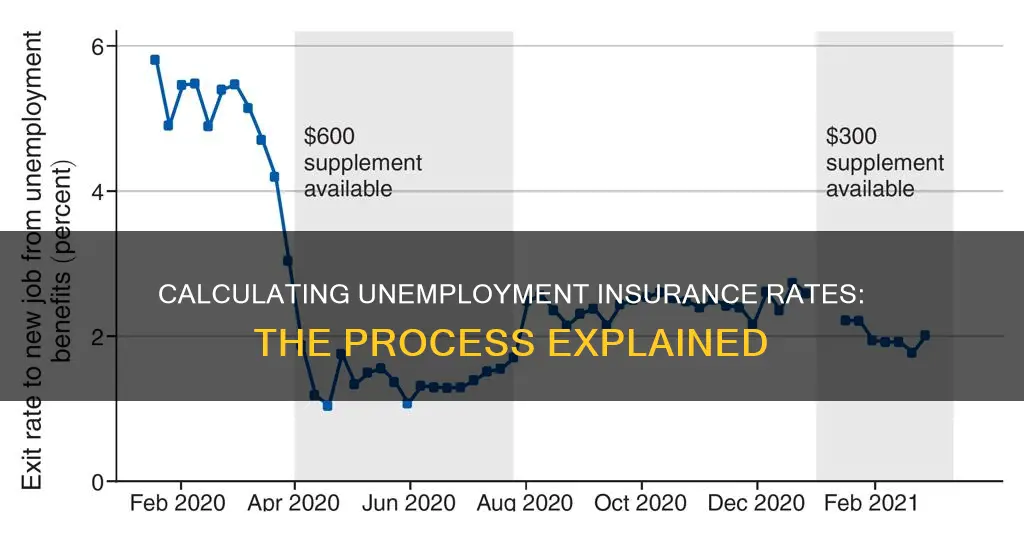

Unemployment insurance rates are calculated based on various factors, including employment status, earnings, and state-specific criteria. In the United States, unemployment insurance benefits are typically determined by an individual's wages during a defined base period, which may vary by state. Employers also play a role in unemployment insurance rates, as they are responsible for paying state and federal unemployment taxes, which fund these programs. These tax rates can differ based on industry, state, and other factors, with some states employing unique systems for new employers. Understanding unemployment insurance rates is crucial for both employees seeking benefits and employers navigating their tax obligations.

| Characteristics | Values |

|---|---|

| Eligibility | To be eligible for unemployment insurance benefits, you must have had sufficient earnings as an employee in the four calendar quarters before you applied for benefits. |

| Benefit Calculation | If eligible, you will receive a weekly benefit amount of approximately 50% of your average weekly wage, up to a maximum set by law. |

| Maximum Weekly Benefit | As of October 1, 2024, the maximum weekly benefit amount is $1,051 per week. |

| Base Period | The base period is defined by law and is typically the last four completed calendar quarters before the effective date of your claim. |

| Benefit Credit | The benefit credit is the total amount of benefits you are eligible to receive. |

| WorkShare Benefits | Under WorkShare, your weekly benefit rate is a percentage of your regular unemployment insurance benefit rate, based on the proportion of lost hours. |

| Maximum Duration | You can collect WorkShare benefits up to the duration of your WorkShare plan or up to a 52-week maximum. |

| State Unemployment Insurance Rates | State unemployment insurance rates vary by state, industry, and other factors. Each state assigns a unique rate to businesses. |

| New Employer Rates | Many states provide new employers with a standard rate, which may differ for construction and non-construction industries. |

| Federal Unemployment Taxes | Employers must pay federal unemployment taxes if they meet certain criteria, such as paying wages above a specified threshold or having a minimum number of employees. |

| State Unemployment Taxes | Employers are generally responsible for paying state unemployment taxes, which fund unemployment programs and benefit payments. |

| Tax Rate Determination | An employer's tax rate determines their state unemployment insurance tax liability, calculated by multiplying taxable wages by the tax rate. |

| Taxable Wages | The maximum amount of taxable wages per employee per calendar year is set by statute and may vary by state. |

Explore related products

What You'll Learn

![]()

Eligibility for unemployment insurance

In Massachusetts, for example, to be eligible for unemployment insurance benefits, a worker must have earned enough in the four calendar quarters before they apply for benefits. The law assumes that any worker who provided services for an employer was an employee, and that the pay they received counts toward their eligibility for unemployment benefits. Their status as an employee does not depend on whether their employer tells them that they are an employee or independent contractor, reports their income on a 1099 tax form instead of a W-2, pays them in cash, or tells them that they are not eligible for unemployment insurance or other benefits.

