The length of time you'll be paying mortgage insurance depends on several factors, including the type of loan and how much of a down payment you've made. For instance, if you've made a larger down payment of 15% on a conventional loan, you may only pay mortgage insurance for about 5 years. However, if you've made a smaller down payment of 5%, it could take up to 9 years to reach the point where mortgage insurance can be cancelled. In the case of FHA loans, mortgage insurance may be required for the full term of the loan, although there are certain circumstances where it can be removed after 11 years. It's important to note that lenders may have different requirements for removing mortgage insurance, so it's always a good idea to consult with a mortgage expert to understand the specific conditions of your loan.

| Characteristics | Values |

|---|---|

| When to pay mortgage insurance | When the down payment is below 20% |

| Private Mortgage Insurance (PMI) | Drops off once the loan balance reaches 78% of the original purchase price |

| FHA Mortgage Insurance | Remains for the life of the loan, but can drop off after 11 years |

| USDA and VA Mortgage Insurance | Remains for the life of the loan |

| Cancelling PMI | Request cancellation in writing once the 20% threshold is met |

| Lender Requirements | May require a formal appraisal of the home prior to cancellation |

| Automatic Cancellation | Occurs at 78% loan-to-value ratio (LTV) or 22% of the loan paid off |

| Shorter PMI Period | Larger down payment, home price appreciation, prepayments on mortgage |

| Conventional Loans | PMI cancellation at 80% LTV if timely payments and loan held for several years |

| FHA Loans | Cannot be cancelled if made after June 2013 with less than a 10% down payment |

| FHA Loans with 10% Down Payment | Can be cancelled after 11 years |

| Lender-Paid Mortgage Insurance | Cannot be cancelled |

Explore related products

What You'll Learn

![]()

It depends on the loan type

The number of years you have to keep mortgage insurance depends on the type of loan you have. For conventional loans, Private Mortgage Insurance (PMI) will typically be removed once the loan balance reaches 78% of the original purchase price. This usually happens when you've paid off 22% of the loan, but it can also depend on how much you initially put down and how much equity you have. For example, if you start with a 15% down payment, you may only pay mortgage insurance for around 5 years, whereas a 5% down payment will likely take closer to 8 years to reach the necessary 80% Loan-to-Value (LTV) level.

Mortgage insurance on Federal Housing Administration (FHA) loans often requires insurance for the full term of the loan, or at least 11 years. If you put less than 10% down on an FHA loan, you may not be able to cancel the insurance at all. Similarly, loans from the Department of Veterans Affairs (VA) and the United States Department of Agriculture (USDA) will usually require mortgage insurance for the life of the loan.

It's important to note that there are different types of mortgage insurance policies, such as Lender-Paid Mortgage Insurance, which cannot be cancelled. Additionally, some lenders may require a formal appraisal of your home before cancelling the PMI, and this process can take several months.

Farmers Insurance Umbrella: Comprehensive Protection for Your Assets

You may want to see also

Explore related products

![]()

FHA loans and mortgage insurance

FHA loans are mortgages that are backed by the Federal Housing Administration (FHA). They are known for having more lenient standards for borrowers compared to other mortgage options, such as credit score and down payment requirements.

FHA loans require borrowers to pay a mortgage insurance premium (MIP), which is an additional payment made to secure the mortgage loan. This insurance provides protection for the lender in the event that the borrower defaults on their loan. It is important to note that FHA MIPs do not protect the borrower but instead safeguard the lender against potential losses.

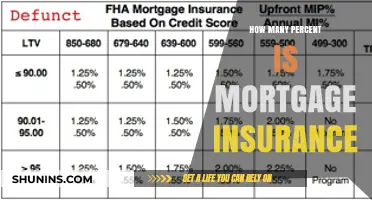

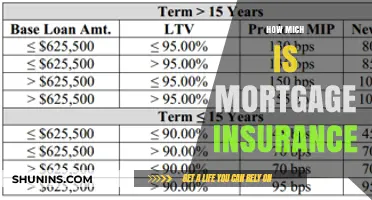

The cost of FHA mortgage insurance premiums varies depending on factors such as the loan amount, the size of the down payment, and the loan term. Borrowers are typically required to pay two types of FHA MIP: an upfront premium and an additional annual payment. The upfront premium is typically set at 1.75% of the loan amount, while the annual MIP varies based on specific loan characteristics.

The duration of FHA MIP payments depends on the loan term and the down payment. For a 30-year FHA loan, if the down payment is 3.5%, borrowers will generally pay MIP for the entire loan term. However, if the down payment is at least 10%, the MIP will typically be required for the first 11 years of the loan. It is important to note that FHA loan guidelines can change, and borrowers should consult with mortgage experts for the most up-to-date information.

FHA loans provide an attractive option for homebuyers who may not have saved a substantial amount for their down payment or have lower credit scores. While the FHA MIP adds to the overall cost of the loan, it enables borrowers to qualify for a mortgage with more flexible requirements.

Federal Long-Term Insurance: Worth the Effort?

