Personal liability insurance is often included as standard in homeowners insurance policies, protecting you from lawsuits if you or your family members are responsible for someone else's injuries or property damage. It covers bodily injury caused to someone else or damage to the property of others. It also covers incidents that occur away from your home. The average cost of homeowners insurance in the US is $2,110 per year, with a $300,000 liability limit, but it doesn't cost much to add more coverage. Homeowners can also purchase personal liability insurance as a standalone policy if they need higher coverage limits.

| Characteristics | Values |

|---|---|

| Average annual cost of homeowners insurance in the U.S. | $2,110 |

| Average liability limit | $300,000 |

| Cost of increasing liability limit to $500,000 | Negligible |

| Home insurance deductible | Paid by the insured in case of property damage claims |

| Other names for personal liability insurance | Coverage E |

| What it covers | Lawsuits, injuries to others, damage to others' property |

| What it doesn't cover | Injuries to self or family, business claims, car accidents, commercial claims, intentional damage, transmission of contagious diseases |

| Typical coverage limits | $100,000, $300,000, and $500,000 |

| Recommended coverage | At least $300,000 to $500,000 worth of liability coverage |

| Cost-saving factors | Fencing around swimming pools, securing trampolines with nets |

Explore related products

$14.99 $14.99

What You'll Learn

- Personal liability insurance covers lawsuits if you injure someone or damage their property

- It does not cover intentional damage or business claims

- The average cost of homeowners insurance in the US is $2,110 per year

- Homeowners insurance policies usually provide a minimum of $100,000 of liability insurance

- You can lower the risk of 'attractive nuisances' by adding fencing around a pool or securing a trampoline

![]()

Personal liability insurance covers lawsuits if you injure someone or damage their property

Personal liability insurance is a standard part of homeowners insurance. It covers lawsuits if you injure someone or damage their property. It also covers everyone in your household, including children and pets. For example, if your child hits a baseball through a neighbour's window, your personal liability insurance will cover the damage. It also covers dog bites, although some insurers may limit coverage to certain breeds.

Personal liability insurance also covers medical expenses and lost wages if someone is injured on your property. For instance, if a delivery person slips and falls on your icy front steps, they could file a lawsuit accusing you of negligence. Your personal liability insurance would cover your legal defence and pay up to your policy limit if a court finds you liable for the injury.

However, personal liability insurance does not cover injuries or damages to yourself or your family. It also does not cover claims related to your business or profession. If you run a business from home, you will need separate business insurance to cover any lawsuits connected to your business pursuits.

When choosing a personal liability insurance policy, it is recommended to select a coverage limit that matches or exceeds your total net worth to ensure your assets are well-protected. Common coverage limits offered by homeowners and renters policies include $100,000, $300,000, and $500,000. You can also purchase an umbrella insurance policy to extend your coverage beyond $500,000.

Mortgage Insurance Options: Down Payment Impact

You may want to see also

Explore related products

![]()

It does not cover intentional damage or business claims

Personal liability insurance is typically included in homeowners insurance policies and offers financial protection in case of lawsuits. It covers scenarios where someone is injured or their property is damaged due to the policyholder's actions or negligence. However, it is important to note that personal liability insurance does not cover intentional damage or business claims.

Intentional damage refers to willful acts of harm, where an individual makes a conscious decision to cause injury or property damage. For example, if a driver deliberately drives their vehicle into a crowd of people or another person's property, it is considered an intentional act. In such cases, insurance companies will likely deny claims for healthcare costs, vehicle damage, or property damage.

Homeowners insurance policies specifically exclude coverage for business-related activities and claims. This means that any claims arising from your business operations or profession are not covered by your personal liability insurance. If you run a business from your home, you may need to purchase additional coverage or endorsements to protect your business activities and assets.

Business endorsements can provide coverage for limited business activities taking place within your home or other structures on your property. They may also offer increased limits for business property coverage, including protection for business income, important records, and extra expenses. However, it's important to note that theft by employees, dishonest acts, and commercial or professional liability may be excluded from such endorsements.

To ensure adequate coverage, business owners should carefully review their homeowners insurance policy and consider purchasing additional coverage or endorsements specifically designed for home-based businesses. These options can provide the necessary protection for business-related claims that are not covered by standard personal liability insurance.

Why Mortgage Lenders Spam You About Insurance

You may want to see also

Explore related products

![]()

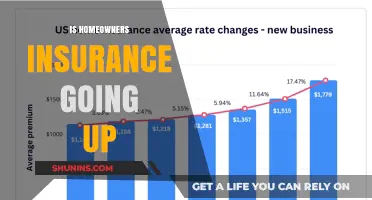

The average cost of homeowners insurance in the US is $2,110 per year

Personal liability insurance is typically included as standard in homeowners insurance policies, but it can also be purchased as a separate policy if higher coverage limits are required. This type of insurance covers lawsuits and financial costs if you or members of your household are found responsible for injuring someone else or damaging their property. It also covers incidents that occur away from your home, although it does not extend to car accidents or business-related claims.

