Georgia faces a significant challenge in ensuring healthcare access for all its residents, as a notable portion of its population remains uninsured. According to recent data, approximately 12% of Georgians lack health insurance, translating to over 1.2 million people without coverage. This issue disproportionately affects low-income individuals, communities of color, and those in rural areas, where access to affordable healthcare options is limited. Factors such as the state’s decision not to expand Medicaid under the Affordable Care Act, high premiums, and gaps in employer-based coverage contribute to this persistent problem. Addressing the uninsured rate in Georgia is critical to improving public health outcomes and reducing disparities across the state.

| Characteristics | Values (2022) |

|---|---|

| Total Uninsured Population in Georgia | Approximately 1.4 million |

| Uninsured Rate | 12.8% |

| Uninsured Children (Ages 0-18) | 3.8% |

| Uninsured Adults (Ages 19-64) | 15.3% |

| Uninsured Seniors (Ages 65+) | <1% (most covered by Medicare) |

| Racial/Ethnic Disparities | Higher rates among Hispanic (20.7%) and Black (14.1%) populations compared to White (9.8%) |

| Income-Based Disparities | Higher uninsured rates among low-income households (below 200% FPL) |

| Employment Status | Higher uninsured rates among part-time or self-employed workers |

| Medicaid Expansion Status | Georgia has not expanded Medicaid (as of 2023), contributing to higher uninsured rates |

| Urban vs. Rural Disparities | Higher uninsured rates in rural areas compared to urban areas |

| Source | U.S. Census Bureau, American Community Survey (ACS) 2022 |

Explore related products

What You'll Learn

- Uninsured rate trends in Georgia over the past decade

- Factors contributing to lack of health insurance in Georgia

- Impact of income levels on uninsured populations in Georgia

- Role of Medicaid expansion in reducing uninsured rates in Georgia

- Geographic disparities in uninsured rates across Georgia counties

![]()

Uninsured rate trends in Georgia over the past decade

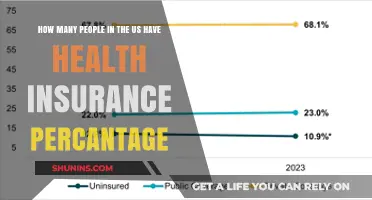

Over the past decade, Georgia's uninsured rate has seen significant fluctuations, reflecting broader national trends and state-specific policy decisions. In 2013, before the full implementation of the Affordable Care Act (ACA), approximately 19.4% of Georgians lacked health insurance. By 2016, this figure had dropped to 12.9%, a testament to the ACA’s expansion of coverage options. However, Georgia’s decision not to expand Medicaid under the ACA has since constrained further reductions, leaving the state with one of the highest uninsured rates in the nation. As of 2022, around 12.4% of Georgians remain uninsured, highlighting persistent gaps in access to healthcare.

Analyzing these trends reveals a stark contrast between federal initiatives and state-level resistance. While the ACA’s marketplace subsidies and Medicaid expansion have been effective in other states, Georgia’s refusal to expand Medicaid has left hundreds of thousands of low-income residents without coverage. This gap disproportionately affects working-age adults (18–64), who often earn too much to qualify for traditional Medicaid but too little to afford private insurance. For example, a single adult earning between $6,000 and $18,000 annually falls into this coverage gap, underscoring the need for targeted policy interventions.

A comparative perspective further illuminates Georgia’s challenges. Neighboring states like Kentucky and Arkansas, which expanded Medicaid, have uninsured rates below 7%. In contrast, Georgia’s rate remains nearly double, despite having a similar demographic profile. This disparity suggests that policy choices, rather than socioeconomic factors alone, drive the state’s high uninsured rate. Advocates argue that expanding Medicaid could reduce the uninsured rate by up to 50%, providing coverage to an estimated 400,000 Georgians.

Practical steps to address this issue include increasing awareness of ACA marketplace subsidies, which can significantly lower premiums for eligible individuals. For instance, a family of four earning up to $100,000 annually may qualify for subsidies, yet many remain unaware of this option. Additionally, community health centers and nonprofit organizations play a critical role in bridging gaps by offering low-cost or sliding-scale services. Policymakers could also explore state-specific solutions, such as Georgia’s recent proposal to implement a Medicaid waiver program, though its impact remains uncertain.

