Private mortgage insurance (PMI) is a type of insurance that is required when taking out a conventional loan with a down payment of less than 20%. It protects the lender in the event that the borrower defaults on their loan. The cost of PMI is typically between $30 to $70 per month for every $100,000 borrowed and is calculated based on the borrower's credit score and the risk they present to the lender. While PMI can increase the cost of a loan, it also makes it possible for buyers with limited cash reserves to qualify for a loan. In some cases, a gift of equity from a family member can be used as a down payment, allowing buyers to avoid the need for PMI. However, if the gift of equity is too large, the seller may be subject to gift taxes.

| Characteristics | Values |

|---|---|

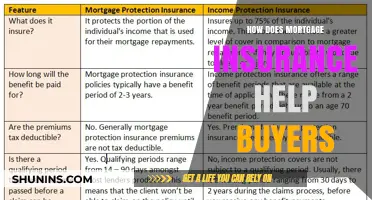

| What is a gift of equity? | When someone, usually a family member, sells a home to buyers for a price below market value. |

| Who can give a gift of equity? | Family members like parents, grandparents, cousins or in-laws. |

| Who can receive a gift of equity? | Family members like children or other relatives. |

| What is the tax exemption limit for a gift of equity? | Under the Internal Revenue Service (IRS) rules, an individual can provide a gift of up to $17,000 in cash or property to another individual in a year without triggering gift taxes. |

| What is the tax exemption limit for a married couple? | A married couple can provide a gift of equity of $34,000 total ($17,000 each from each parent) without triggering gift taxes. |

| What is Private Mortgage Insurance (PMI)? | A type of mortgage insurance you might be required to buy if you take out a conventional loan with a down payment of less than 20% of the purchase price. |

| Who does PMI protect? | PMI protects the lender, not the borrower, against any losses if the borrower stops making payments or fails to repay their conventional loan. |

| Who has to pay for PMI? | Borrowers who purchase a home with less than a 20% down payment are typically required to pay for mortgage insurance. |

| How much does PMI cost? | PMI costs between $30 to $70 per month for every $100,000 borrowed. |

| How is the cost of PMI calculated? | The cost of PMI is calculated based on the risk presented to the lender, the down payment amount, the loan amount, and the borrower's credit score. |

| How can you avoid paying PMI? | By making a 20% down payment or opting for a piggyback loan or lender-paid mortgage insurance. |

| When can you cancel PMI? | You can request to cancel PMI when you reach 20% equity in your home, and the lender must automatically cancel it once the principal balance reaches 78% of the original home value or at the midpoint of the amortization schedule. |

Explore related products

What You'll Learn

![]()

Private mortgage insurance (PMI) is required when a down payment is less than 20%

Private mortgage insurance (PMI) is a type of insurance that protects the lender in the event that the borrower defaults on their mortgage. It is required when the borrower takes out a conventional loan with a down payment of less than 20% of the purchase price. This is because borrowers with less equity are more likely to have issues paying off their mortgage, and the lender is providing the upfront cash for the home, so they risk taking a loss if the borrower stops making payments.

PMI can be costly for the borrower, ranging from $30 to $70 per month for every $100,000 borrowed. The cost is typically added to each mortgage payment and is based on the borrower's credit score and the risk they present to the lender. A larger down payment and a higher credit score will usually result in a lower PMI cost.

There are a few ways to avoid paying PMI. One way is to make a down payment of at least 20%, which can be challenging for many homebuyers, especially in high-priced metropolitan areas. Another option is to use a piggyback loan, where the borrower takes out a second mortgage to make up the difference between their down payment and the 20% requirement. However, this second mortgage will have its own separate interest rate, which may be substantially higher.

A gift of equity from a family member can also be used to make a down payment of at least 20% and avoid PMI. This is when a family member sells their home to the buyer for below market value, allowing them to purchase the home without having to put down a large sum of cash. Most lenders allow buyers to use a gift of equity as their down payment, but it is important to note that sellers may incur gift taxes if they gift too much equity.

Overall, while PMI can increase the cost of a loan, it allows borrowers with limited cash reserves to qualify for loans they may not have otherwise been able to obtain.

Collateral Protection Insurance: House Insurance Explained

You may want to see also

Explore related products

![]()

PMI costs are calculated based on the risk to the lender

Private mortgage insurance (PMI) is a type of insurance that protects the lender in case the borrower defaults on their mortgage. It is required when the borrower takes out a conventional loan with a down payment of less than 20% of the purchase price. The cost of PMI is typically between $30 to $70 per month for every $100,000 borrowed, but it can vary depending on several factors. These factors include the size of the mortgage loan, the down payment amount, the borrower's credit score, and the type of mortgage.

The larger the mortgage loan, the higher the PMI cost will be. This is because a larger loan poses a greater risk to the lender, as they stand to lose a larger investment if the borrower defaults. A smaller down payment also represents a higher risk for the lender, as it means the borrower has less equity in the home and is more likely to have issues with repayment. As a result, borrowers with smaller down payments will typically pay more for PMI.

The borrower's credit score also plays a significant role in determining the cost of PMI. A higher credit score indicates lower risk to the lender, which results in a lower PMI rate. Borrowers with excellent credit can expect to pay less for PMI, while those with lower credit scores may be charged a higher rate.

