Auto insurance rates are determined by a variety of factors, including age, gender, location, driving history, and vehicle type. For a 41-year-old driver, the cost of auto insurance will depend on these factors and the specific insurance provider. On average, a 40-year-old driver can expect to pay around $2,542 for full coverage and $740 for minimum coverage annually, according to Bankrate. The cost of auto insurance tends to decrease as drivers get older, with teens and young adults paying the highest premiums due to their lack of driving experience and higher risk of accidents. Additionally, factors such as gender, driving record, and credit score can also impact the cost of auto insurance. It is recommended to shop around and compare quotes from multiple insurance providers to find the best rate.

| Characteristics | Values |

|---|---|

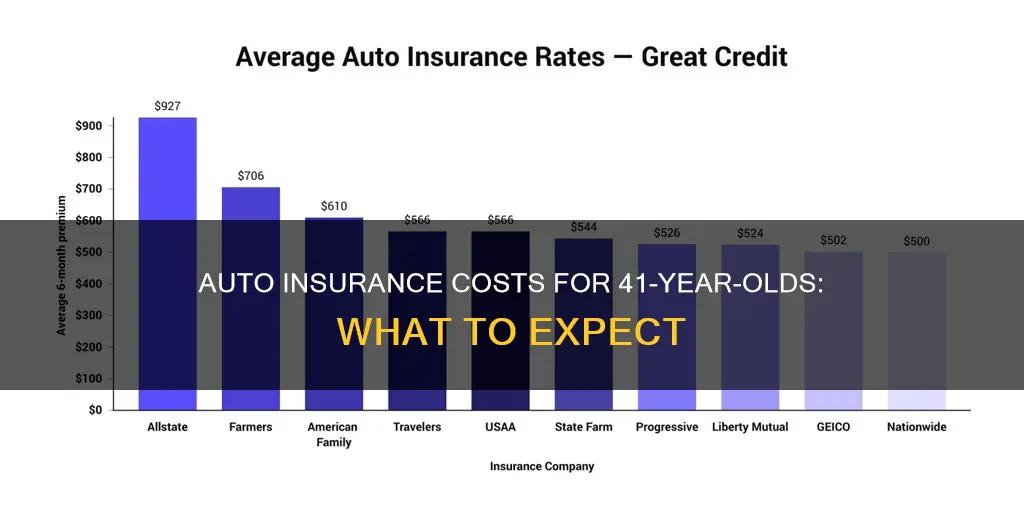

| Average annual cost of car insurance for a 41-year-old | $1,580 |

| Average monthly cost of car insurance for a 41-year-old | $132 |

| Average annual cost of car insurance for a 40-year-old | $2,542 for full coverage; $740 for minimum coverage |

| Average monthly cost of car insurance for a 40-year-old | $212 for full coverage; $62 for minimum coverage |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Gender as a rating factor

The use of gender as a rating factor in auto insurance is a controversial topic. While some states have banned the practice, it is still allowed in most states. Insurance companies that use gender as a rating factor argue that it is a fair practice based on actuarial research, while consumer advocates argue that it is discriminatory.

In states that allow gender to be used as a rating factor, males tend to pay more for auto insurance than females, especially during their teen and young adult years. This is because males are considered to be higher-risk drivers due to a higher likelihood of accidents, speeding, and DUI convictions. The price difference between males and females decreases as they get older, and by the age of 40, males may even pay slightly less than females. However, the difference is not significant compared to other factors such as driving record and credit score.

Some insurers have discontinued the use of gender as a rating factor, and it is expected that more states and insurers will move towards prohibiting the use of gender in setting car insurance rates as gender rights and equality issues gain more attention.

It is worth noting that the impact of gender on car insurance rates is not consistent across all states and insurance companies. Some states and insurers charge men and women equally, while others may even charge women higher premiums. Additionally, there is a lack of clarity on how car insurance rates are determined for transgender and non-binary individuals.