In California, eligibility requirements for unemployment benefits include earning enough wages, being unemployed through no fault of one's own, and looking for work. To receive unemployment benefits, one must have a Social Security number or authorization to work in the US, be fully or partially unemployed, be physically able and available to work, and be actively looking for work each week. They must also be ready and willing to accept work immediately.

In addition to these state-specific requirements, federal law also sets certain eligibility criteria. For example, federal law does not require an employee to quit in order to receive benefits due to the impact of COVID-19. The Federal-State Unemployment Insurance Program provides unemployment benefits to eligible workers who are unemployed through no fault of their own and meet other eligibility requirements of state law.

It is important to note that employers are generally responsible for paying state unemployment taxes, which fund unemployment programs and benefit payments to eligible employees. These taxes are based on a percentage of employee wages and are used to support workers who lose their jobs without cause. While most states have a standard new employer rate, some states, like Nebraska, differentiate between construction and non-construction industries when setting rates.

California's Commercial Auto Insurance Requirements: What You Need to Know

You may want to see also

Explore related products

![]()

Calculating unemployment insurance benefits

To calculate unemployment insurance benefits, several factors are considered. Firstly, eligibility is determined by earnings in the four calendar quarters before the application for benefits. This means that to be eligible for unemployment insurance benefits, an individual must have worked and earned wages during this period. The specific criteria for eligibility may vary by state and are often defined by state law. For example, in Massachusetts, the law assumes that an individual is an employee, and their wages during this period are considered for eligibility, regardless of their employer's classification of their employment status.

Once eligibility is established, the amount of the unemployment insurance benefit is calculated. This typically amounts to approximately 50% of the average weekly wage earned by the individual, up to a maximum set by law. This maximum amount can vary by state and is adjusted periodically. For instance, as of October 1, 2024, the maximum weekly benefit amount in Massachusetts is $1,051.

The calculation of the benefit amount also takes into account the base period, which is typically defined as the last four completed calendar quarters before the claim is filed. The primary base period is used to calculate the maximum benefit credit, which represents the total benefits an individual is eligible to receive. In some states, like Vermont, the calculation method involves dividing the total wages paid in the two highest quarters of the base period by 45.

Additionally, unemployment insurance benefits may be impacted by the WorkShare program, which calculates benefits based on the percentage of lost hours. For example, if an individual loses 20% of their weekly work hours, their WorkShare benefit would be 20% of their regular unemployment insurance benefit rate.

It is important to note that unemployment insurance benefits are separate from unemployment taxes, which are paid by employers to fund these benefit programs. These taxes are typically paid at a state level and may vary based on factors such as industry and the number of employees. While generally an employer-only tax, some states require additional withholdings from employee wages for state unemployment taxes.

Insuring a Friend's Car: Your Options

You may want to see also

Explore related products

![]()

Worker misclassification

Misclassification also has a broader impact on the economy. Law-abiding employers face a competitive disadvantage when competing for business or bidding for jobs against employers who misclassify. Misclassifying employers have artificially low costs because they have not covered the cost of unemployment insurance contributions and workers' compensation for their employees. This means that law-abiding businesses that properly classify their employees are subsidising businesses that misclassify and could end up paying higher unemployment insurance contributions, higher workers' compensation premiums, and higher taxes than would be required if all employers followed the law.

To combat worker misclassification, federal, state, and local policymakers should enforce the rights to which all workers are entitled under federal, state, and local labour laws. These laws provide extensive protections for employees, including the minimum wage, overtime pay, eligibility for state and federal unemployment insurance, Workers’ Compensation coverage, and employer contributions toward Social Security and Medicare.