In conclusion, Georgia’s uninsured rate trends over the past decade highlight both progress and persistent challenges. While federal policies have reduced the uninsured population, state-level barriers continue to limit access. Addressing this issue requires a multifaceted approach, combining policy reforms, public education, and community-based initiatives. By learning from successful models in other states and tailoring solutions to Georgia’s unique needs, the state can make significant strides in ensuring healthcare coverage for all residents.

Prescribing HAART Medications: Insurance and Access

You may want to see also

Explore related products

![]()

Factors contributing to lack of health insurance in Georgia

As of recent data, approximately 12% of Georgia's population, or around 1.2 million people, lack health insurance. This figure places Georgia among the states with the highest uninsured rates in the U.S., highlighting a persistent challenge in healthcare access. Understanding the factors behind this issue is crucial for addressing it effectively.

One significant contributor is Georgia's decision not to expand Medicaid under the Affordable Care Act (ACA). Unlike many states, Georgia has maintained strict eligibility criteria for Medicaid, excluding low-income adults who do not have children or disabilities. This gap leaves hundreds of thousands of Georgians without affordable coverage options, as they earn too much to qualify for Medicaid but too little to afford private insurance. For context, a single adult without children must earn less than 36% of the federal poverty level (FPL) to qualify for Medicaid in Georgia, which equates to roughly $5,000 annually—an impossibly low threshold for survival.

Another factor is the high cost of private health insurance, particularly for individuals and families purchasing plans on the ACA marketplace. Despite federal subsidies, premiums and out-of-pocket costs remain prohibitive for many. For example, a 40-year-old in Atlanta might face monthly premiums exceeding $400 for a mid-tier plan, with deductibles often surpassing $4,000. Small businesses, which employ a significant portion of Georgia's workforce, frequently cannot afford to offer employer-sponsored insurance, leaving workers to navigate the individual market.

Geographic disparities also play a role, particularly in rural areas where healthcare infrastructure is limited. In counties like Clay or Talbot, residents may live hours away from the nearest hospital or specialist, reducing the perceived value of insurance. Additionally, rural Georgians often work in industries like agriculture or service, which are less likely to provide health benefits. This combination of limited access and lower wages creates a cycle where insurance feels unnecessary or unattainable.

Lastly, systemic barriers, such as lack of awareness about enrollment periods or confusion over eligibility, prevent some Georgians from securing coverage. The ACA's annual open enrollment period, typically from November to January, is often missed due to inadequate outreach or language barriers. For instance, Spanish-speaking residents, who make up over 10% of Georgia's population, may struggle to find resources in their native language. Similarly, undocumented immigrants, though ineligible for most insurance programs, may avoid seeking information due to fear of legal repercussions, leaving even U.S. citizen family members uninsured.

Addressing these factors requires a multi-faceted approach: expanding Medicaid, increasing subsidies for marketplace plans, investing in rural healthcare, and enhancing public awareness campaigns. Without targeted interventions, Georgia's uninsured rate will likely persist, perpetuating health disparities and economic strain.

Dropping Medical Insurance: Understanding Work Benefits and Alternatives

You may want to see also

Explore related products

![]()

Impact of income levels on uninsured populations in Georgia

In Georgia, the correlation between income levels and the uninsured rate is stark, with lower-income individuals disproportionately lacking health coverage. According to recent data, approximately 12% of Georgians are uninsured, and this figure climbs to nearly 20% for those living below the federal poverty level. This disparity highlights a critical issue: as income decreases, the likelihood of being uninsured increases dramatically. For families earning less than $25,000 annually, the financial burden of health insurance premiums, deductibles, and copays often becomes insurmountable, forcing difficult choices between healthcare and basic necessities like food and housing.

Consider the mechanics of this relationship. Georgia’s decision not to expand Medicaid under the Affordable Care Act (ACA) has left a coverage gap, where individuals earning too much to qualify for traditional Medicaid but too little to afford private insurance are left without options. For example, a single adult earning $12,000 annually falls into this gap, ineligible for Medicaid yet unable to allocate even $200 monthly for a marketplace plan. This structural exclusion disproportionately affects low-wage workers in industries like agriculture, hospitality, and retail, where employer-sponsored insurance is rare and wages are insufficient to bridge the gap.

