The Affordable Care Act (ACA), often referred to as Obamacare, has significantly reshaped the American healthcare landscape since its inception in 2010. One of the most critical aspects of the ACA is its expansion of health insurance coverage, particularly through the establishment of health insurance marketplaces and Medicaid expansion. As of recent data, millions of Americans have gained access to health insurance through ACA-compliant plans, either via the marketplaces or expanded Medicaid programs. Understanding the number of Americans covered under ACA insurance is essential for assessing the law’s impact on reducing the uninsured rate, improving access to care, and addressing ongoing challenges in the healthcare system. Current estimates suggest that tens of millions of individuals rely on ACA-related coverage, highlighting its pivotal role in the nation’s healthcare infrastructure.

Explore related products

$19.99

What You'll Learn

- Enrollment Trends: Annual ACA sign-ups and renewals since its inception

- State-by-State Coverage: Variations in ACA enrollment across different U.S. states

- Demographic Breakdown: ACA coverage by age, income, and ethnicity

- Impact of Medicaid Expansion: How Medicaid expansion affects ACA enrollment numbers

- Subsidy Utilization: Percentage of enrollees receiving premium tax credits

![]()

Enrollment Trends: Annual ACA sign-ups and renewals since its inception

Since its inception in 2010, the Affordable Care Act (ACA) has seen fluctuating enrollment numbers, reflecting shifting political landscapes, economic conditions, and public awareness. The first open enrollment period in 2013–2014 attracted 8 million sign-ups, a figure that climbed to over 12 million by 2016. However, subsequent years witnessed a decline, with 2017–2018 enrollments dropping to 8.7 million due to reduced advertising budgets and policy changes under the Trump administration. Despite these challenges, the ACA has demonstrated resilience, with enrollments rebounding to 11.3 million in 2021–2022, partly fueled by increased federal funding and expanded outreach efforts during the COVID-19 pandemic.

Analyzing these trends reveals a clear correlation between policy support and enrollment rates. For instance, the 2021 American Rescue Plan Act, which expanded subsidies and made coverage more affordable, led to a 21% increase in sign-ups during the 2022 open enrollment period. Conversely, attempts to repeal the ACA in 2017 coincided with a 4% drop in enrollments. Renewals, which typically account for 80–85% of annual enrollments, have remained relatively stable, indicating that once individuals secure coverage, they tend to maintain it. However, attracting new enrollees remains a challenge, particularly among younger, healthier populations who may perceive lower immediate need for insurance.

A comparative analysis of state-level data highlights the impact of Medicaid expansion on ACA enrollment trends. States that expanded Medicaid under the ACA saw lower marketplace enrollments initially, as more individuals qualified for Medicaid. However, these states have consistently maintained higher overall coverage rates. Non-expansion states, such as Texas and Florida, have experienced higher marketplace enrollments but also higher uninsured rates, underscoring the importance of comprehensive policy implementation. For example, California, a Medicaid expansion state, has consistently enrolled over 1.5 million individuals annually, while Texas, with its limited Medicaid program, struggles to reach 1 million enrollees despite a larger uninsured population.

To maximize ACA enrollment, practical strategies include leveraging technology for streamlined applications, extending open enrollment periods, and targeting underserved populations through community-based outreach. For instance, Healthcare.gov introduced a "Fast App" feature in 2022, reducing application time by 25%. Additionally, states like New York and Colorado have implemented their own marketplaces, offering localized support and tailored plans. Individuals can optimize their enrollment experience by comparing plans during open enrollment (typically November 1 to January 15), checking for subsidy eligibility, and seeking assistance from certified navigators. Renewals should be reviewed annually to ensure coverage aligns with changing health needs and financial circumstances.

In conclusion, ACA enrollment trends since its inception reflect a dynamic interplay of policy, economics, and public engagement. While renewals remain robust, boosting new sign-ups requires targeted efforts to address affordability, awareness, and accessibility. By learning from successful state models and implementing innovative strategies, the ACA can continue to expand coverage and fulfill its mission of making healthcare accessible to all Americans.

Best Universal Life Insurance: Comprehensive Coverage for All

You may want to see also

Explore related products

![]()

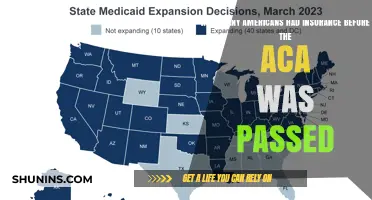

State-by-State Coverage: Variations in ACA enrollment across different U.S. states

The Affordable Care Act (ACA) has significantly reshaped the American health insurance landscape, but its impact isn’t uniform. Enrollment rates vary widely across states, influenced by factors like Medicaid expansion, state-run exchanges, and local economic conditions. For instance, as of 2023, states like California and New York, which embraced Medicaid expansion and established robust state-run marketplaces, report higher ACA enrollment rates. In contrast, states like Texas and Florida, which have not expanded Medicaid, lag behind, leaving millions uninsured despite the ACA’s framework.

