Private mortgage insurance (PMI) is an additional cost that protects the lender in the event that the borrower defaults on their loan. It is usually required when homebuyers make a down payment of less than 20% of the home's value. The cost of PMI is calculated as a percentage of the mortgage loan amount, typically ranging from 0.5% to 1.86% annually. There are several ways to remove PMI from your monthly mortgage payments, including reaching 20% equity in your home, reducing your loan balance to below 80% of the purchase price, or reaching the midpoint of your loan's amortization schedule. In some cases, you may need to provide evidence that you have a good payment history and that the value of your property has not declined.

| Characteristics | Values |

|---|---|

| When can PMI be removed? | When the mortgage’s loan-to-value (LTV) ratio reaches 78% of the home’s purchase price or the month after the loan term's midpoint. |

| How to remove PMI faster? | By making extra payments toward the principal balance, refinancing, getting a reappraisal, or paying down the mortgage faster. |

| When can FHA MIP be removed? | After 11 years or when the loan-to-value (LTV) ratio reaches 78% (depending on the loan). |

| How to remove FHA MIP? | By refinancing to a conventional loan if it saves you money. |

| When can LPMI be removed? | By refinancing. |

| When can MIP be removed from a multi-unit property? | When the loan term is halfway through, or when 30% equity is reached. |

Explore related products

What You'll Learn

- Lender must cancel PMI when the loan reaches 78% of the home's purchase price

- You can request cancellation when the loan reaches 80% of the home's value

- You can request cancellation if the home's value increases

- Automatic cancellation after 11 years for FHA loans with a 10% down payment

- No automatic cancellation for multi-unit homes owned by Freddie Mac

![]()

Lender must cancel PMI when the loan reaches 78% of the home's purchase price

Private mortgage insurance (PMI) is an additional monthly cost that protects the lender in case the borrower defaults on their mortgage. It is usually required when homebuyers make down payments of less than 20% of the home's value.

The Homeowners Protection Act of 1998 (HPA) requires mortgage lenders or servicers to automatically cancel PMI when the loan-to-value (LTV) ratio reaches 78% of the home's purchase price. This means that the principal balance of the mortgage has dropped to 78% of the original value of the home. This is true even if the midpoint of the loan's amortization schedule has not been reached.

For example, if you have a $250,000 home loan, your PMI will typically range from $1,250 to $2,500 per year or between $104 and $208 per month. Once your loan balance drops to $195,000 (78% of $250,000), your lender is required to cancel your PMI.

It's important to note that you can also request an early cancellation of PMI. If you've owned the home for at least five years, you can ask for PMI cancellation when your loan balance is no more than 80% of the new valuation. If you've owned the home for at least two years, your remaining mortgage balance must be no greater than 75% of the new valuation. To make this request, you'll need to provide a written request or fill out a specific form provided by your lender. Additionally, you'll need to pay for a home appraisal to verify that the value of your property has not declined.

It's worth mentioning that if you have an investment property or multiunit home loan owned by Freddie Mac, there is no automatic cancellation of mortgage insurance. In this case, you'll need to show 35% equity to request a cancellation, regardless of whether it's based on the original value or home improvements. If it's based solely on increases in market value, you'll need to wait at least two years before requesting a cancellation.

Engine Overheating Emergencies: A Guide to Staying Safe and Smart

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![]()

You can request cancellation when the loan reaches 80% of the home's value

Private mortgage insurance (PMI) is an additional monthly cost that protects the lender in the event that you default on your mortgage. It is usually required if you bought a home with less than a 20% down payment.

You can request to cancel PMI when your loan balance reaches 80% of your home's value. This is known as reaching 20% equity in your home. To make this request, you will need to submit a written request to your mortgage servicer. You may also need to pay for a home appraisal to verify that the value of your property has not declined.

It is important to note that the rules for removing PMI may vary depending on the type of mortgage loan you have and the lender. For example, if you have a Federal Housing Administration (FHA) loan, removing mortgage insurance may be more complicated and may require refinancing. Additionally, if you have an investment property or multi-unit home loan owned by Freddie Mac, there is no automatic cancellation of mortgage insurance, and you will need to show 35% equity to request termination.

There are ways to get rid of PMI ahead of schedule, such as by refinancing, getting a reappraisal, or paying down your mortgage faster. However, if you are unable to get a lower interest rate by refinancing, it may not be worth it, as you could end up paying more for PMI on a conventional loan than you would on an FHA loan.

Is Your Mortgage Federally Insured? Find Out How

You may want to see also

Explore related products

![]()

You can request cancellation if the home's value increases

Private mortgage insurance (PMI) is a type of insurance that protects the lender if you default on your loan. It is usually required if you put less than 20% down on your home. However, there are ways to get rid of PMI once you have built up enough equity in your home.