The type of mortgage can also impact the cost of PMI. Adjustable-rate mortgages (ARMs) are considered riskier for lenders because the interest rate can fluctuate, making it harder to predict future mortgage payments. As a result, PMI tends to be more expensive for ARMs compared to fixed-rate loans, which offer more stability and predictability.

In addition to these factors, there may be other considerations that lenders take into account when determining PMI costs. It is important for borrowers to understand the specific requirements and options offered by their lender, as PMI policies and payment methods can vary. By considering the risk factors involved and making informed decisions, borrowers can work towards obtaining favourable terms for their mortgage loans.

American Family vs. Farmers Insurance: A Comprehensive Comparison Guide

You may want to see also

Explore related products

![]()

PMI can be paid monthly or annually

Private mortgage insurance, or PMI, is a type of insurance that protects the lender in the event that the borrower defaults on their payments. It is required when a homebuyer puts down less than a 20% down payment.

PMI can be paid in several ways, including monthly or annually. The monthly premium is usually added to your monthly mortgage payment and is based on a percentage of your loan balance. The cost of PMI varies based on insurance rates and the borrower's credit score, but is usually between 0.0022% to 0.025% of the principal loan amount, or $30 to $70 per month for every $100,000 borrowed.

You may also have the option to pay yearly, but yearly payments are usually non-refundable, even if you sell the home. Some PMI policies may also allow you to pay the entire PMI coverage in cash upfront at closing or finance the amount into your loan principal. This option may be a good choice if you have the cash available and want to minimise your monthly housing expenses.

Another option is lender-paid PMI, where you agree to a higher mortgage interest rate and, in exchange, the lender pays the PMI premium on your behalf. Alternatively, you can choose a split premium, where you pay a portion of the PMI upfront and add the remaining premium to your monthly mortgage payments.

It's important to note that PMI is not the same as homeowners insurance, which provides financial protection from damages to your home. PMI is an additional cost that protects the lender, not the borrower. Additionally, PMI can be removed from your monthly payments once you have achieved 20% equity in your home or paid off your loan balance to below 80% of the purchase price.

Term Life Insurance: Worth the Investment?

You may want to see also

Explore related products

![]()

Buyers can avoid PMI with a gift of equity

Private mortgage insurance, or PMI, is a policy that protects the lender against any losses if the borrower stops making payments or fails to repay their conventional loan. Borrowers who purchase a home with less than a 20% down payment are typically required to pay for mortgage insurance. A gift of equity is a way for a seller to help buyers, usually family members, purchase a home. The seller agrees to sell their home below market value, allowing the buyer immediate access to more equity than they have paid for.

A gift of equity can be used as a down payment, saving the buyer the hassle of scraping together enough money for this payment. Buyers don't have to pay taxes on a gift of equity. However, if the gift is too large, the seller may have to fill out a gift tax form when filing returns. Under the Internal Revenue Service (IRS) rules, an individual can provide a gift of up to $17,000 to any other individual in a year before they have to file gift taxes.

If the gift of equity is large enough, buyers might not have to pay PMI. For example, if a buyer wants to purchase a home from a family member worth $600,000, a 20% down payment is $120,000. If the family member sells the home for $550,000, the buyer now only needs to make a down payment of $70,000 (about 11.7%) to cover the 20% down payment. Since that's 20% of the market value, the buyer could qualify for a conventional loan with no PMI, assuming their credit score and financial circumstances are acceptable.

A gift of equity letter is required by lenders, which should include the total amount of the gift of equity and explain that the buyer is not required to pay back this gift. The letter should also explain the relationship between the owners and buyers and include the address of the property.

Chubb Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Lenders may offer PMI options with varying timeframes

Private mortgage insurance (PMI) is a type of insurance that you may be required to purchase if you take out a conventional loan with a down payment of less than 20% of the purchase price. PMI protects the lender if you stop making payments on your loan. The cost of PMI varies based on insurance rates and the borrower's credit score, but is usually between $30 to $70 per month for every $100,000 borrowed.

Some PMI policies may allow you to pay the entire PMI coverage in cash at closing or finance the amount into your loan principal. You can also request to cancel PMI when you reach 20% equity in your home. Federal law allows you to request cancellation when your loan-to-value (LTV) ratio drops to 80%, and lenders must automatically end PMI when the LTV ratio drops to 78%.

It is important to ask lenders about the PMI choices they offer and to calculate the total costs over different timeframes to determine the best option for your financial situation.

Pet Insurance: Is Nationwide's Plan Worth the Cost?

You may want to see also

Frequently asked questions

A gift of equity is when someone, usually a family member, sells a home to buyers for a price below market value. It is a way for owners to gift real estate to their children or other relatives even if the buyers don’t have enough cash to cover a down payment.

PMI is a type of insurance that protects the lender in case the borrower defaults on their mortgage. Buyers who are gifted a large chunk of equity may still need to apply for a mortgage loan. PMI costs are calculated based on the risk presented to the lender and the likelihood of defaulting on the mortgage.

The simplest way to avoid paying PMI is to make a 20% down payment on a conventional loan. This gives you an 80% loan-to-value (LTV) ratio, which means you have a lower financial risk for the lender.

Another way to avoid PMI is to take a piggyback loan, which is an immediate second mortgage to make up the difference between your down payment and the 20% requirement. You can also choose a lender-paid mortgage insurance plan, where the lender covers the cost of your PMI in exchange for a higher interest rate.