Homeowners' insurance rates are rising across the United States. There are several factors contributing to this increase, including severe weather events, rising inflation, supply chain issues, and increased building costs. The frequency and intensity of weather-related events, such as hurricanes, wildfires, and floods, have led to costly insurance claims and repairs, with natural disaster losses increasing tenfold from the 1980s to the 2020s. Inflation has also impacted the cost of homebuilding and repairs, with material goods for new residential construction rising by 14.3% between October 2021 and October 2022. In addition, legal system abuse, credit scores, and the availability of insurers in certain states are also contributing to rising insurance rates. These factors are causing concern among homeowners, with nearly 30% of American homeowners nervous about the increasing costs.

| Characteristics | Values |

|---|---|

| Average increase in homeowner's insurance rates | 23% increase from January 2023 |

| States with the most expensive insurance rates | Florida, Louisiana, Oklahoma, Kentucky, and Nebraska |

| Factors contributing to rising rates | Severe weather events, rising cost of building materials, supply chain issues, labor shortages, and unfilled jobs |

| States with projected premium increases | California (21%), with smaller carriers and "non-admitted" firms offering more affordable options |

| Average cost of home insurance in select states | Oklahoma ($6,133), Nebraska ($5,912), and Kansas ($5,412) |

| Ways to lower insurance premiums | Increase deductible, maintain and upkeep home, and avoid filing minor claims |

| Marital status impact | Married couples may receive lower premiums due to fewer claims, but individual rating factors and marital status changes can affect rates |

| Historical rate changes | Rates increased cumulatively by 40.4% across the U.S. from 2019 to 2024, with the biggest jump in 2021 (3.0%) |

Explore related products

What You'll Learn

![]()

Home insurance rates rose by 23% from January 2023

Home insurance rates have been increasing for a number of reasons, and this trend continued into 2023. By January 2023, home insurance rates had risen by 23% since the previous year. This sharp increase is a cause for concern for many homeowners, especially those already struggling with the financial strain of higher living costs.

There are several factors contributing to this rise in home insurance rates. One of the key reasons is the increase in the frequency and intensity of severe weather events, such as hurricanes, floods, droughts, wildfires, and windstorms. These events have resulted in costly insurance claims, with the United States sustaining 15 weather events with losses exceeding $1 billion each as of October 2022. As a result, insurers have been adjusting rates upwards to compensate for these losses and prepare for future climate disasters.

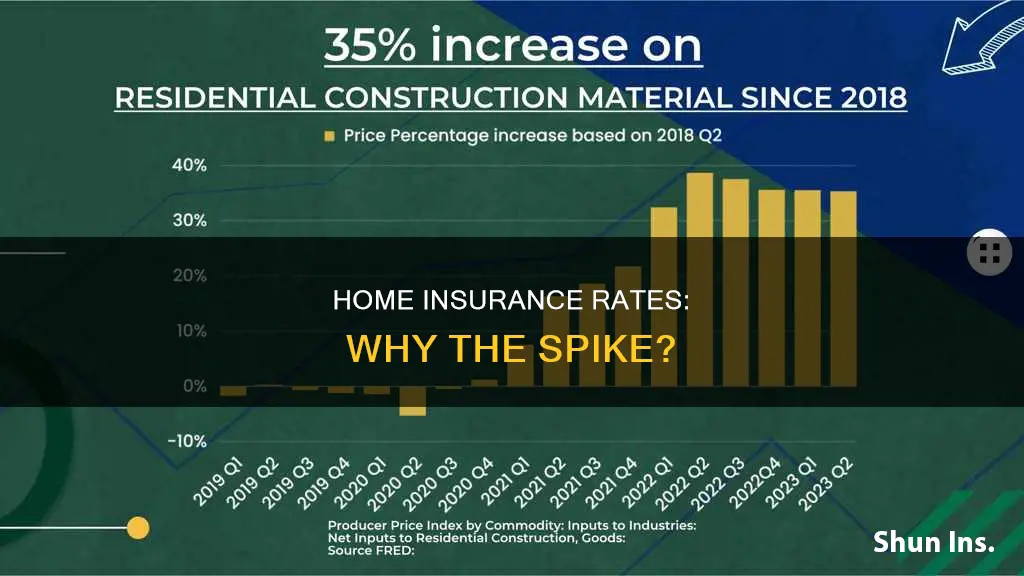

In addition to severe weather, the rising cost of building materials and labour is also driving up home insurance rates. The construction industry is facing challenges such as supply chain issues and skilled labour shortages, which have led to increased costs for repairs and rebuilding homes. Inflation has also played a significant role in the rising costs of homebuilding and repairs, with the cost of materials, parts, and labour rising significantly.

