Life insurance is a crucial financial product that provides peace of mind and security for individuals and their loved ones. While term life insurance is a popular choice due to its affordability, it has an expiration date, leaving individuals unprotected after a certain period. To address this limitation, individuals can convert their term life insurance into permanent life insurance, ensuring lifelong coverage and offering additional benefits, such as cash value accumulation. This conversion process is often straightforward, bypassing the need for medical exams and lifestyle assessments. However, it's important to carefully consider the reasons for converting, as premiums tend to increase significantly, and partial conversions may be more suitable in certain circumstances. Understanding the specific life insurance products available, such as universal or whole life insurance, and seeking guidance from independent agents, are essential steps in making an informed decision about converting life insurance policies.

| Characteristics | Values |

|---|---|

| Reasons for conversion | To provide for the unexpected needs of loved ones, leave an inheritance for children, or maintain coverage for the entirety of one's life |

| Conversion types | Partial or total conversion, term-to-permanent, term-to-universal, term-to-whole |

| Conversion timing | Within the first few years of the policy, before the end of the term, or before a certain age (e.g., 65, 70, or 75) |

| Conversion costs | Premium payments are likely to be higher, but there is usually no direct cost to convert; some companies offer conversion credits or discounts for the first year |

| Conversion process | Contact the insurance company, discuss details including coverage and cost, finalize, and receive a new policy |

| Conversion privileges | Guaranteed coverage and set premium payments, no evidence of insurability or medical exam required |

Explore related products

What You'll Learn

![]()

To provide for the unexpected needs of loved ones

Life insurance is a thoughtful and appreciated gesture that helps prepare your loved ones for the unexpected. It is designed to help with growing financial commitments like day-to-day expenses, a mortgage, debt payments, and even college costs for your kids.

Term life insurance is a popular choice for those looking to save money upfront. It is the most affordable and simple type of life insurance coverage, allowing you to choose the term length and benefit amount. However, it eventually terminates. For example, parents often obtain a life insurance policy that lasts until their children reach legal age or graduate from college.

If you find yourself unexpectedly caring for a family member, converting from term to whole life insurance can help provide for their long-term needs. Whole life insurance offers lifelong coverage and a cash value component. By converting, you can maintain your coverage for life and protect your family financially.

When considering a conversion, it is important to check if your term life insurance is convertible and when the conversion option is available. Some insurers allow conversion throughout the duration of the contract, while others only offer it during the first few active years of the policy. Additionally, there may be a maximum age requirement, such as not being able to convert if you are over 65 years old.

You can also choose between a partial or total conversion. A partial conversion results in a smaller death benefit and lower premiums, while a total conversion provides a higher death benefit but at a greater cost. It is essential to weigh your options and seek guidance from a financial advisor to make an informed decision.

Term Rider: Life Insurance's Essential Add-On

You may want to see also

Explore related products

![]()

To leave an inheritance for children

Life insurance is a way to leave an inheritance for your children, providing financial security and peace of mind. It ensures that your loved ones will be taken care of even after you're gone. In a NerdWallet study, leaving an inheritance was the top reason for millennials to buy life insurance.

When you purchase life insurance, you choose the amount of coverage you want, ensuring your family can maintain their standard of living. This is especially important if you have young children who are financially dependent on you. By securing a life insurance policy, you can guarantee that your children will have the financial resources they need to go to college and pursue their goals.

Life insurance can also help with mortgage payments, ensuring your family can keep their home. For example, consider a family with a $500,000 mortgage and two young children. They may opt for $1,000,000 of coverage to ensure they can pay off their home and provide for their children's education. By layering term life insurance with a guaranteed universal life policy, they can ensure both immediate coverage and a future inheritance.

Additionally, life insurance can shield your children from hefty estate taxes. If your estate is valued above a certain threshold, it may be subject to taxes, which your heirs must pay. Life insurance can help cover these taxes, ensuring your children receive the full benefit of their inheritance. It's also worth noting that life insurance payouts are typically tax-free, further maximizing the financial benefit for your children.

Finally, life insurance allows you to spend your retirement savings without guilt. Many retirees live frugally to preserve their savings as an inheritance. With life insurance, you can enjoy your retirement and still leave a legacy. Guaranteed universal life insurance (GUL) is a popular option, offering fixed premiums and coverage up to a specified age, ensuring you don't outlive your policy.

How to Change Your OPM Life Insurance Policy

You may want to see also

Explore related products

![]()

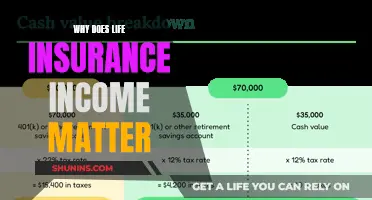

To access cash during retirement

If you have a permanent life insurance policy, it may have accumulated a significant amount of funds in its cash value. This money can be used to supplement your retirement income. Permanent life insurance policies are typically more expensive than term life insurance policies because they provide coverage for your entire life and can build cash value. This cash value grows over time as you pay your premiums, with a portion of the premiums going into a fund.

