Mortgage insurance is an insurance policy that protects the lender or property holder in the event that the borrower defaults on payments, passes away, or is otherwise unable to meet the contractual obligations of the mortgage. It is typically required when the borrower makes a down payment of less than 20% of the purchase price of the home. The cost and payment structure of mortgage insurance can vary depending on the type of loan and the borrower's credit score. It is important to distinguish mortgage insurance from homeowners insurance, which covers the home and protects the homebuyer in case the home becomes temporarily unlivable or if liability claims are made.

| Characteristics | Values |

|---|---|

| Who does mortgage insurance protect? | The lender or titleholder |

| Who needs mortgage insurance? | Those who borrow with a down payment of less than 20% |

| Who doesn't need mortgage insurance? | Those who borrow with a down payment of more than 20% |

| What does mortgage insurance cover? | Financial loss if the borrower defaults on payments or cannot meet mortgage obligations |

| What does mortgage insurance not cover? | The borrower, homeowners, or the home itself |

| Types of mortgage insurance | Private mortgage insurance (PMI), qualified mortgage insurance premium (MIP) insurance, mortgage title insurance, mortgage protection insurance (MPI), mortgage life insurance |

| How is mortgage insurance paid? | Monthly premium, upfront lump sum, or a combination of both |

| Can mortgage insurance be cancelled? | Yes, once the borrower has paid enough to reach more than 20% equity in their home |

| What is mortgage protection insurance (MPI)? | An optional policy that protects the lender in the event of the borrower's death |

| What is mortgage life insurance? | A policy that pays the lender directly in the event of the borrower's death |

Explore related products

$4.99 $14.99

What You'll Learn

![]()

Private mortgage insurance (PMI)

PMI is arranged by the lender and provided by private insurance companies. It insures the lender against loss caused by borrowers failing to make loan payments. If you fall behind on your mortgage payments, PMI does not protect you, and you can still lose your home through foreclosure. PMI can help you qualify for a loan that you might not otherwise be able to get. However, it can increase the cost of your loan.

The amount you pay for PMI depends on your loan and down payment size, whether it’s a fixed- or adjustable-rate mortgage, and your credit score. For those with a credit score of 620 to 639, PMI can be as high as 1.5% of the loan amount, according to the Urban Institute. By comparison, those with a credit score of 760 or greater might pay as low as 0.46%. You can pay PMI with a one-time upfront premium at closing, monthly premiums, or a combination of both.

You can request to cancel PMI when your mortgage balance reaches 80% of your home’s value. Federal law dictates that your mortgage lender must automatically end your PMI when your loan-to-value (LTV) ratio drops to 78%, or when you are one month past the midpoint of your loan term.

American Family vs. Farmers Insurance: A Comprehensive Comparison Guide

You may want to see also

Explore related products

![]()

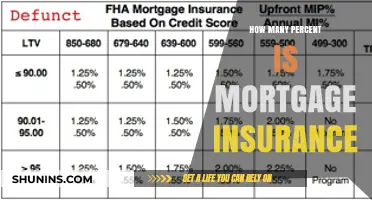

Qualified mortgage insurance premium (MIP) insurance

Mortgage insurance is an insurance policy that protects the lender or titleholder against financial loss if the borrower defaults on payments or cannot meet mortgage obligations. It lowers the risk to the lender of making a loan to the borrower, allowing the borrower to qualify for a loan they may not otherwise be able to get. However, it increases the cost of the loan for the borrower.

A Qualified Mortgage Insurance Premium (MIP) Insurance is a type of mortgage insurance that is required for homeowners who take out loans backed by the Federal Housing Administration (FHA). FHA-approved lenders provide lower down payment requirements and more flexible credit qualifying requirements compared to most conventional loans. Therefore, MIP protects the lender in the case of default by higher-risk borrowers.

MIP has two parts: an upfront premium and an annual premium. The upfront premium is often paid as part of the closing costs but can also be rolled into the loan cost and paid monthly if the borrower cannot pay it upfront. The annual premium is calculated yearly and then divided by 12 and included in the borrower's monthly mortgage payment.

MIP is typically required for the full loan term if the down payment for an FHA loan is less than 10% of the home's value. However, there are certain circumstances where the annual MIP can be removed, such as refinancing the FHA loan into a conventional mortgage.

The Catchy Rhythm of Insurance: Exploring the BPM of Farmers Insurance Jingle

You may want to see also

Explore related products

![]()

Mortgage title insurance

In the context of mortgage insurance, mortgage title insurance protects the lender or titleholder against financial loss if the borrower defaults on payments or cannot meet mortgage obligations. It is worth noting that the type of mortgage insurance you need can depend on various factors, including the type of mortgage and the size of your down payment.

Safety Valve Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Mortgage protection insurance (MPI)

MPI is available through insurance companies and mortgage lenders. The cost of MPI depends on various factors, including the number of years left on the mortgage, the mortgage balance, the policyholder's age, and the property location. MPI applicants generally don't need to undergo a health exam, making it a good option for those who may not qualify for traditional life insurance due to pre-existing health conditions. However, MPI tends to be more expensive than traditional life insurance because of its more flexible underwriting criteria.