When it comes to auto insurance for a 41-year-old, gender may play a role in the premium, but it is just one of many factors. Other factors that can impact the cost of auto insurance include driving record, credit score, location, vehicle type, and marital status. It is always a good idea to shop around and compare quotes from different insurers to find the best rate.

Unraveling the Medical-Insurance Knot: Navigating Auto Insurance Claims in the Medical Office

You may want to see also

Explore related products

![]()

Age and insurance rates

Age is one of the most significant factors in determining auto insurance rates, with younger and older drivers generally facing higher premiums due to their increased likelihood of accidents. Auto insurance rates are highest for teens and seniors, who are considered high-risk, and rates steadily decrease as drivers get older, with middle-aged drivers being the cheapest to insure.

Teens are considered the riskiest drivers due to their lack of experience, with 16-year-olds paying an average of $3,192 per year for minimum coverage and $3,343 per year for minimum coverage. The cost of auto insurance for young adults is also high, with 20-year-olds paying an average of $3,092 per year for a full coverage policy. This is because insurance companies consider young drivers to be high-risk, as they are more likely to be involved in accidents and file expensive claims.

As drivers enter their 20s, their auto insurance rates start to decrease, with 30-year-olds paying an average of $136.75 per month and 40-year-olds paying an average of $126.69 per month for continuous coverage. By the time drivers reach their 50s, their auto insurance rates are significantly lower, with the average cost of car insurance for a 50-year-old being $1,209 per year for full coverage.

It is important to note that auto insurance rates are not only based on age but also on other factors such as gender, location, driving record, credit score, vehicle type, and coverage level. Additionally, auto insurance rates vary by state, with Wyoming having the cheapest full coverage rates and Florida having the most expensive.

Auto Insurance and Rental Cars: Understanding the Damage Waiver

You may want to see also

Explore related products

![]()

Average insurance rates by state

The average cost of car insurance varies from state to state and depends on several factors, including age, gender, driving record, credit score, and location. Here is a breakdown of the average insurance rates by state in the United States:

States with the Highest Average Insurance Rates

The states with the highest average insurance rates for full coverage are:

- New York: $8,232 per year

- Louisiana: $4,357 per year

- Michigan: $4,067 per year

- Pennsylvania: $3,909 per year

- Nevada: $3,870 per year

The states with the highest average insurance rates for minimum liability coverage are:

- New York: $2,221 per year

- Nevada: $1,665 per year

- Florida: $1,605 per year

- Louisiana: $1,497 per year

- New Jersey: $1,408 per year

States with the Lowest Average Insurance Rates

The states with the lowest average insurance rates for full coverage are:

- Maine: $1,460 per year

- Vermont: $1,539 per year

- Hawaii: $1,581 per year

- Idaho: $1,588 per year

- Ohio: $1,660 per year

The states with the lowest average insurance rates for minimum liability coverage are:

- Wyoming: $303 per year

- Vermont: $366 per year

- South Dakota: $443 per year

- Hawaii: $455 per year

- North Dakota: $460 per year

Other Factors Affecting Insurance Rates

In addition to location, several other factors can influence insurance rates. These include:

- Driving record: A history of accidents, speeding tickets, or other violations can increase rates.

- Deductible: Choosing a higher deductible can lower insurance premiums.

- Credit history: In most states, a higher credit score can lead to lower insurance rates.

- Age: Younger and older drivers often pay higher rates due to increased risk.

- Marital status: In some states, married drivers may pay lower insurance premiums.

- Population density: More populated areas may have higher insurance rates due to increased accident risks.

- State insurance minimums: The required coverage amounts in each state can impact average rates.

- Gender: In most states, male drivers pay higher rates than female drivers.

Auto Insurance and Garage Repairs: What's Covered?

You may want to see also

Explore related products

![]()

Insurance rates by vehicle type

The make and model of your vehicle is a major factor in determining your insurance rates. Insurers use this information to determine your car's worth, safety features, and how expensive it may be to repair. For example, an expensive luxury car model costs more to repair than a standard model, resulting in higher premiums.