Workers who believe they have been misclassified can apply for unemployment benefits. If they meet the eligibility requirements for unemployment benefits, including having been paid enough wages by an employer, they can apply through UI Online, by phone, or by mailing or faxing a paper application form. They should include proof of wages (like W-2, 1099, pay stubs, cash receipts, or other documents showing earnings) and any information about their work history. If they disagree with any information on the award notice, they should mail a letter to the relevant authority within 30 days of the mail date at the top of the form.

Understanding SR-22 Auto Insurance Requirements

You may want to see also

Explore related products

![]()

Voluntary payments

Voluntary unemployment insurance contributions are a way for employers to reduce their unemployment tax rate. In 2022, 27 states allowed voluntary unemployment contributions. However, the deadline has passed in some of these states, including Missouri, Nebraska, Ohio, and South Dakota. States such as California and Louisiana also have certain rules that do not permit voluntary contributions under certain conditions. For example, in California, if a certain tax rate schedule is in effect, employers are not allowed to make voluntary contributions. In 2021, the state of Washington made its unemployment voluntary contribution program more appealing by waiving a surcharge fee, reducing the minimum rate class buy down, and extending the deadline to apply.

The impact of voluntary contributions varies depending on the state. In reserve-ration states, a voluntary contribution increases the balance in the employer's reserve, resulting in a lower rate being assigned. In benefit-ration states, an employer pays voluntary contributions to cancel benefit charges to its account, thereby reducing its benefit ratio. Some states, such as Wisconsin, New Jersey, and North Carolina, provide forms or online tools to help employers determine if a voluntary contribution will help lower their unemployment tax rate.

It is important for employers to understand the potential impact of making a voluntary contribution, as no refunds can be made if it does not lead to a reduced rate or if the employer changes their mind. Employers should also be aware that their state will eventually change their new employer rate, and they will receive a new SUTA tax rate each year.

Overall, voluntary unemployment insurance contributions can be a useful strategy for employers to reduce their unemployment tax burden, but it is important to understand the specific rules and guidelines of the state in which they operate.

Lower Auto Insurance Premiums: Infinity's Guide to Savings

You may want to see also

Explore related products

![]()

State unemployment insurance rates for new employers

State unemployment insurance rates, also known as SUI or SUTA, are taxes that employers are responsible for paying when running payroll. These taxes are used to fund unemployment programs and pay out benefits to employees who lose their jobs without fault of their own. While SUI rates can vary by state, industry, and other factors, new employers can generally expect to be assigned a standard new employer SUTA tax rate by their state.

For example, in Nebraska, new employers receive a SUTA rate of 1.25%, while new construction employers receive a rate of 5.4%. Some states, like Alaska, New Jersey, and Pennsylvania, require that employers withhold additional money from employee wages for state unemployment taxes. Each state sets its own range of tax rates, which may be based on factors such as the number of employees or the industry.

States also set wage bases for unemployment tax, meaning that employers only contribute unemployment tax until the employee earns above a certain amount. If your employees work in multiple states, you will need to pay SUTA tax to each state in which your employees work.

While specific SUTA tax rate information for each state is not readily available, it is recommended to contact your state for more information on included and additional assessments. Additionally, you can use resources such as the New Employer Information by State for Payroll to learn more about state-specific requirements.

Unlicensed and Uninsured: Understanding Auto Insurance Coverage for Unlicensed Drivers

You may want to see also

Frequently asked questions

The Unemployment Insurance contribution rate is the normal rate plus the subsidiary rate. This rate is used to calculate line #4 on the Quarterly Combined Withholding; Wage Reporting and Unemployment Insurance Report NYS 45.

If you are eligible to receive unemployment insurance (UI) benefits, you will receive a weekly benefit amount of approximately 50% of your average weekly wage, up to the maximum set by law. As of 1 October 2024, the maximum weekly benefit amount is $1,051 per week. The amount of UI benefits you may be eligible to receive is determined by wages paid to you during either your primary or alternate base period.

Many states give newly registered employers a standard new employer rate. The state unemployment insurance rate for new employers varies. For example, new employers receive a SUTA rate of 1.25% in Nebraska, but all new construction employers receive a SUTA rate of 5.4%.