Mortgage insurance is an additional cost built into your monthly payments to the lender. It is required for loans backed by the Federal Housing Administration (FHA) and the U.S. Department of Agriculture (USDA). The insurance lowers the risk to the lender of offering a loan to you and makes it easier for you to qualify for a loan with a lower down payment. The insurance is not to be confused with homeowners insurance, which protects the homeowner in case of damage to the house or belongings.

| Characteristics | Values |

|---|---|

| Who does mortgage insurance protect? | The lender, in the event that the borrower falls behind on payments. |

| Who needs mortgage insurance? | Homebuyers who want to qualify for a loan with a down payment as low as 3%. |

| Types of mortgage insurance | Private mortgage insurance (PMI), mortgage insurance premiums (MIP), single-premium mortgage insurance, lender-paid mortgage insurance, split-premium mortgage insurance, borrower-paid mortgage insurance, and lender-paid mortgage insurance. |

| How much does mortgage insurance cost? | Typically between 0.1% to 2% of the loan balance per year, but can vary depending on credit score, down payment amount, loan amount, and loan term. |

| How often is mortgage insurance paid? | Monthly, upfront at closing, or both, depending on the type of mortgage insurance and the lender. |

| Can mortgage insurance be cancelled? | Yes, under certain circumstances. For PMI, it can be cancelled when the borrower reaches 20%-22% equity in their home. For MIP on FHA loans, it can be cancelled after 11 years if the down payment was more than 10%. |

| Are there alternatives to mortgage insurance? | Yes, some lenders may offer a "piggyback" second mortgage or other options, but it's important to compare the total cost before making a decision. |

Explore related products

What You'll Learn

![]()

Mortgage insurance is paid monthly

Borrower-paid PMI is the most common type of PMI. With this type, your insurance payment is added to your monthly mortgage payment. You can also pay PMI upfront or through a combination of an upfront fee and a lower monthly premium. Lender-paid PMI is when the lender pays the insurance with a lump sum when the loan is closed. In return, the borrower accepts a higher interest rate on their mortgage.

Mortgage insurance premiums (MIP) are for borrowers using loans backed by the Federal Housing Administration (FHA). FHA loans require an upfront premium of 1.75% and an ongoing monthly premium. MIP is required on all FHA loans, regardless of the down payment size. If you put down more than 10%, you pay MIP for 11 years.

USDA loans, guaranteed by the U.S. Department of Agriculture, and VA loans, backed by the U.S. Department of Veterans Affairs, don't require mortgage insurance. However, they have borrower-paid fees to protect lenders. USDA loans are zero-down-payment loans for rural home buyers. USDA loans have an upfront guarantee fee of 1% of the loan amount and an annual fee paid every year for the life of the loan. The annual fee is divided into monthly installments. VA loans require an upfront funding fee of up to 3.3% of the loan amount.

Mechanical Breakdown Insurance: Is GEICO's Offering Valuable?

You may want to see also

Explore related products

![]()

It protects the lender, not the borrower

Mortgage insurance is an insurance policy that protects the lender or titleholder if the borrower defaults on payments, passes away, or is otherwise unable to meet the contractual obligations of the mortgage. It is not designed to protect the borrower.

Mortgage insurance is typically required for borrowers who make a down payment of less than 20% of the purchase price of the home. It is also usually required for Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans. The insurance lowers the risk to the lender of making a loan, allowing them to offer loans to borrowers who might not otherwise qualify. However, it increases the cost of the loan for the borrower.

Private mortgage insurance (PMI) is a type of mortgage insurance that lenders may require borrowers to purchase if they make a small down payment. PMI is arranged by the lender and provided by private insurance companies. It protects the lender against losses caused by borrowers failing to make loan payments. If a borrower falls behind on their mortgage payments, PMI does not protect them, and they can still lose their home through foreclosure.

Mortgage insurance is typically paid monthly, with the premium added to the borrower's monthly mortgage payment. In some cases, there may also be an upfront cost paid as part of the closing costs. Under certain circumstances, borrowers may be able to cancel their mortgage insurance once they have paid off a significant portion of the loan.

While mortgage insurance protects the lender, it is important to note that borrowers may still have other protections in place, such as mortgage protection life insurance, which can provide payouts to either the lender or the heirs of the borrower in the event of the borrower's death.

Fire and Theft Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

It's required for Federal Housing Administration loans

Mortgage insurance is typically required for borrowers who make a down payment of less than 20% on their home purchase. The duration for which this insurance needs to be paid depends on various factors, including the type of loan, the size of the down payment, and the lender.

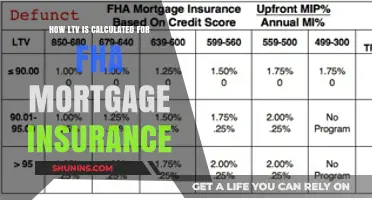

For Federal Housing Administration (FHA) loans, mortgage insurance is indeed required. FHA loans are government-backed mortgages that are popular among first-time homebuyers due to their low down payment requirements and flexible credit score requirements. When obtaining an FHA loan, borrowers are required to pay an upfront mortgage insurance premium (UFMIP) at the time of closing. This amount is typically 1.75% of the base loan amount and can be financed into the mortgage.

