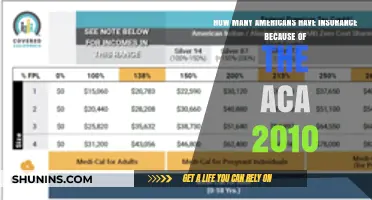

Before the Affordable Care Act (ACA), commonly known as Obamacare, was passed in 2010, millions of Americans lacked health insurance coverage. In 2010, approximately 48.6 million non-elderly Americans were uninsured, representing about 18% of the population under age 65. The uninsured rate was particularly high among low-income individuals, part-time workers, and those employed in small businesses, as many could not afford private insurance and did not qualify for public programs like Medicaid or Medicare. The ACA aimed to address this gap by expanding Medicaid eligibility, creating health insurance marketplaces, and implementing reforms to make coverage more accessible and affordable, significantly reducing the uninsured rate in subsequent years.

| Characteristics | Values |

|---|---|

| Year | 2010 (pre-ACA) |

| Total Uninsured Americans | Approximately 48.6 million |

| Uninsured Rate | 16.3% of the population |

| Uninsured Children | 7.5 million (9.5% of children) |

| Uninsured Young Adults (19-25) | 8.8 million (29.7% of this age group) |

| Uninsured Non-Elderly Adults | 33.3 million (19.5% of non-elderly adults) |

| Uninsured by Race/Ethnicity | - Hispanic: 32.4% - Black: 20.8% - White: 12.4% |

| Uninsured by Income Level | - Below 138% of poverty line: 28.9% - 138-250% of poverty line: 22.1% - Above 250% of poverty line: 8.9% |

| Uninsured by Employment Status | - Part-time workers: 27.5% - Unemployed: 27.4% - Full-time workers: 10.8% |

| Uninsured by State | Varied significantly; states like Texas (24.6%) and New Mexico (21.9%) had higher uninsured rates compared to states like Massachusetts (4.4%) and Hawaii (7.7%) |

| Source | U.S. Census Bureau, Current Population Survey (CPS) |

Explore related products

What You'll Learn

![]()

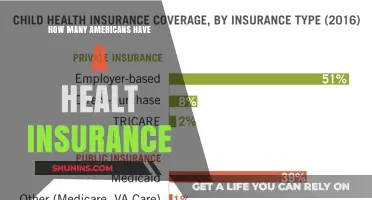

Pre-ACA uninsured rates by age group

Before the Affordable Care Act (ACA) was passed in 2010, the uninsured rate in the United States varied significantly by age group, reflecting disparities in access to employer-sponsored coverage, financial stability, and eligibility for public programs. Young adults aged 19 to 25 were among the most vulnerable, with an uninsured rate of approximately 30% in 2010. This group often faced gaps in coverage as they transitioned from parental plans to independent insurance, compounded by lower wages and part-time employment. The ACA later addressed this issue by allowing young adults to remain on their parents’ plans until age 26, a policy that significantly reduced uninsured rates in this demographic.

In contrast, children under 18 had a relatively lower uninsured rate of around 8% pre-ACA, largely due to programs like the Children’s Health Insurance Program (CHIP) and Medicaid. These safety nets provided critical coverage for low-income families, though disparities persisted among states with varying eligibility criteria. For adults aged 26 to 34, the uninsured rate hovered around 28%, driven by factors such as job instability and the lack of affordable individual market options. This age group was particularly at risk due to their reliance on employer-based insurance, which often excluded part-time or gig workers.

Middle-aged adults, aged 35 to 54, faced an uninsured rate of roughly 18%, reflecting their higher likelihood of full-time employment with benefits. However, this group also included individuals with pre-existing conditions who struggled to obtain affordable coverage in the individual market. Older adults aged 55 to 64, nearing Medicare eligibility, had an uninsured rate of about 11%, though this figure masked significant financial strain for those without employer coverage or sufficient savings to bridge the gap to Medicare.

Analyzing these trends reveals a clear pattern: younger Americans were disproportionately uninsured pre-ACA, while older adults benefited from greater access to employer-sponsored or public coverage. The ACA’s reforms, such as expanding Medicaid and creating health insurance marketplaces, aimed to address these age-based disparities. For instance, states that expanded Medicaid saw dramatic reductions in uninsured rates across all age groups, particularly among low-income adults.

Practical takeaways from this data underscore the importance of age-specific policies in health reform. Young adults benefit from extended parental coverage, while older adults require affordable options to bridge the gap to Medicare. Policymakers and advocates can use these insights to design targeted interventions, ensuring that future reforms address the unique challenges faced by each age group. Understanding pre-ACA uninsured rates by age not only highlights historical inequities but also provides a roadmap for building a more inclusive healthcare system.

