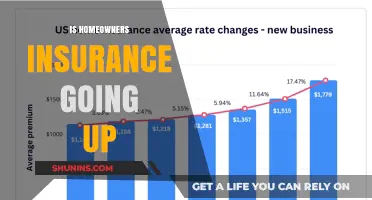

Homeowners insurance is an important consideration for anyone looking to buy a house. The cost of insurance for a $600,000 house will depend on a variety of factors, including the location, age, and size of the property, as well as the coverage amount, deductible, and the homeowner's credit score. On average, homeowners can expect to pay around $4,677 per year for insurance on a $600,000 house, but rates can vary significantly depending on the specific circumstances.

| Characteristics | Values |

|---|---|

| Average national cost of homeowners insurance for a $600,000 house | $4,677 a year |

| Average cost of home insurance with $600,000 in dwelling coverage and $300,000 in liability with a $1,000 deductible (excellent credit) | $3,986 |

| Average cost of home insurance with $600,000 in dwelling coverage and $300,000 in liability with a $1,000 deductible (poor credit) | $14,637 |

| Average cost of home insurance with $350,000 in dwelling coverage, $175,000 in personal property coverage and $100,000 in liability coverage | $1,678 per year |

| Average cost of homeowners insurance in the U.S. for $300,000 worth of dwelling coverage | $2,110 a year |

| Average cost of homeowners insurance in the U.S. for $300,000 worth of dwelling coverage | $2,466 a year |

| Average cost of homeowners insurance in Connecticut for $600,000 of dwelling coverage | $3,765 |

| Average cost of homeowners insurance in Kentucky for $600,000 of dwelling coverage | $6,142 |

Explore related products

$14.99 $14.99

What You'll Learn

![]()

Average national cost

The average national cost of homeowners insurance for a $600,000 house is $4,677 a year. However, this figure can vary depending on several factors. Firstly, the cost of home insurance depends on your ZIP code or location. For example, the average cost of $600,000 of dwelling coverage in Connecticut is $3,765, while in Kentucky, the same amount of coverage costs $6,142. The state you live in is, therefore, one of the biggest factors in home insurance rates.

Your credit score also plays a significant role in determining your insurance costs. Poor credit is associated with a higher likelihood of filing a claim, so you can expect to pay more for homeowners insurance if you have a poor credit rating. For instance, a person with excellent credit can expect to pay an average of $3,986 for home insurance with $600,000 in dwelling coverage and $300,000 in liability with a $1,000 deductible. On the other hand, poor credit can drive this average up to $14,637.

Other factors that can influence the cost of homeowners insurance include the deductible and liability limits you choose, the age and size of your home, the cost of building materials, and the threat of natural disasters in your area. It is also worth noting that home insurance is based on the replacement cost of your home, not its market value. Experts recommend purchasing enough coverage to rebuild your home from scratch at today's prices.

Progressive Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Cost determined by location

The location of your home is one of the greatest factors influencing the cost of homeowners insurance. The average national cost of homeowners insurance for a $600,000 house is $4,677 a year, but pricing varies from state to state. For example, in Connecticut, the average cost for $600,000 of dwelling coverage is $3,765, while in Kentucky, the same amount of coverage costs $6,142. Oklahoma, Texas, and Nebraska are the most expensive states for home insurance, while Hawaii, Vermont, and Delaware are the least expensive.

Your ZIP code plays a significant role in insurance companies' calculation of your risk profile, taking into account weather and natural disaster trends in the area, as well as claims history. Homes located in areas prone to extreme weather, flooding, wildfires, or crime will be more expensive to insure than homes in less risky areas. For instance, insurance rates may be higher if you live in an area vulnerable to wildfires, tornadoes, or hurricanes. Similarly, if your home is situated closer to a fire station, your premiums may be lower, whereas residing in a neighbourhood with higher crime rates could increase your premiums.

The cost of rebuilding your house is another critical factor in determining insurance rates. Home insurance is based on the replacement cost of your home, not its market value. Experts recommend obtaining enough coverage to rebuild your home from scratch at current prices. A home that cost $600,000 to construct may now cost $700,000 due to inflation, and this should be reflected in your insurance coverage.

Additionally, the age of your home can impact insurance rates. As a home gets older, materials degrade, and safety standards may become outdated, particularly concerning plumbing and electrical systems. This increases the risk of significant damage occurring during a covered event, leading to higher repair and rebuilding costs.

Accident Insurance: Dave Ramsey's Take on Coverage

You may want to see also

Explore related products

![]()

Credit score impact

The cost of home insurance for a $600,000 house depends on several factors, including location, coverage amounts, deductible, and credit score. The national average for homeowners insurance on a house with $600,000 in dwelling coverage is $4,677 per year, but this can vary significantly depending on your credit score.

In most states, insurers use credit-based insurance scores to help determine home insurance rates and whether to offer coverage. Poor credit is often associated with a higher likelihood of filing a claim, so individuals with poor credit may pay significantly more for homeowners insurance. For example, someone with a poor credit rating can pay up to 50% to 90% more than someone with an excellent credit rating. Additionally, in some states, insurers are not allowed to use credit history as a rating factor, and your credit score may not be the sole reason for an insurance company's decision.

While the impact of credit scores on insurance rates varies by company, individuals with poor credit may find it more challenging to obtain affordable home insurance. Requesting quotes and shopping around for insurance will not negatively impact your credit score, as insurance companies typically use soft pulls rather than hard inquiries when calculating credit-based insurance scores.