To address this, policymakers and advocates must focus on targeted solutions. Expanding Medicaid eligibility to cover individuals up to 138% of the federal poverty level would immediately reduce uninsured rates among low-income Georgians. Additionally, subsidizing premiums for those in the coverage gap could make marketplace plans more accessible. For instance, a subsidy that caps premiums at 5% of income for individuals earning below $30,000 annually could provide relief. Pairing these measures with outreach campaigns in underserved communities, such as translating materials into Spanish and providing enrollment assistance at local clinics, could further increase uptake.

Comparatively, states that have expanded Medicaid, such as neighboring North Carolina, have seen uninsured rates drop by as much as 50% among low-income populations. Georgia could replicate this success by leveraging federal funding, which covers 90% of expansion costs. Critics argue that expansion strains state budgets, but evidence from other states shows long-term savings through reduced uncompensated care costs and improved public health outcomes. For Georgia, the choice is clear: inaction perpetuates a cycle of financial instability and poor health for low-income residents, while strategic policy changes could transform access and affordability.

Finally, the human cost of this issue cannot be overlooked. Uninsured individuals are more likely to delay or forgo necessary care, leading to untreated chronic conditions, preventable hospitalizations, and higher mortality rates. A 40-year-old uninsured Georgian with diabetes, for instance, may skip insulin or checkups due to cost, risking complications like kidney failure or amputations. By addressing the income-based disparities in insurance coverage, Georgia can not only improve health outcomes but also reduce the economic burden on its healthcare system, creating a healthier, more equitable state for all.

Why Insurance Companies Often Fail Their Customers: A Critical Look

You may want to see also

Explore related products

![]()

Role of Medicaid expansion in reducing uninsured rates in Georgia

Georgia's uninsured rate has long been a pressing issue, with approximately 12% of its population lacking health coverage as of recent data. This places Georgia among the states with the highest uninsured rates in the nation. One of the most debated solutions to this problem is Medicaid expansion, a policy that has proven effective in other states but remains contentious in Georgia. By examining the role of Medicaid expansion, we can understand its potential impact on reducing uninsured rates and improving public health outcomes in the state.

Analytically, Medicaid expansion under the Affordable Care Act (ACA) extends eligibility to adults earning up to 138% of the federal poverty level, a group often referred to as the "coverage gap." In Georgia, an estimated 300,000 to 400,000 individuals fall into this gap, earning too much to qualify for traditional Medicaid but too little to afford private insurance. States that have expanded Medicaid have seen significant reductions in uninsured rates, with some experiencing declines of up to 50%. For example, neighboring states like Kentucky and Arkansas, which expanded Medicaid, have uninsured rates below 10%, compared to Georgia’s higher figure. This data underscores the potential for Medicaid expansion to address Georgia’s coverage gap directly.

Instructively, implementing Medicaid expansion in Georgia would require legislative action to accept federal funding, which covers 90% of expansion costs. The process involves submitting a state plan amendment to the Centers for Medicare & Medicaid Services (CMS) and designing a program that aligns with federal guidelines while addressing state-specific needs. States have flexibility in their approach, such as incorporating work requirements or offering premium assistance for private plans. For Georgia, a tailored expansion could include initiatives like rural healthcare access improvements, given the state’s significant rural population, which faces unique health disparities.

Persuasively, the economic and health benefits of Medicaid expansion in Georgia cannot be overstated. Studies show that expansion states have experienced reduced uncompensated care costs for hospitals, increased job growth in the healthcare sector, and improved health outcomes for low-income adults. For instance, expanded Medicaid coverage has been linked to higher rates of cancer screenings, chronic disease management, and mental health treatment. In Georgia, where rural hospitals are closing at alarming rates, Medicaid expansion could provide a financial lifeline, ensuring access to care for thousands while stabilizing healthcare infrastructure.

Comparatively, Georgia’s current approach to healthcare coverage falls short when compared to states that have embraced Medicaid expansion. While Georgia has implemented limited initiatives, such as the Georgia Pathways program, which imposes work requirements on Medicaid recipients, these measures have not significantly reduced uninsured rates. In contrast, states like Louisiana and Virginia, which expanded Medicaid in recent years, have seen rapid declines in uninsured populations and improved overall health metrics. Georgia’s reluctance to expand Medicaid leaves it an outlier, missing out on billions in federal funding and the opportunity to address its coverage gap effectively.