If the value of your home has increased, you may be able to request PMI cancellation. To do this, you will need to pay for a home appraisal to verify the new market value and prove that your loan balance is no more than 80% of the new valuation. This is known as the loan-to-value (LTV) ratio, and it is calculated by dividing the remaining mortgage balance by the current value of the home. For example, if you purchased a $300,000 home and your mortgage balance is $240,000, your LTV ratio would be 80%.

It's important to note that the requirements for removing PMI may vary depending on the lender and the type of property. For example, if you have an investment property or a multi-unit home loan owned by Freddie Mac, there may be different equity requirements for PMI cancellation. Additionally, some lenders may accept a broker price opinion instead of a formal appraisal, which can be cheaper.

To initiate the PMI cancellation process, you will need to contact your lender or mortgage servicer. In some cases, a phone call may be sufficient to document the request and begin the process. However, some lenders may require a written request or a specific form to be filled out. It is recommended to start with a phone call to review the guidelines and requirements for PMI removal.

Keep in mind that, in addition to reaching the required equity threshold, you will also need to be current on your mortgage payments for PMI cancellation to be approved. Late payments in recent months may disqualify you from cancelling PMI. By staying up to date on your payments and monitoring your home's value, you can take advantage of the opportunity to remove PMI when eligible.

Critical Illness Insurance: Is MetLife's Plan Worth the Cost?

You may want to see also

Explore related products

![]()

Automatic cancellation after 11 years for FHA loans with a 10% down payment

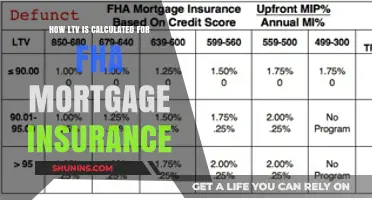

If you have an FHA loan, you'll need to pay for a Mortgage Insurance Premium (MIP). This is a type of mortgage insurance that is required for all FHA loans. While MIP has a similar function to Private Mortgage Insurance (PMI), it differs in that you must pay for it regardless of how much you put down as a down payment, and you'll often pay it for the life of the loan.

However, there is an exception to this rule: if you take out an FHA loan and put down at least 10% as a down payment, you'll only need to pay MIP for 11 years. After this, it will be automatically cancelled. This rule applies to loans taken out after June 3, 2013. If your loan was taken out before this date, you can still cancel MIP after 11 years, but only if your down payment was at least 10% and your loan amount is no more than 78% of your home's FHA-appraised value.

If you don't meet the criteria for automatic MIP cancellation, you'll need to consider refinancing your FHA loan. This can be done using several loan types, including a conventional loan, a USDA loan, or a VA loan. However, the latter two are reserved for specific borrower types. For most people, refinancing from an FHA loan into a conventional loan will be the best option.

To prepare for the automatic cancellation of your MIP after 11 years, it's a good idea to follow up with your loan servicer a few months before your loan's 11-year anniversary to ensure that the cancellation is on track. Your servicer is the company that manages your loan and accepts your mortgage payments, and they will be able to advise you on the next steps.

Farmers Insurance Open: Saturday's Final Round a Treat for Golf Fans

You may want to see also

Explore related products

![]()

No automatic cancellation for multi-unit homes owned by Freddie Mac

Private mortgage insurance (PMI) is a type of policy that you must purchase if you put less than 20% down payment on your home with a conventional mortgage. It protects your lender in case you default on your mortgage, and you typically pay premiums as part of your monthly mortgage payment. While federal law requires mortgage lenders to automatically cancel PMI when the balance of the mortgage drops to 78% of the home's purchase price, or halfway through the loan term, there are no automatic cancellations for multi-unit homes owned by Freddie Mac.

For multi-unit homes or investment properties, the requirements for removing PMI vary. If your multi-unit home loan is owned by Freddie Mac, there is no automatic cancellation of mortgage insurance. To terminate the insurance, you must show 35% equity, regardless of the reason for your request. If you are basing the request solely on increases in market value, you will need to wait at least two years.

It is important to note that PMI cancellation guidelines created by loan investors like Freddie Mac cannot be less favourable to the borrower than the standard guidelines. The standard guidelines state that you can request to cancel PMI ahead of the scheduled date if you have made additional payments that reduce the principal balance of your mortgage to 80% of the original value of your home. The "original value" generally refers to either the contract sales price or the appraised value of your home when you purchased it, whichever is lower.

To remove PMI, you will need to contact your servicer with a written request and they may have a specific form for you to fill out. You will need to build up at least 20% equity in your home and get a home valuation to ensure that the home value has not declined and still meets expectations.

Building Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

You need to pay at least 20% of the home's value upfront to avoid paying mortgage insurance.

Mortgage insurance costs between 0.5% and 1% of your total loan amount per year.

You can remove mortgage insurance by reaching 20% equity in your home or by paying your loan balance down to below 80% of the purchase price of your home.