Another factor influencing home insurance rates is the location of the property. States with a higher risk of severe weather events or natural disasters, such as California, Florida, and Louisiana, tend to have higher insurance premiums. Additionally, the likelihood of a homeowner filing a claim also impacts rates, with insurers increasing premiums after claims related to theft, water damage, and liability due to the higher risk of repeated claims.

The increase in home insurance rates has led many homeowners to seek alternative options. Some have chosen to shop around for better rates, while others have considered bundling their insurance policies or increasing their deductibles to lower their premiums. As affordability becomes an issue in many parts of the country, it is essential for homeowners to explore different options and strategies to manage their insurance costs effectively.

Mortgage Insurance: Does the US Government Provide Coverage?

You may want to see also

Explore related products

$20.18 $24.99

![]()

Severe weather events and rising repair costs

The impact of severe weather events on insurance rates is particularly evident in certain regions. For example, consumers living in areas with a higher risk of climate-related perils, such as coastal areas or wildfire-prone states, face significantly higher insurance premiums. In some cases, insurance companies have even opted not to renew policies in these high-risk areas, leaving homeowners struggling to find alternative coverage.

Rising repair costs are another critical factor in the increasing cost of homeowners' insurance. The cost of building materials has increased due to supply chain issues, limited supplies, and inflation. Additionally, the construction industry faces a skilled labor shortage, resulting in higher wages and added expenses. These increased repair costs are driving up the cost of insurance claims, which is then passed on to homeowners through higher insurance premiums.

The combination of severe weather events and rising repair costs is creating a challenging situation for both homeowners and insurance providers. Homeowners are facing higher insurance premiums and may struggle to find affordable coverage, especially in high-risk areas. Insurance companies, on the other hand, are facing increasing losses and are adjusting their rates and coverage options to mitigate their risks.

As the frequency and intensity of severe weather events continue to rise due to climate change, it is likely that homeowners' insurance costs will continue to increase. This trend has significant implications for homeowners' financial planning, housing markets, and local economies. It also highlights the need for proactive measures to mitigate the impacts of climate change and severe weather events.

Farmers Insurance Exodus: Understanding the Florida Departure

You may want to see also

Explore related products

![]()

The skilled labor shortage and supply chain issues

The rise in homeowners insurance costs has been influenced by a combination of factors, including increasing natural catastrophe losses, inflation, and supply chain issues. One significant factor contributing to the increase in insurance rates is the skilled labor shortage. The construction industry has faced challenges due to a shortage of skilled workers, resulting in added expenses related to wages, supply chain problems, and other construction issues. This talent gap has become a critical issue, with Congress proposing the Creating Opportunities for New Skills Training at Rural and Underserved Colleges and Trade Schools (CONSTRUCTS) Act to address it.

The skilled labor shortage in the construction industry has been a long-standing issue, with a reported shortage of skilled construction workers in the US over the last five to ten years. This shortage has resulted in increased costs for insurance providers, as they have to pay higher wages to attract and retain workers. Additionally, the aging workforce in the insurance industry has contributed to the talent gap, with many employees nearing retirement. The US Bureau of Labor Statistics projects a significant decline in the insurance sector's workforce, anticipating a loss of around 400,000 workers through attrition by 2026.

The skilled labor shortage has been further exacerbated by the increasing demand for specific skill sets, such as data analytics, cybersecurity, and digital marketing. The adoption of new technologies and the need for specialized knowledge in insurance laws, compliance frameworks, and risk management practices have created a skills gap that the industry is struggling to fill. This shortage of skilled workers has not only impacted the construction industry but also the insurance sector, affecting their ability to adapt to the digital age and make informed business decisions.

The rise in homeowners insurance costs is also influenced by supply chain issues. The construction industry has faced challenges due to limited supplies and inflated prices for building materials. Lumber prices, in particular, have contributed significantly to the increase in insurance rates, as it is an important element in rebuilding homes after natural disasters. The supply chain bottleneck has made refrigerators and stoves more expensive and scarce, further adding to the challenges faced by the construction industry.

To address the skilled labor shortage and supply chain issues, insurance providers and construction companies need to adapt to market conditions and find innovative solutions. While some factors contributing to the rise in homeowners insurance costs may be beyond their control, such as natural disasters, companies can focus on effective succession planning, adopting new technologies, and exploring alternative sources for building materials to mitigate the impact of these issues.