Descriptively, the human impact of Medicaid expansion in Georgia would be profound. Imagine a single mother in Atlanta, working part-time at a minimum wage job, who currently cannot afford health insurance. Under expansion, she would gain access to preventive care, prescription medications, and mental health services, improving her quality of life and ability to care for her family. Similarly, a small business owner in rural south Georgia, unable to provide health benefits to employees, would see his workers gain coverage, reducing absenteeism and increasing productivity. These stories illustrate the transformative potential of Medicaid expansion for individuals and communities across Georgia.

In conclusion, Medicaid expansion stands as a proven, effective strategy for reducing uninsured rates in Georgia. By closing the coverage gap, stabilizing healthcare systems, and improving health outcomes, expansion offers a pathway to a healthier, more equitable state. While political and logistical challenges remain, the evidence from other states and the clear benefits for Georgians make a compelling case for action. The question is not whether Georgia can afford to expand Medicaid, but whether it can afford not to.

Understanding AM Health Insurance: Benefits, Coverage, and Cost-Saving Tips

You may want to see also

Explore related products

![]()

Geographic disparities in uninsured rates across Georgia counties

Georgia's uninsured rate varies dramatically across its 159 counties, revealing a patchwork of access to healthcare that defies simple statewide averages. While the state’s overall uninsured rate hovers around 12%, certain counties report rates exceeding 20%, while others dip below 5%. This geographic disparity is not random; it mirrors broader socioeconomic and demographic patterns, with rural counties consistently faring worse than their urban counterparts. For instance, Clayton County, part of the Atlanta metro area, enjoys an uninsured rate of approximately 8%, whereas rural counties like Clay and Talbot report rates above 18%. Such variations underscore the need to examine local factors driving these differences.

To understand these disparities, consider the role of economic opportunity and industry. Rural counties often lack the diversified economies found in urban centers, relying heavily on agriculture or declining manufacturing sectors. This limits access to employer-sponsored insurance, the primary coverage source for most Americans. In contrast, counties like Fulton and DeKalb, home to Atlanta’s thriving corporate and healthcare sectors, offer more job opportunities with benefits. Additionally, urban areas benefit from higher Medicaid enrollment rates, partly due to better access to enrollment assistance programs. Rural residents, despite often qualifying for Medicaid, face barriers like limited transportation and fewer outreach efforts, exacerbating their uninsured status.

Another critical factor is the political and policy landscape at the county level. Georgia’s decision not to expand Medicaid under the Affordable Care Act disproportionately affects rural counties, where lower incomes make residents more likely to fall into the "coverage gap"—earning too much for traditional Medicaid but too little for subsidized marketplace plans. For example, in counties like Randolph and Schley, where median incomes are well below the state average, the absence of expanded Medicaid leaves thousands without affordable options. Meanwhile, counties with larger populations of federal employees or retirees, such as Richmond (home to Augusta), tend to have lower uninsured rates due to access to federal health benefits.

Addressing these disparities requires targeted interventions tailored to each county’s unique challenges. In rural areas, mobile health clinics and telehealth initiatives could bridge the gap in physical access to care. Urban counties, while better off overall, still face pockets of high uninsured rates among low-income populations, necessitating localized outreach campaigns. Policymakers could also incentivize small businesses in rural counties to offer health benefits through tax credits or subsidies. Ultimately, reducing geographic disparities in uninsured rates demands a nuanced approach that acknowledges the distinct realities of Georgia’s diverse counties.

Medical Insurance: What Hospitals in SA TX Offer

You may want to see also

Frequently asked questions

As of the latest data, approximately 1.4 million people in Georgia are uninsured, representing about 13% of the state’s population.

Georgia’s uninsured rate is higher than the national average. While Georgia’s rate is around 13%, the U.S. average is approximately 9%.

Low-income adults, young adults (ages 18–34), and Hispanic individuals are among the groups most likely to be uninsured in Georgia.

The number of uninsured individuals in Georgia has fluctuated but remains persistently high due to factors like the state’s decision not to expand Medicaid under the Affordable Care Act.

Common reasons include high insurance costs, lack of employer-sponsored coverage, and ineligibility for Medicaid due to Georgia’s strict eligibility criteria.