You may want to see also

Explore related products

![]()

Conventional loans and PMI

Private mortgage insurance (PMI) is a type of insurance that you might need to buy if you take out a conventional loan with a down payment of less than 20% of the purchase price. It is an additional monthly cost that is rolled into your mortgage payment and protects the lender in case of foreclosure. It is calculated as a percentage of your mortgage loan amount, ranging from 0.58% to 1.86% annually. The cost of PMI depends on factors such as your down payment amount, credit score, mortgage amount, and mortgage type.

Lenders sometimes offer conventional loans with smaller down payments that do not require PMI, but these usually come with a higher interest rate. If you are considering a conventional loan and want to avoid PMI, you can take out a piggyback loan, which involves making a down payment of around 10% and using a second mortgage to pay the remaining 10% of the 20% down payment. However, this option comes with the added financial burden of a second mortgage and a higher interest rate.

To cancel PMI on a conventional loan, you typically need to reach 20% equity in your home or pay off your loan balance to less than 80% of the original value. At this point, you can request that your lender evaluates PMI termination, and they may require a formal appraisal of your home. It is important to review the terms of your loan, as some lenders may automatically cancel PMI once you reach 22% equity or when the loan balance reaches 78% of the original purchase price.

It is worth noting that PMI requirements and removal processes may vary depending on the lender's standards and the specific type of conventional loan you have. Therefore, it is advisable to consult your lender and seek expert advice to understand the specific requirements and options available for your loan.

Self-Defense Insurance: Necessary Protection or Wasteful Spending?

You may want to see also

Explore related products

![]()

How to stop paying PMI

Private mortgage insurance (PMI) is an additional expense on top of your monthly mortgage payment. It is there to protect the lender in case you default on the loan. It does not directly benefit the borrower, so it is financially beneficial to stop paying for PMI as soon as possible.

Wait for automatic removal

Your lender will automatically remove PMI once you've paid down enough of your mortgage. This usually happens when your mortgage balance reaches 78% of the original purchase price or the mortgage hits the halfway point of the loan term, such as the 15th year of a 30-year mortgage.

Request early cancellation

You can ask your mortgage servicer to cancel PMI once your mortgage balance reaches 80% of your home's value at the time you bought it. This is known as your loan-to-value ratio (LTV). You can calculate your LTV by dividing your loan balance by the original purchase price or using an LTV calculator. Make a written request to your mortgage servicer several months before your mortgage is scheduled to hit 80% LTV.

Get a reappraisal

If you've noticed rising prices in your area or have completed home improvement projects, you could have over 20% equity in your home even if you haven't been making extra mortgage payments. Contact your loan servicer and request a formal appraisal of your home. If your equity is above 20%, your lender may cancel your PMI. However, you may need to pay for the appraisal.

Refinance your mortgage

Refinancing your mortgage can be a way to get rid of PMI. Whether you'll need to pay for PMI on the new loan will depend on your home's current value and the principal balance of the new mortgage. You can likely get rid of PMI if your equity has increased to at least 20% and you don't use a cash-out refinance.

Report Your Non-Smoking Status to Insurance: Save Money

You may want to see also

Explore related products

![]()

Lender-paid mortgage insurance

LPMI is often cheaper than private mortgage insurance (PMI) on a monthly basis, but it may cost more over the life of the loan. LPMI is also more difficult to cancel than PMI. While PMI can be cancelled once the borrower has paid off 20% of the loan, LPMI remains in effect for the life of the loan, unless the borrower refinances.

LPMI is a good option for borrowers who want to keep their monthly payments affordable, but it is important to consider the long-term costs. LPMI may be the best option in terms of both short- and long-term costs, especially if the borrower can get rid of PMI sooner than scheduled, for example, by prepaying their mortgage or getting a reappraisal.

It is also important to note that LPMI is not a separate line item on monthly bills, so it may not be immediately clear how much the borrower is paying for LPMI. Borrowers should also be aware that the only ways to get rid of LPMI are to refinance or pay off the loan.

Upgrading Your Engine: Should You Inform Your Insurer?

You may want to see also

Frequently asked questions

The number of years you will have to keep paying mortgage insurance depends on several factors. The type of loan you have taken out will determine whether you can remove mortgage insurance under particular terms. For example, FHA and USDA loans often require mortgage insurance for the full term of the loan, whereas conventional loans typically allow for the removal of mortgage insurance. The size of your down payment will also influence how long you will pay mortgage insurance. The larger the down payment, the shorter the time period in which you will pay mortgage insurance.

You can stop paying PMI once you have paid off 20% of the loan. You will need to write a letter to your lender requesting that the PMI be cancelled and they may also require a formal appraisal of the home prior to its cancellation.

Mortgage insurance, also known as mortgage guarantee or home-loan insurance, is an insurance that protects the lender in the case of a foreclosure. It is an additional expense on top of your monthly mortgage payment and is usually required by the lender if your down payment on a conventional loan is less than 20% of the home's value.