There are several ways to access the cash value in a universal or whole life policy. One option is to cancel the policy entirely and take the surrender value cash payment. However, this comes with the drawback of losing your life insurance coverage, and the cash received will be lowered by any fees taken out. Surrender fees can be significant, especially with a newer policy, so surrendering a policy before retirement age should be a last resort.

Another option is to take out a life insurance loan against your cash value balance. Insurers often offer loans once policyholders have paid a certain amount into the policy. Life insurance loans can be a low-cost, flexible way to access cash value while keeping your coverage in place. There is no need for credit or income checks, as the loan is guaranteed by your policy. However, there is a charge to borrow, and the amount owed will grow over time due to interest charges. If you don't pay back the loan, the amount and interest will be deducted from the death benefit paid to your beneficiaries.

You can also withdraw money directly from the cash value. The amount available differs based on the type of policy and the company issuing it. Withdrawals are not taxable up to your policy basis, as long as your policy is not classified as a modified endowment contract (MEC). However, withdrawals that reduce your cash value could also reduce your death benefit, potentially compromising your family's financial future.

Finally, you can sell your life insurance policy through a life settlement or viatical settlement. This involves selling your policy to a third party for more than the cash surrender value but less than the death benefit. Once the sale is complete, the buyer becomes responsible for paying your insurance premiums and maintenance fees for the rest of your life, after which they receive the policy's death benefit.

Life Insurance Tax: What Employees Need to Know

You may want to see also

Explore related products

![]()

To avoid a medical exam

Life insurance without a medical exam, also known as "no-exam life insurance" or "simplified-issue life insurance", is designed to offer a more convenient and streamlined application process for individuals who prefer to avoid medical exams or have specific health concerns. This type of insurance is ideal for those who need coverage quickly, such as those with a history of good health or known health issues who are looking to provide support for funeral and burial expenses on a rapid timeline.

No-exam life insurance allows individuals to skip the medical exam that is typically required when applying for a life insurance policy. The medical exam helps insurance companies assess an applicant's overall health and evaluate potential risks associated with providing coverage. It may include measuring blood pressure, heart rate, height, and weight, as well as taking blood and/or urine samples. For older individuals, it may also involve additional tests such as an electrocardiogram (EKG) or treadmill test.

By opting for no-exam life insurance, individuals can expedite the process of obtaining life insurance, especially if they have a general idea of how long they will need coverage for. This type of insurance may also be beneficial for those with a fear of needles or those who simply prefer a hassle-free experience without the waiting period associated with traditional life insurance.

It is important to note that no-exam life insurance typically comes with a cap on the coverage amount and may be more expensive due to the higher risk taken on by the insurer. Most companies will still require applicants to fill out a health questionnaire, and the coverage amounts and policy options may be more limited. However, no-exam life insurance can provide a valuable alternative for those who may have trouble qualifying for traditional life insurance due to pre-existing medical conditions or high-risk occupations.

Investor-Originated Life Insurance: What's the Deal?

You may want to see also

Explore related products

![]()

To maintain insurability

Life insurance conversion allows individuals to maintain their insurability by converting their group life insurance policy to an individual policy, without providing evidence of insurability. This means that they can avoid medical evaluations or health screenings, which is especially beneficial if their health has changed or deteriorated since enrolling in the original policy.

The conversion privilege is a contract provision that allows the insured to switch to a different form of coverage without demonstrating evidence of insurability. This option is particularly valuable for those who have experienced serious health complications since their original policy was issued, as it allows them to maintain coverage without facing higher premiums due to their changed health status.

The conversion period typically lasts for a limited time after leaving the group, with a time frame of 30 to 60 days being common. During this time, individuals can secure a new policy without undergoing a medical exam or answering health questions. If this period is missed, the individual may lose the option to convert their coverage and may need to provide health information to obtain new coverage.

In addition to maintaining insurability, life insurance conversion can offer other benefits. For example, some insurers offer a conversion credit, which is a premium reduction to offset the significant price increase for a permanent policy. This discount usually applies only for the first year of the conversion. Life insurance conversion also provides flexibility, allowing individuals to change their insurance coverage as their needs evolve. For instance, someone who initially needed coverage for a specific period might later decide to convert to a permanent policy.

Life Insurance Cancellation: Are Refunds Possible?

You may want to see also

Frequently asked questions

Converting term life insurance to whole life insurance can help provide for the unexpected needs of loved ones. By converting, you can maintain your coverage for the entirety of your life and protect your family financially.

Permanent life insurance policies have additional benefits such as cash value, a policy loan option, and coverage that won't expire. These additional components often aid in retirement and estate planning.

First, check if your term life insurance is convertible and when the conversion is available. Then, choose the type of permanent life insurance you want and calculate the new policy cost. Finally, decide whether to do a partial or total conversion of your existing policy.

It's important to understand the ins and outs of converting coverage and to consider all of your options. Speak with an independent agent before modifying your policy as some changes cannot be reversed. Additionally, consider the cost of conversion as premiums are likely to be higher.