Borrowing from Life Insurance: What You Can and Can't Do

You may want to see also

Explore related products

![]()

Employer-based coverage before the ACA

Before the Affordable Care Act (ACA) was passed in 2010, employer-based health insurance was the cornerstone of the American healthcare system, covering approximately 158 million individuals, or about 60% of the non-elderly population. This system relied heavily on employers offering health benefits as part of their compensation packages, a practice rooted in historical wage controls during World War II. However, this model was far from universal, leaving millions uninsured or underinsured due to job instability, part-time work, or employer cost-cutting measures.

Consider the mechanics of this system: employers typically negotiated group plans with insurers, leveraging their large employee pools to secure lower premiums. Yet, this arrangement disproportionately benefited workers in larger, more stable companies, often in higher-paying sectors. Small businesses, comprising nearly half of the private workforce, were less likely to offer coverage due to prohibitive costs. For instance, in 2009, only 46% of firms with 3–9 workers provided health insurance, compared to 98% of firms with 200+ employees. This disparity underscored the inequities embedded in employer-based coverage.

A critical flaw in this pre-ACA model was its vulnerability to economic downturns. During the 2008 recession, for example, an estimated 2.6 million workers lost employer-sponsored insurance (ESI) as companies slashed benefits to cut costs. Even those who retained coverage faced increasing out-of-pocket expenses, with average annual premiums for family coverage rising from $9,249 in 2000 to $13,375 in 2009. This trend highlighted the precarious nature of tying healthcare to employment, a risk the ACA later sought to mitigate through individual market reforms and Medicaid expansion.

To illustrate the human impact, imagine a 35-year-old retail worker earning $30,000 annually. Pre-ACA, if their employer didn’t offer insurance—a common scenario in low-wage sectors—they faced limited options: purchasing costly individual plans (often with exclusions for pre-existing conditions) or going uninsured. This example underscores how employer-based coverage, while dominant, failed to address the needs of millions, particularly those in precarious or low-wage jobs.

In conclusion, employer-based coverage before the ACA was a double-edged sword: a lifeline for many, yet a source of exclusion and instability for others. Its reliance on employment status created systemic gaps, leaving the most vulnerable populations at risk. Understanding this pre-ACA landscape is crucial for appreciating the reforms that followed, particularly the ACA’s efforts to decouple healthcare from employment and expand access through alternative pathways.

Climbing the Ladder: Strategies to Advance Your Insurance Career

You may want to see also

Explore related products

![]()

Medicaid enrollment prior to 2010

Before the Affordable Care Act (ACA) was passed in 2010, Medicaid served as a critical safety net for millions of low-income Americans, though its reach was limited by stringent eligibility criteria. In 2009, approximately 46.5 million individuals were enrolled in Medicaid, a figure that highlights both the program’s importance and its constraints. Eligibility was primarily restricted to specific categories: pregnant women, children, parents with dependent children, the elderly, and individuals with disabilities. For example, in most states, non-disabled adults without children were categorically excluded, regardless of how low their income was. This patchwork system left significant gaps in coverage, particularly among able-bodied adults living in poverty.

The eligibility thresholds for Medicaid prior to 2010 were strikingly low, often set at or below the federal poverty level (FPL). For instance, in 2009, a family of three could qualify for Medicaid only if their income was below $10,830 annually, which was 67% of the FPL. These thresholds varied widely by state, with some states offering more generous coverage while others maintained stricter limits. Children, however, fared slightly better due to the Children’s Health Insurance Program (CHIP), which extended coverage to those in families earning up to 200% of the FPL. Despite these efforts, an estimated 9.4 million children remained uninsured in 2009, underscoring the limitations of pre-ACA Medicaid.

A critical issue with Medicaid enrollment prior to 2010 was the administrative complexity that deterred eligible individuals from applying. The application process often required extensive documentation, in-person interviews, and lengthy approval times. For example, applicants had to provide proof of income, citizenship, and residency, which could be particularly challenging for those with unstable living situations or limited access to necessary documents. This bureaucratic burden disproportionately affected vulnerable populations, including the homeless, undocumented immigrants, and those with mental health issues, further exacerbating disparities in access to care.

Comparatively, Medicaid’s role in covering long-term care for the elderly and disabled was more robust, with over two-thirds of nursing home residents relying on the program. However, this aspect of Medicaid was often funded through asset spend-down policies, requiring individuals to deplete their savings before qualifying. This created a perverse incentive for families to shield assets, complicating the financial planning process for many. The pre-ACA Medicaid system, while essential, was thus a patchwork of coverage that left millions uninsured or underinsured, setting the stage for the transformative changes introduced by the ACA.

Dirt Bike Experience: Does It Impact Motorcycle Insurance Rates?

You may want to see also

Explore related products

![]()

Individual insurance market pre-ACA

Before the Affordable Care Act (ACA) was enacted in 2010, the individual insurance market in the United States was characterized by significant barriers to access, limited consumer protections, and wide disparities in coverage availability. Approximately 15% of Americans, or about 48 million people, were uninsured in 2010, with many of these individuals relying on the individual market for coverage. This market, however, was fraught with challenges that often left consumers vulnerable to high costs, denied coverage, or inadequate plans.