Reporting Hurricane Damage: Insurance Payment Procedures

You may want to see also

Explore related products

![]()

Wildfires and natural disasters

Climate change has increased the frequency, severity, and geographic reach of natural disasters such as hurricanes and wildfires, making them more unpredictable and expensive. As a result, insurance companies are facing challenges in covering the costs of these disasters, which is causing an increase in insurance premiums for homeowners.

Wildfires have caused significant economic damage and loss of life, with California experiencing particularly devastating effects. Since 2017, wildfires in California have resulted in over $30 billion in insured losses, according to the reinsurance company Munich Re. In response, several large insurance companies, including Allstate, State Farm, and Chubb, have reduced their home insurance business in the state or halted the sale of new policies to avoid paying for wildfire damage.

Homeowners in California and other wildfire-prone areas may struggle to find affordable insurance or have their coverage limited or excluded from their policies. The California FAIR Plan offers wildfire coverage for those who cannot obtain it through their regular insurance. Additionally, homes in areas prone to wildfires may require a separate endorsement, a stand-alone deductible, or higher premiums to account for the increased risk.

Natural disasters, such as hurricanes, wildfires, tornadoes, and flooding, pose a significant risk to homeowners across the United States. As the frequency and severity of these events increase due to climate change, insurance companies are faced with higher payouts and uncertainty about future losses. This, in turn, leads to higher premiums for homeowners, especially those in high-risk areas.

Homeowners insurance policies typically cover fire and wind damage, but they often exclude coverage for natural disasters such as earthquakes, floods, mudflows, landslides, and tsunamis. It is important for homeowners to understand their policies, know their risks, and consider purchasing additional coverage for valuable items or specific natural disasters that may not be included in their standard policy.

Understanding Mortgage Insurance: Prepaid Finance Charges Explained

You may want to see also

Explore related products

![]()

Individual rating factors and marital status

Homeowners' insurance rates have been increasing dramatically, with a 23% increase from January 2023. The Consumer Federation of America (CFA) reported that insurance rates are rising faster than inflation in several US states. The CFA also identified the five most expensive states for home insurance as Florida, Louisiana, Oklahoma, Kentucky, and Nebraska.

Several factors contribute to rising insurance rates. One significant factor is the increase in weather-related damage and costly insurance claims due to severe weather events. As the frequency and severity of weather-related disasters rise, so does the overall cost of insurance. Additionally, the construction industry faces challenges, including a skilled labor shortage, supply chain issues, and rising material costs, all of which drive up the costs of home repairs and reconstruction. These market conditions directly impact insurance premiums.

Individual rating factors play a crucial role in determining homeowners' insurance rates. One such factor is an individual's credit history and insurance score. Insurance companies in most states consider an individual's credit history when calculating monthly premiums. While insurance scores are distinct from FICO credit scores, they share some common criteria. However, it's important to note that California, Maryland, and Massachusetts do not allow credit history to influence home insurance rates.

Marital status is another individual rating factor that can impact homeowners' insurance rates. Insurers typically offer lower rates to married couples because statistical data indicates a lower likelihood of filing claims compared to unmarried homeowners. Married individuals are often viewed as more stable, responsible, and less risky by insurance companies. This perception results in financial breaks for married couples, similar to those they may receive with their taxes. However, it's worth noting that Hawaii and Massachusetts prohibit the use of marital status as a rating factor in homeowners' insurance.

While marital status can influence insurance rates, it's important to recognize that it is just one aspect of a comprehensive risk assessment. Insurance companies consider various other factors, such as the location, age, and construction type of the home, as well as personal factors about the homeowner, claims history, and the chosen coverage level. By understanding these individual rating factors, homeowners can make informed decisions and explore options to keep their insurance costs manageable.

Home Insurance: Is Your Phone Covered?

You may want to see also

Frequently asked questions

There are several factors behind the rising rates of homeowner's insurance. These include severe weather events, the rising cost of building materials, supply chain issues, and unfilled jobs in the construction industry.

Home insurance rates have spiked 40.4% cumulatively across the US. In 2023, there was a 23% increase in rates. In 2025, Insurify projected premium increases in all 50 states, with an average increase of 8%.

The most expensive states for home insurance are Florida, Louisiana, Oklahoma, Kentucky, and Nebraska. In 2025, the average cost of home insurance in Oklahoma was $6,133, while Nebraska was close behind at $5,912.

You can lower your premium by increasing your deductible, which is the amount you pay out of pocket for claims. Additionally, you can pay for minor repairs yourself instead of going through insurance, as home insurance claims make your rate go up.

It is difficult to predict the future of homeowner's insurance rates, but some experts are optimistic for better prices. In the short term, homeowners can take steps to maintain and upkeep their homes to keep costs down.