Consider the role of state policies in driving these disparities. States with expanded Medicaid programs, such as Kentucky and Nevada, have seen uninsured rates drop dramatically, often below 5%. These states actively promote enrollment through outreach campaigns and simplified application processes. Conversely, non-expansion states like Mississippi and Alabama continue to struggle with uninsured rates above 10%, as residents fall into the "coverage gap"—earning too much for traditional Medicaid but too little for ACA subsidies.

Another critical factor is the presence of state-run health insurance exchanges. States operating their own marketplaces, like Washington and Colorado, often offer more tailored plans and extended enrollment periods, boosting participation. Federally facilitated marketplaces, while accessible, may lack localized marketing and support, leading to lower enrollment in states like Georgia and Tennessee. For example, Washington’s exchange provides year-round enrollment for certain populations, a strategy that could be replicated elsewhere to increase coverage.

Economic and demographic differences also play a role. States with higher poverty rates, such as Louisiana and West Virginia, face greater challenges in enrolling eligible residents, even with Medicaid expansion. Cultural attitudes toward healthcare and political messaging further complicate efforts. In states where ACA enrollment is framed as a personal responsibility rather than a societal benefit, participation tends to be lower, regardless of available resources.

To address these variations, policymakers and advocates should focus on targeted solutions. Non-expansion states could revisit Medicaid expansion, as seen in Missouri and Oklahoma, where ballot initiatives have pushed for change. States with federally facilitated marketplaces might consider transitioning to state-run models to better meet local needs. Additionally, leveraging community health workers and digital tools can improve outreach in underserved areas. By understanding these state-by-state nuances, stakeholders can work toward a more equitable distribution of ACA coverage nationwide.

Step-by-Step Guide to Enrolling in UCR Insurance Coverage

You may want to see also

Explore related products

![]()

Demographic Breakdown: ACA coverage by age, income, and ethnicity

The Affordable Care Act (ACA) has significantly reshaped the American health insurance landscape, but its impact isn’t uniform across all demographics. Understanding who benefits most from ACA coverage requires a closer look at age, income, and ethnicity—factors that reveal both successes and gaps in the system.

Age plays a pivotal role in ACA enrollment patterns. Young adults aged 18–34, often referred to as "young invincibles," initially lagged in sign-ups, posing a challenge to risk pool stability. However, targeted outreach efforts and the availability of catastrophic plans have gradually increased their participation. Conversely, older adults aged 50–64, who are not yet eligible for Medicare, represent a significant portion of ACA enrollees. This group often faces higher premiums due to age-based rating rules but benefits from subsidies that cap their contributions as a percentage of income. For instance, a 60-year-old earning $30,000 annually might pay no more than 8.5% of their income for a benchmark plan, thanks to ACA subsidies.

Income is another critical determinant of ACA coverage. The law’s premium tax credits are designed to make insurance affordable for individuals and families earning between 100% and 400% of the federal poverty level (FPL). For example, a family of four earning up to $100,000 in 2023 could qualify for subsidies, significantly reducing their monthly premiums. However, those earning below 100% FPL often fall into the "coverage gap" in states that did not expand Medicaid, leaving them without affordable options. Conversely, higher-income individuals above 400% FPL face the full brunt of premium costs, which can exceed $1,000 monthly for comprehensive plans, leading some to opt out of coverage altogether.

Ethnicity highlights both progress and persistent disparities in ACA coverage. Hispanic and Black Americans have seen notable gains in insurance rates since the ACA’s implementation, with Hispanic enrollment increasing by over 20 percentage points in some states. However, language barriers, immigration status concerns, and lower average incomes continue to limit access for certain subgroups. For instance, undocumented immigrants are ineligible for ACA plans, while mixed-status families may face confusion about eligibility. Asian Americans, though generally well-insured, show variability based on country of origin and language proficiency. White Americans, while the largest demographic group, have lower uninsured rates overall but still face challenges in rural areas where provider networks are limited.

Practical takeaways for maximizing ACA coverage across demographics include:

- Young adults: Explore catastrophic plans or short-term health insurance if premiums seem prohibitive, but remember these options have limited benefits.

- Older adults: Use the ACA’s age-rating cap (3:1 ratio) to your advantage and consider silver-level plans, which often provide additional cost-sharing reductions.

- Low-income individuals: Check Medicaid eligibility in your state, even if it hasn’t expanded, as some states have alternative pathways to coverage.

- Minority communities: Utilize navigator programs and multilingual resources to overcome enrollment barriers and ensure accurate information.

By addressing these demographic nuances, policymakers and consumers can work toward a more equitable and effective ACA system.