One of the most striking features of the pre-ACA individual market was the practice of medical underwriting, where insurers could deny coverage or charge exorbitant premiums based on pre-existing conditions. For example, a person with a history of cancer, diabetes, or even asthma could be deemed "uninsurable" or face premiums that were financially crippling. This left millions of Americans with few options, often forcing them to go without insurance or settle for bare-bones plans that excluded essential benefits like prescription drugs or maternity care. The result was a system that disproportionately harmed those with the greatest health needs.

Another critical issue was the lack of standardized benefits and consumer protections. Unlike employer-sponsored plans, which were subject to some state and federal regulations, individual market plans varied widely in terms of coverage and cost. Many plans had lifetime or annual caps on benefits, meaning individuals with serious illnesses could quickly exhaust their coverage. Additionally, insurers could rescind policies retroactively if they discovered a pre-existing condition not disclosed during the application process, leaving policyholders with medical bills and no coverage. These practices created a climate of uncertainty and fear for those in the individual market.

The pre-ACA individual market also lacked a mechanism to pool risk effectively, leading to higher premiums for healthier individuals and limited options for those with lower incomes. Without a mandate to purchase insurance or subsidies to offset costs, younger and healthier people often opted out of coverage, skewing the risk pool toward older and sicker individuals. This adverse selection drove up premiums, making insurance even less affordable for those who needed it most. For context, the average annual premium for an individual policy in 2009 was around $2,985, a significant expense for many households.

In summary, the individual insurance market before the ACA was a fragmented and often predatory system that failed to provide adequate, affordable coverage for millions of Americans. Its flaws—medical underwriting, lack of standardized benefits, and poor risk pooling—highlighted the need for comprehensive reform. The ACA’s subsequent introduction of protections for pre-existing conditions, essential health benefits, and premium subsidies marked a transformative shift, addressing many of the systemic issues that plagued this market. Understanding this pre-ACA landscape is crucial for appreciating the impact of the reforms that followed.

Wyoming Boat Insurance: Is It Required for Your Watercraft?

You may want to see also

Explore related products

![]()

Uninsured demographics before ACA passage

Before the Affordable Care Act (ACA) was passed in 2010, approximately 46.5 million Americans, or about 15% of the population, were uninsured. This staggering number wasn’t evenly distributed; certain demographics bore a disproportionate share of the burden. Understanding who these uninsured individuals were provides critical context for the ACA’s impact. Young adults aged 19 to 25, for instance, faced higher uninsured rates compared to older age groups, with nearly 30% lacking coverage. This was partly due to aging off parental plans and limited access to employer-sponsored insurance in entry-level jobs.

Geography played a significant role in uninsured rates, with Southern and Western states like Texas, Florida, and New Mexico reporting higher percentages of uninsured residents. These states often had stricter eligibility criteria for Medicaid and lower rates of employer-sponsored coverage, leaving millions without viable options. In Texas alone, over 25% of the population was uninsured, the highest rate in the nation. This regional disparity highlighted the patchwork nature of healthcare access before the ACA.

Low-income individuals were another heavily affected group, with nearly 40% of adults living below the federal poverty level lacking insurance. For this demographic, the cost of private insurance was prohibitive, and Medicaid eligibility was often out of reach due to restrictive state policies. Families with incomes just above the poverty line were particularly vulnerable, as they earned too much to qualify for Medicaid but too little to afford private plans. This coverage gap left millions in a perilous financial position, often forgoing necessary care.

Racial and ethnic minorities also faced higher uninsured rates, reflecting systemic disparities in healthcare access. Nearly 30% of Hispanic Americans and 20% of Black Americans were uninsured, compared to 11% of non-Hispanic whites. Language barriers, immigration status, and occupational segregation into low-wage jobs without benefits contributed to these disparities. For example, undocumented immigrants were entirely excluded from federal and state insurance programs, leaving them with few options beyond emergency care.

Finally, workers in industries like retail, hospitality, and agriculture were less likely to have employer-sponsored insurance, driving up uninsured rates among these groups. Small businesses, which employed a significant portion of the workforce, were less likely to offer health benefits due to cost constraints. This left millions of workers and their families vulnerable, often relying on inconsistent or inadequate coverage. These demographic patterns underscore the targeted challenges the ACA aimed to address, reshaping the landscape of healthcare access in the U.S.

Life Insurance: Strategies for a Successful Sale

You may want to see also

Frequently asked questions

Approximately 84% of Americans, or about 260 million people, had health insurance coverage in 2010 before the ACA was enacted.

About 16% of Americans, or roughly 48 million people, were uninsured in 2010 prior to the ACA's passage.

Yes, the ACA reduced the uninsured rate from 16% in 2010 to approximately 9% by 2015, covering millions more Americans.

Low-income individuals, young adults, and people of color had disproportionately higher uninsured rates before the ACA was implemented.

Employer-based insurance was the most common form of coverage, with about 55% of Americans insured through their jobs or a family member’s job in 2010.