. For instance, a 64-year-old planning for retirement should mark their Initial Enrollment Period, while a family expecting a child should prepare for Special Enrollment. Understanding these differences ensures you leverage the right system at the right time.

Practical tips can streamline the process. Set calendar reminders for open enrollment dates and qualifying life events. Gather documents like pay stubs, tax returns, or marriage certificates in advance for Medicaid or Special Enrollment applications. For Medicare, consult the official website or a counselor to avoid penalties. If you miss a deadline, explore short-term plans or state-specific extensions as temporary solutions. Proactive planning transforms enrollment from a chore into a strategic step toward continuous coverage.

Finally, consider the interplay between these systems. For example, losing employer-sponsored insurance might qualify you for Special Enrollment, but if your income drops significantly, Medicaid could be a better fit. Similarly, turning 65 while on Medicaid requires navigating dual eligibility with Medicare. Each program’s timeline overlaps with others, creating a complex but navigable landscape. By mastering these periods, you ensure not just compliance, but optimal coverage tailored to your needs.

Understanding Insurance Surplus: Definition, Importance, and Impact on Policyholders

You may want to see also

Frequently asked questions

MA healthcare insurance, often referring to Medicare Advantage plans, combines Medicare Parts A (Hospital) and B (Medical) into a single plan, often including Part D (Prescription Drug) coverage. These plans are offered by private insurers approved by Medicare and may include additional benefits like dental, vision, or wellness programs.

Eligibility for MA healthcare insurance typically requires individuals to be enrolled in Medicare Parts A and B, live in the plan’s service area, and be a U.S. citizen or lawfully present in the country. Most plans do not cover individuals with End-Stage Renal Disease (ESRD), except in specific cases.

Costs for MA healthcare insurance vary by plan and location. While some plans have $0 monthly premiums, others may charge a premium in addition to the Medicare Part B premium. Additional costs include copays, coinsurance, and deductibles, which differ based on the plan’s structure and the services used.