The personal liability portion of homeowners insurance also covers bodily injury or property damage caused by pets and family members, as well as court costs and damages awarded. It is important to note that personal liability insurance does not cover intentional damage or the transmission of contagious diseases.

Homeowners insurance policies also offer additional coverages, such as personal property coverage, which insures items like furniture, clothing, and kitchen appliances. Additional living expenses (ALE) coverage pays for temporary living costs if you are unable to live in your home due to an insured disaster, such as a fire or severe storm. It is recommended to consider the limits and exclusions of your policy to determine if additional coverage is needed.

Upgrading Your Engine: Should You Inform Your Insurer?

You may want to see also

Explore related products

![]()

Homeowners insurance policies usually provide a minimum of $100,000 of liability insurance

Homeowners insurance policies typically include a minimum of $100,000 of personal liability insurance. This coverage offers financial protection in the event of lawsuits arising from bodily injury or property damage caused by you, your family members, or pets to others. It covers incidents both on and off your property, providing comprehensive security.

Personal liability insurance is an essential component of homeowners insurance, safeguarding you from unforeseen circumstances. It covers a range of scenarios, from dog bites to guests injuring themselves on your property. Notably, it does not cover intentional damage or business-related claims. However, it may help with medical payments, providing versatility in protecting your financial assets.

While the standard minimum of $100,000 is a common starting point, it is worth considering your specific circumstances. If you have enticing features on your property, such as a swimming pool or trampoline, you may want to increase your liability coverage to mitigate the elevated risk. Additionally, if your net worth exceeds the liability limit, consider opting for higher coverage of $300,000 or $500,000 to fully protect your assets.

Umbrella insurance policies are an option for those seeking coverage beyond $500,000. These policies extend your liability limits, providing additional peace of mind. The cost of an umbrella policy is influenced by the amount of underlying insurance you have and your risk profile. By increasing your underlying liability coverage, you can often obtain a more affordable umbrella policy.

It is important to review your homeowners insurance policy's declarations page to understand your personal liability coverage and limits. This proactive approach ensures you have adequate protection and can make adjustments if necessary.

Understanding Home Insurance Due Dates and Payments

You may want to see also

Explore related products

![]()

You can lower the risk of 'attractive nuisances' by adding fencing around a pool or securing a trampoline

Personal liability insurance is typically included in homeowners insurance policies, covering scenarios such as dog bites or injuries sustained by visitors on your property. The average cost of homeowners insurance in the US is $2,110 per year, with a $300,000 liability limit. Increasing this limit to $500,000 does not significantly impact your premium.

However, certain features on your property, such as swimming pools and trampolines, can increase your risk of liability claims from injured children, even if they are trespassing. These are known as "attractive nuisances." To lower this risk, you can take the following precautions:

- Install fencing around your pool: Ensure the fence is at least four feet tall and difficult to climb, with a locking gate. Consider adding an alarm to the gate and covering the pool with a safety cover when not in use.

- Secure your trampoline: Install a safety net around the trampoline and ensure it is placed on level ground. Consider enclosing the trampoline within a locked and alarmed fence to deter unauthorised use.

- Take general safety measures: Keep rescue equipment, such as a life ring with throw ropes, near the pool area. Remove pool toys from the deck and pool area after swimming to make the area less inviting to children. Store all pool chemicals safely out of reach.

By implementing these measures, you can help reduce the risk of accidents and lower your liability exposure as a homeowner. It is also advisable to review your insurance policy and consider increasing your personal liability coverage limit to account for the presence of attractive nuisances on your property.

Understanding Insurance Aging Reports: Financial Health Insights

You may want to see also

Frequently asked questions

Personal liability insurance is often included in homeowners insurance policies and offers financial protection in case of lawsuits if you injure someone else or damage their property.

Most homeowners insurance policies provide a minimum of $100,000 worth of liability insurance, but higher amounts are available. Increasingly, it is recommended that homeowners consider purchasing at least $300,000 to $500,000 worth of liability coverage.

Personal liability insurance does not cover intentional damage, such as in a fight, or the transmission of a contagious disease. It also does not extend coverage to car accidents or business or commercial claims.

It is recommended that you select a coverage limit that matches or exceeds your net worth. For instance, if your total net worth is $150,000, you should opt for at least $300,000 in coverage to fully protect your assets.

If you have any enticing backyard features, such as a swimming pool or trampoline, you may be considered a higher risk and your insurance costs could be higher. Taking basic precautions, such as adding fencing or a net, may help to reduce the cost of your insurance policy.