Homeowners' insurance, also known as home insurance, is a type of property insurance that covers a private residence. It is a contract of indemnity that combines various personal insurance protections, including losses occurring to one's home, its contents, loss of use, and liability insurance for accidents that may happen at the home or at the hands of the homeowner within the policy territory. Although not legally required in any state, it is often a prerequisite for a home loan. Hazard insurance is another term used to refer to dwelling coverage under a homeowners insurance policy, which covers the physical structure of the home against certain perils.

| Characteristics | Values |

|---|---|

| Other names | Hazard insurance, dwelling coverage, home insurance, HOI |

| What it covers | Physical structure of the home, personal property, liability insurance, loss of use, loss of other personal possessions |

| Cost | Depends on the replacement cost of the house, additional endorsements, and riders attached to the policy |

| Policy types | HO-1, HO-2, HO-3, HO-4, HO-5, HO-6, HO-7, HO-8 |

| Most common type | HO-3 |

Explore related products

![]()

Hazard insurance

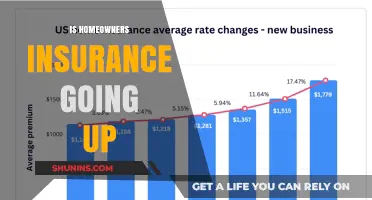

The cost of hazard insurance is influenced by several factors, including the replacement cost of your home, location, and risk factors. If your home is in an area prone to natural disasters, this can affect your insurance rates. The coverage amount and deductible you choose will also impact the premium. It is crucial to carefully review your policy to understand the specifics and determine if additional coverage is needed.

While homeowners insurance is not legally required in any state, it is often required as part of your loan agreement with your mortgage lender. Even if your home is paid off, it is still a good idea to carry homeowners insurance to protect your valuable asset against covered perils and potential liabilities.

Understanding Mortgage Insurance: Cash Gifts and Their Impact

You may want to see also

Explore related products

![]()

Home insurance

Homeowner's insurance, on the other hand, is a multiple-line insurance policy, meaning it includes both property insurance and liability coverage. It combines various personal insurance protections, including losses occurring to one's home, its contents, loss of use (additional living expenses), or loss of other personal possessions of the homeowner. It also provides financial protection against disasters and accidents that may happen at home or at the hands of the homeowner within the policy territory.

The cost of homeowner's insurance often depends on the replacement cost of the house and any additional endorsements or riders attached to the policy. It is adjusted to reflect the replacement cost, usually upon applying an inflation factor or a cost index. Major factors in price estimation include location, coverage, and the amount of insurance, based on the estimated cost to rebuild the home. Homeowner's insurance policies come in eight different forms, from HO-1 (basic form) to HO-8, each offering distinct coverage levels and protection types.

The type of homeowner's insurance policy determines the covered perils and reimbursement values. Named peril policies cover only those explicitly listed, while open peril policies cover all perils except those listed as exclusions. The reimbursement method determines how much can be claimed, with Actual Cash Value (ACV) based on current value, and Replacement Cost Value (RCV) based on the replacement cost without depreciation. HO-3 is the most common form of homeowner's insurance, offering comprehensive coverage for most homeowners' needs. It provides open peril coverage for the dwelling and named peril coverage for personal property.

Reporting Insurance Fraud in South Africa: What You Need to Know

You may want to see also

Explore related products

![]()

HO-3 insurance

HO-3 policies are typically written on an open-perils basis for the dwelling and a named-perils basis for personal property. This means that the insurance company will pay for damage to the home unless the peril is listed as an exclusion by the policy. On the other hand, personal property protection will only cover damage related to the losses specifically listed in the policy.

Home Insurance: What Happens When the Owner Dies?

You may want to see also

Explore related products

![]()

Mortgage insurance

Home insurance, also known as homeowner's insurance, is not the same as mortgage insurance. Home insurance is a type of property insurance that covers a private residence. It combines various personal insurance protections, including losses occurring to one's home, its contents, loss of use, and loss of other personal possessions. It also includes liability insurance for accidents that may happen at home or at the hands of the homeowner.

There are several types of mortgage insurance, including:

- Private mortgage insurance (PMI): This type of insurance is arranged by the lender and issued by private insurance companies. It is required when the down payment is less than 20% of the property's selling price, and it protects the lender.

- Federal Housing Administration (FHA) mortgage insurance: This type of insurance is required for all FHA loans and includes an upfront cost paid at closing, as well as a monthly cost included in the monthly payment.

- Qualified mortgage insurance premium (MIP) insurance: This type of insurance is required for loans backed by the Federal Housing Administration (FHA).

- Mortgage title insurance: This type of insurance protects against loss if a sale is invalidated due to a problem with the title. It ensures that the beneficiary does not suffer losses if it is determined that someone other than the seller owns the property.

- Department of Veterans' Affairs (VA)-backed loan: With this type of loan, the VA guarantee replaces mortgage insurance. There is no monthly mortgage insurance premium, but an upfront "funding fee" is paid, which can vary based on different factors.

It is important to note that mortgage insurance should not be confused with mortgage life insurance, which protects heirs if the borrower dies while owing mortgage payments.

Aflac Pregnancy Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Property insurance

Homeowner's insurance typically covers losses occurring to one's home, its contents, loss of use, or loss of other personal possessions of the homeowner. It also provides financial protection against disasters and liability insurance for accidents that may happen at the home or caused by the homeowner within the policy territory. While not legally required, homeowner's insurance is often necessary as part of a loan agreement with a mortgage lender.

There are several types of homeowner's insurance policies, including HO-1, HO-2, HO-3, HO-4, and HO-5. HO-1 is the most basic form of homeowner's insurance, covering only specific named perils. HO-2, also known as broad form insurance, provides coverage for a broader variety of perils compared to HO-1. HO-3 is the most common type of homeowner's insurance and offers comprehensive coverage for the dwelling and personal property. HO-4 is commonly known as renter's insurance, specifically designed for individuals renting or leasing a home. Finally, HO-5 is a more comprehensive policy, providing coverage for both the home and personal belongings at their replacement cost.

It is important to note that hazard insurance, popularized by mortgage lenders, refers to dwelling coverage under a homeowner's insurance policy. It protects the physical structure of the home against certain perils but is not a separate type of insurance. When purchasing homeowner's insurance, it is essential to consider factors such as property type, coverage needs, and budget to choose the most suitable policy.

Transferring Homeowners Insurance to a New Owner: Is It Possible?

You may want to see also

Frequently asked questions

Home insurance.

There is no difference. Home insurance is just another name for homeowners' insurance.

Hazard insurance is dwelling coverage under your homeowners' insurance policy. It covers the physical structure of your home against certain perils.

Fire, lightning, weight of ice, snow and sleet.

HO-3 is the most common homeowners' insurance form. It offers open peril coverage for the dwelling and named peril coverage for personal property.