- Vehicle MSRP: Pricier cars typically cost more to repair due to custom, foreign, or premium parts, which generally result in higher insurance premiums. You might also need higher coverage maximums to cover claims, which means you'll pay more for coverage.

- Safety ratings: Safer cars are less likely to be involved in accidents and cost less to repair, resulting in fewer claims and more savings for you.

- Likelihood of theft: Some cars are frequently targeted by thieves, which drives up insurance costs.

- Sportiness: Sportier cars tend to be associated with faster driving and riskier behavior, increasing the likelihood of collisions and claims.

- Body type: Convertibles, sports cars, and SUVs are typically more expensive to insure due to higher theft rates and the increased risk of collisions.

When comparing insurance rates by vehicle type, it's important to consider the specific make, model, trim, and model year of the car. Even within the same brand, different models can have varying insurance rates. For example, the cheapest car model to insure might be different from the most expensive one. Additionally, the age of the car can also impact the premium, with older cars potentially attaining greater value as classics.

Getting Your Auto Insurance Payout: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Insurance rates by gender

The cost of auto insurance varies depending on several factors, including age, gender, location, driving history, and credit score. While age is a significant factor, with younger drivers typically paying higher premiums than older drivers, gender also plays a role in determining insurance rates. Here is a detailed overview of insurance rates by gender:

In most states, gender is a factor that auto insurance companies consider when determining insurance rates. Males typically pay more for auto insurance during their teenage years and early adulthood, with rates gradually evening out as they get older. The gender gap in insurance rates is more pronounced at younger ages; at 20 years old, men pay approximately $581 more per year than women, while at 30 and 35 years old, the difference decreases to $23 and $13, respectively. On average, male drivers pay about 6% more for auto insurance than female drivers of the same age, which equates to a difference of roughly $245 annually or $16 per month.

However, it's important to note that this gap varies by state and insurance company. Some states, including California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania, have banned the use of gender as a factor in setting insurance rates. In these states, insurance companies are required to offer unisex or blended rates, eliminating any gender-based price differences.

The reason for the gender disparity in insurance rates lies in statistical data. Males, particularly young and teenage males, are considered higher-risk drivers due to a higher likelihood of accidents, speeding, and DUI convictions. According to the National Highway Traffic Safety Administration, male drivers involved in fatal accidents are more likely to have been speeding than female drivers. Additionally, men are less likely to wear seatbelts and are more likely to drive vehicles with higher insurance rates. As a result, insurance companies view them as a greater insurance risk and charge them higher premiums.

The gender gap in insurance rates begins to narrow as drivers age and gain more experience. By the time men and women reach their 30s, their insurance rates become more comparable, with only minor differences. Insurance companies still consider gender a risk factor, but other factors, such as driving record and credit score, become more significant in determining insurance rates.

It's worth noting that insurance rates for both genders can vary significantly depending on the insurance company and the specific details of an individual's policy. Shopping around and comparing rates from multiple companies can help drivers find the most affordable coverage for their needs. Additionally, taking advantage of discounts, such as those for good driving records or low mileage, can further reduce insurance costs.

Understanding the Ins and Outs of Auto Insurance Supplements

You may want to see also

Frequently asked questions

Auto insurance rates are highest for teens and seniors because they are considered high-risk due to an increased likelihood of accidents and expensive claims. Rates generally decrease as drivers get older and gain more experience, with middle-aged drivers typically paying the least for car insurance.

The cost of auto insurance for a 41-year-old can vary depending on factors such as gender, location, driving record, credit score, vehicle type, and coverage level. Age is one of the biggest factors influencing insurance rates, but it's important to note that other factors like driving record and vehicle type can also have a significant impact.

There are several ways for 41-year-olds to save on auto insurance. They can compare rates from multiple providers, choose a carrier that offers accident forgiveness, increase their deductibles (if they can afford to pay more out-of-pocket), and look for applicable discounts, such as those for safe driving, alumni groups, or bundling home and auto insurance.