Improving your credit score can help reduce your homeowners insurance costs in the long term. Paying bills on time and using less available credit can positively impact your credit score and potentially lead to lower insurance premiums.

The Fine Print of Farmers Insurance: Understanding the Driving Agreement

You may want to see also

Explore related products

![]()

Coverage types

The cost of home insurance for a $600,000 house depends on several factors, including the location, coverage amounts, deductible, and credit score. The national average for homeowners insurance on a house with $600,000 in dwelling coverage is $4,677 per year, but prices vary across states.

Now, let's dive into the various coverage types available for homeowners insurance:

Home insurance coverage can be categorized into two main groups: personal property and personal liability. Here are some common coverage types:

Comprehensive Coverage:

This type of policy covers the building and its contents against all risks, except those specifically excluded. Optional coverages that can be purchased separately include flood, earthquake, or sewer backup coverage. Comprehensive coverage is ideal for those seeking extensive protection for their homes and belongings.

Basic or Named Perils Coverage:

This type of policy covers only the perils or risks that are specifically stated or listed in the policy. It does not include protection against unlisted events or risks. Named perils coverage is more limited in scope compared to comprehensive coverage.

Broad Coverage:

Broad coverage combines aspects of comprehensive and basic coverage. It provides comprehensive protection for high-value items, such as the building structure, while also offering named perils coverage for the contents within. This type of policy is suitable for those who want a blend of comprehensive and basic coverage.

No Frills Coverage:

This type of coverage is offered by some insurers for properties that do not meet standard insurance requirements. It may be an option for homes that are older, in unique circumstances, or do not qualify for traditional insurance policies.

Personal Liability Coverage:

Personal liability coverage protects you in the event someone is injured on your property or if your actions cause injury or damage to someone else's property. It covers the legal and financial consequences of such incidents, providing peace of mind.

Additional Living Expenses Coverage:

This type of coverage provides funds for temporary housing or living expenses if you need to relocate while your house is being repaired due to a covered loss. It ensures that you can maintain your standard of living even when your home is uninhabitable.

HO Policy Types:

There are several types of HO (Homeowners) policies available, offering different levels of coverage. HO-1 is the most basic, covering only the structure of the home and attached features. HO-2 offers broader coverage, including protection for your personal belongings. HO-3 is the most common type, providing coverage for the home, personal property, liability, and additional living expenses. HO-4 is for renters, while HO-5 offers the most comprehensive coverage for high-value properties, including coverage for possessions and access to additional add-ons.

It is important to carefully review the coverage types and choose the ones that best suit your needs as a homeowner. Understanding the specifics of each coverage type will help you make an informed decision when purchasing homeowners insurance for your $600,000 house.

Lift House Loan: Remove Insurance

You may want to see also

Explore related products

![]()

Cost-saving measures

The national average for homeowners insurance on a $600,000 house is $4,677 per year, but this can vary depending on several factors, such as location, coverage amount, deductible, and credit score. Here are some cost-saving measures to consider when looking to reduce the cost of homeowners insurance:

Shop Around for the Best Policy

Compare rates from multiple insurance companies to find the best deal. Check with friends, consult consumer guides, insurance agents, companies, and online insurance quote services to get an idea of price ranges and find the lowest prices.

Choose a Higher Deductible

The deductible is the amount you pay toward a loss before your insurance company starts to pay a claim. By choosing a higher deductible, you can significantly reduce your premiums. For example, increasing your deductible from $1,000 to $2,500 can save you about 12% annually. Just ensure you have enough savings to cover the higher deductible if needed.

Bundle Your Policies

Consider purchasing multiple policies from the same company. Many insurance providers offer discounts if you bundle your homeowners insurance with another type of insurance, such as auto or liability coverage. However, always compare the combined cost with the cost of purchasing separate policies from different companies to ensure you're getting a better deal.

Improve Your Credit Score

In most states, insurance companies consider your credit score when determining your insurance rates. A good credit score can help you secure lower premiums. Regularly check your credit record and promptly correct any errors to maintain a healthy score.

Install Safety and Security Devices

Insurance companies may offer discounts if you have safety and security features in your home, such as monitored burglary or smoke alarm systems, dead-bolt locks, or storm shutters. These features not only make your home more secure but can also help reduce your insurance costs.

By implementing these cost-saving measures, you can help mitigate the financial burden of homeowners insurance while ensuring you have the necessary coverage to protect your $600,000 house.

Home Insurance: What's Covered for Ductwork Damage?

You may want to see also

Frequently asked questions

The average cost of homeowners insurance in the US is $4,677 per year, but this figure can vary depending on several factors.

The cost of homeowners insurance depends on your ZIP code, coverage amounts, deductible, credit score, and policy structure. The location of your home, including the likelihood of natural disasters, the local crime rate, and the cost of living in the area, can also impact the price.

Poor credit is associated with a higher likelihood of filing a claim, so you may pay more for homeowners insurance if your credit score is poor. For example, a person with poor credit can pay up to 50% to 90% more than someone with excellent credit.

According to NerdWallet, the cheapest widely available home insurance company is Travelers, with an average annual rate of $2,055. Military insurer USAA offers even cheaper policies, with an average annual rate of $1,790.

Homeowners insurance typically includes liability coverage, which covers injuries and property damage you accidentally cause to others. It also covers your legal expenses if you are sued over such an incident. You can also add additional coverage, such as flood insurance, earthquake insurance, or windstorm insurance.