Converting Life Insurance: Understanding the Benefits and Why

You may want to see also

Explore related products

![]()

Impact of Medicaid Expansion: How Medicaid expansion affects ACA enrollment numbers

Medicaid expansion under the Affordable Care Act (ACA) has significantly reshaped the healthcare landscape, particularly in states that adopted it. As of 2023, approximately 15 million Americans have gained Medicaid coverage through expansion, directly influencing ACA enrollment numbers. This policy extends Medicaid eligibility to adults with incomes up to 138% of the federal poverty level, a move that has reduced the uninsured rate in expansion states by an average of 50% since 2014. By broadening the safety net, Medicaid expansion has not only increased overall coverage but also shifted the demographic profile of ACA enrollees, as fewer low-income individuals now rely on Marketplace plans.

Consider the mechanics of this shift: in expansion states, individuals below the 138% threshold are directed to Medicaid rather than ACA Marketplace plans. This has led to a noticeable decline in Marketplace enrollment in these states, as the pool of eligible applicants narrows. For instance, Kentucky, which expanded Medicaid in 2014, saw its uninsured rate drop from 20.4% to 5.5% by 2020, while Marketplace enrollment stabilized at lower levels. Conversely, non-expansion states like Texas and Florida continue to see higher Marketplace enrollment, as low-income residents have no Medicaid alternative, leaving them dependent on subsidized ACA plans.

The impact of Medicaid expansion on ACA enrollment is not just numerical but also financial. By enrolling eligible individuals in Medicaid, states reduce the demand for premium tax credits in the Marketplace, lowering federal spending on subsidies. A 2021 study by the Kaiser Family Foundation estimated that Medicaid expansion saved the federal government $6.2 billion annually in Marketplace subsidies. However, this dynamic also highlights a cautionary note: in non-expansion states, the absence of Medicaid expansion places a heavier burden on the ACA Marketplace, potentially straining its resources and increasing costs for both enrollees and the federal government.

Practical implications for policymakers and consumers are clear. States considering Medicaid expansion should weigh the benefits of reduced uninsured rates and lower federal costs against potential administrative challenges. For individuals, understanding eligibility criteria is crucial: in expansion states, those below 138% of the poverty level should apply for Medicaid, while others can seek ACA Marketplace plans. Tools like the Healthcare.gov eligibility calculator can help navigate these options. Ultimately, Medicaid expansion’s interplay with ACA enrollment underscores the importance of state-level decisions in shaping access to affordable healthcare.

Understanding Dog Insurance: Benefits, Costs, and Why It’s Essential

You may want to see also

Explore related products

![]()

Subsidy Utilization: Percentage of enrollees receiving premium tax credits

A significant portion of Americans with ACA insurance rely on premium tax credits to make coverage affordable. As of 2023, approximately 88% of enrollees in HealthCare.gov states receive these subsidies, reducing their monthly premiums by an average of $533. This staggering figure underscores the critical role subsidies play in expanding access to healthcare, particularly for low- and middle-income households. Without these credits, many would face premiums that consume a prohibitive share of their income, effectively pricing them out of the market.

To understand subsidy utilization, consider the eligibility criteria. Premium tax credits are available to individuals and families earning between 100% and 400% of the federal poverty level (FPL). For a family of four in 2023, this translates to an income range of $29,974 to $119,880. Enrollees must also purchase coverage through the ACA Marketplace and not have access to affordable employer-sponsored insurance. The subsidy amount is calculated based on the cost of the benchmark plan in their area and their income, ensuring premiums remain capped at a certain percentage of their earnings.

One practical tip for maximizing subsidy utilization is to update your income information annually during open enrollment. Life changes—such as a job loss, pay cut, or new dependent—can significantly alter your eligibility and subsidy amount. Failing to report these changes may result in receiving too much or too little assistance, leading to unexpected tax liabilities or higher premiums. Additionally, enrollees should explore cost-sharing reductions (CSRs), which are available to those earning up to 250% of the FPL and further reduce out-of-pocket costs like deductibles and copays.

Comparatively, states that expanded Medicaid under the ACA have lower subsidy utilization rates, as more individuals qualify for free or low-cost coverage through Medicaid. In non-expansion states, however, subsidies become a lifeline for those in the "coverage gap"—individuals earning too much for Medicaid but too little to afford unsubsidized plans. This disparity highlights the importance of state-level policy decisions in shaping access to affordable care.

In conclusion, subsidy utilization is a cornerstone of the ACA’s success in reducing uninsured rates. By understanding eligibility criteria, staying proactive during enrollment, and leveraging additional cost-saving measures, enrollees can fully benefit from these financial aids. Policymakers, meanwhile, must address disparities in access to ensure subsidies remain a viable tool for achieving universal healthcare coverage.

Assignee Signature: Life Insurance Form Essential

You may want to see also

Frequently asked questions

As of 2023, approximately 14.5 million Americans have health insurance through the Affordable Care Act (ACA) marketplaces.

About 4.5% of the U.S. population relies on ACA marketplace plans for their health insurance coverage.

Over 20 million Americans have gained health insurance coverage through Medicaid expansion since the ACA’s implementation.

ACA enrollment numbers have been steadily increasing in recent years, with record highs reported in the 2023 open enrollment period.