It's important to note that MPI is not the same as private mortgage insurance (PMI) or mortgage insurance premium (MIP). PMI is required when a borrower makes a down payment of less than 20% on a conventional loan, while MIP is typically required for Federal Housing Administration (FHA) loan borrowers. Unlike MPI, PMI and MIP protect the lender, not the borrower, in the event of default.

When considering MPI, it's essential to review the terms and conditions carefully, as the specifics of coverage can vary depending on the policy and provider. MPI may offer peace of mind and financial security for homeowners, but it has drawbacks, including decreasing coverage over time and limited flexibility in how the payout can be used.

Mortgage Insurance: Principal Payment or Extra Cost?

You may want to see also

Explore related products

$8

$9.97 $19.99

![]()

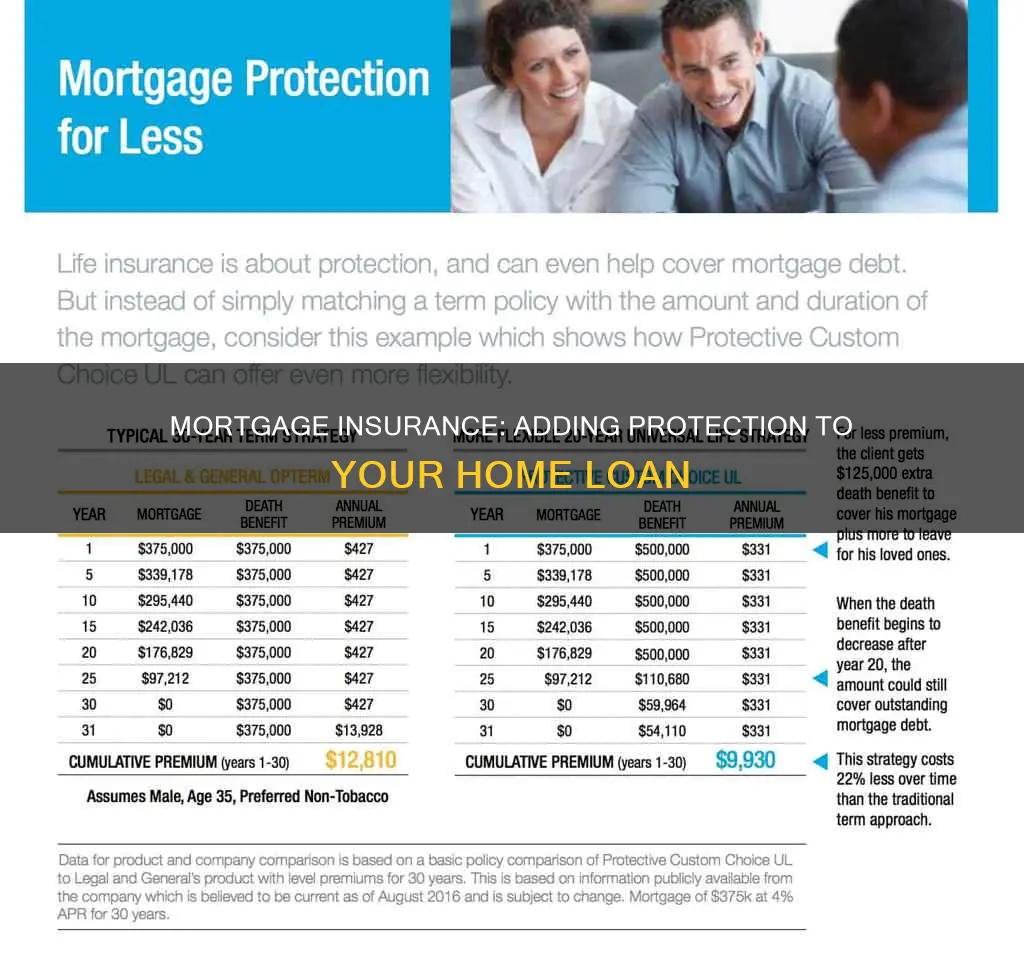

Mortgage life insurance

However, mortgage life insurance also has some drawbacks. It tends to be more expensive than term life insurance, and the lack of flexibility means that beneficiaries cannot use the payout for other expenses or debts. The policy also ends if you pay off your mortgage before your passing, and there is no cash value growth component, limiting its use as a wealth-building tool.

Overall, while mortgage life insurance can provide peace of mind and protect your loved ones from mortgage debt, it is important to carefully consider its limitations and compare it with other types of life insurance to determine the best option for your specific needs.

Banfield Pet Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage insurance, also known as private mortgage insurance or PMI, is insurance that some lenders may require to protect their interests should the borrower default on their loan. It lowers the risk to the lender of making a loan to the borrower, so the borrower can qualify for a loan they might not otherwise be able to get.

There are typically two ways to pay for mortgage insurance. You can either pay a lump sum upfront or over time with monthly payments. The monthly cost of your PMI premium can also be rolled in with your monthly mortgage payment.

Not every homeowner needs mortgage insurance, but it may be required when you take out a mortgage loan and your down payment is less than 20% of the purchase amount. The requirement to have mortgage insurance varies by lender and loan product.