In addition to the upfront payment, borrowers with FHA loans must also pay monthly mortgage insurance premiums (MIP). The duration for which MIP must be paid varies depending on the loan-to-value ratio (LTV) and the length of the mortgage. For FHA loans with terms of 15 years or less and an LTV ratio of less than or equal to 90%, the MIP will be required for at least 11 years but may be removed after that if certain conditions are met. For FHA loans with terms longer than 15 years and an LTV greater than 90%, the MIP will generally be required for the life of the loan.

It's important to note that FHA loans with terms of 15 years or less and an LTV greater than 90% will have the MIP removed after 11 years, but only if the loan was originated after June 3, 2013. For loans originated before this date, different rules may apply. Borrowers with FHA loans should carefully review their loan documents or consult their lender to understand the specific requirements for their mortgage insurance.

Mortgage Insurance: When Does it End?

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI) is for conventional loans

Private mortgage insurance (PMI) is a type of insurance that is typically required for conventional loans when the buyer makes a down payment of less than 20% of the home's value. It is an additional cost for borrowers, but it also offers potential benefits. For example, PMI can help borrowers secure a mortgage with a lower down payment and increase their loan eligibility. It is important to note that PMI protects the lender and not the borrower in case of default. Therefore, if the borrower falls behind on their mortgage payments, PMI will not protect them from foreclosure.

PMI can be removed from monthly payments once the borrower has achieved 20% equity in their home or has paid off enough of the loan balance, typically below 80% of the purchase price of the home. Federal law dictates that lenders must automatically terminate PMI when the loan-to-value (LTV) ratio drops to 78% or when the borrower is one month past the midpoint of their loan term. Borrowers can also request to cancel PMI when their mortgage balance reaches 80% of their home's value.

There are different types of PMI, each with its own payment structure. The most common type is borrower-paid PMI (BPMI), where the borrower pays the insurance as part of their monthly mortgage payment. Lender-paid PMI (LPMI) is another option, where the lender covers the PMI costs, but the borrower pays a higher interest rate on the loan. Single-premium PMI involves paying a one-time upfront premium at closing, either in full or rolled into the loan for a higher balance. Split-premium PMI blends elements of borrower-paid and single-premium PMI, where the borrower pays a larger upfront fee and the remainder with their monthly mortgage payment.

The cost of PMI depends on several factors, including the loan amount, down payment size, credit score, and loan type (fixed or adjustable-rate). It is typically calculated as a percentage of the mortgage loan amount, ranging from 0.58% to 1.86% annually or $30 to $70 per $100,000 borrowed. Before agreeing to a mortgage with PMI, borrowers should carefully consider the different options and calculate the total costs to determine the best deal for their financial situation.

Should You Call Your Insurance?

You may want to see also

Explore related products

![]()

You can cancel PMI when you've paid off some of your loan

Mortgage insurance, also known as Private Mortgage Insurance (PMI), is a type of policy that protects the lender in case the borrower defaults on their loan. While it does not directly benefit the borrower, PMI does give lenders the ability to issue mortgages based on down payments of less than 20%. This insurance is usually paid monthly and can increase the cost of the loan.

Under certain circumstances, you can cancel your PMI. Once you've paid off some of your loan, you may be eligible to cancel your mortgage insurance. This is known as ending PMI and can reduce your monthly costs. You can request PMI cancellation when your mortgage balance reaches 80% of the original value of your home. This is known as reaching 20% equity.

To estimate the amount your mortgage balance needs to reach to be eligible for PMI cancellation, multiply your home's purchase price by 0.80. You can also pay off your mortgage earlier by making biweekly payments, an additional payment each year, or a lump-sum payment at any time. It's important to note that you must be current on your monthly payments for PMI cancellation to occur.

Additionally, you can request PMI cancellation ahead of the scheduled date if you have made additional payments that reduce the principal balance of your mortgage to 80% of the original value of your home. This can be achieved through an increase in market value or home improvements that increase your home's value.

If you have an FHA loan, you pay a mortgage insurance premium (MIP) which has a similar function to PMI but is paid no matter how much you put down on the loan. In many cases, you will pay it for the life of the loan. However, if you put down at least 10%, you will only pay MIP for 11 years.

Red Light Tickets: Insurance Reporting Requirements

You may want to see also

Frequently asked questions

Mortgage insurance protects the lender in case the borrower defaults on the loan. It also helps homebuyers get an affordable, competitive interest rate and qualify for a loan with a lower down payment.

The cost of mortgage insurance varies depending on the type of loan, whether it’s government-backed, and who pays the premium. Private mortgage insurance (PMI) is typically used for conventional loans and can range from 0.1% to 2% of the loan balance per year. For Federal Housing Administration (FHA) loans, mortgage insurance premiums (MIP) are required and include an upfront premium of 1.75% and an ongoing monthly premium.

You typically pay mortgage insurance monthly for several years, until you've paid off enough of your loan to cancel it. If you put down more than 10% on an FHA loan, you'll pay MIP for 11 years.

Yes, you can avoid paying for mortgage insurance by making a larger down payment (typically 20%) or choosing a loan that doesn't require it, such as a VA loan backed by the Department of Veterans Affairs.