The Health Insurance Marketplace, established by the Affordable Care Act (ACA), offers a range of affordable health insurance options. The ACA provides special protections for insured individuals, including prohibitions on coverage refusals based on sex or pre-existing conditions, and no lifetime or annual limits on essential health benefits. The Open Enrollment Period allows individuals to enroll in or change their health plans for the coming year. During this period, consumers can benefit from increased choices of health insurance issuers and plan options. Additionally, unbiased experts known as Navigators assist consumers, especially those in underserved communities, in understanding their benefits, reviewing plans, and enrolling in Marketplace coverage.

| Characteristics | Values |

|---|---|

| Website | Healthcare.gov |

| Enrollment period | November 1 to January 15 |

| Eligibility | US citizen or national, lawfully present, not incarcerated |

| Enrollment qualifications | Must select a plan before deadline |

| Enrollment benefits | No tax penalty for not having health coverage, tax credits, cost-sharing reductions, protection from refusal of coverage based on sex or pre-existing condition, no lifetime or annual limits on coverage for essential health benefits, young adults can stay on family insurance until age 26 |

| Enrollment assistance | Navigators, certified assisters or agents |

Explore related products

What You'll Learn

![]()

Eligibility requirements: US citizen, lawfully present, not incarcerated

To be eligible to enroll in health coverage through the Marketplace, you must fulfill certain requirements. Firstly, you must be a U.S. citizen, a U.S. national, or be lawfully present in the country. Lawful permanent residence, also known as having a "green card," is generally granted to those who have lived in the U.S. for a specific period and have met other eligibility criteria. Those with "qualified non-citizen" status, such as refugees, asylees, and victims of trafficking, are also considered lawfully present. Additionally, lawfully present immigrant status applies to those with "non-immigrant" status, including individuals with work visas or student visas.

It is important to note that undocumented individuals are not considered lawful residents and are therefore not eligible for federally funded programs like Affordable Care Act marketplaces or Medicare. However, some states, like California, have started to establish their own programs that provide health coverage regardless of immigration status. Furthermore, certain states have removed the waiting period for Medicaid or CHIP eligibility for individuals who are "lawfully residing" in the U.S.

To enroll in a Marketplace plan, you must also not be incarcerated. Additionally, having Medicare coverage disqualifies you from enrolling in a Marketplace plan. It is worth mentioning that gaining U.S. citizenship or lawful presence triggers a special enrollment period for Marketplace coverage.

If you are a lawfully present immigrant, you may qualify for lower costs on monthly premiums and extra savings on out-of-pocket costs based on your income. Federal poverty levels are used to determine eligibility for savings on Marketplace health insurance and certain programs like Medicaid and CHIP.

U.S. Insurance Giant USAA's Global Reach

You may want to see also

Explore related products

![]()

Enrollment periods: open, special, deadlines

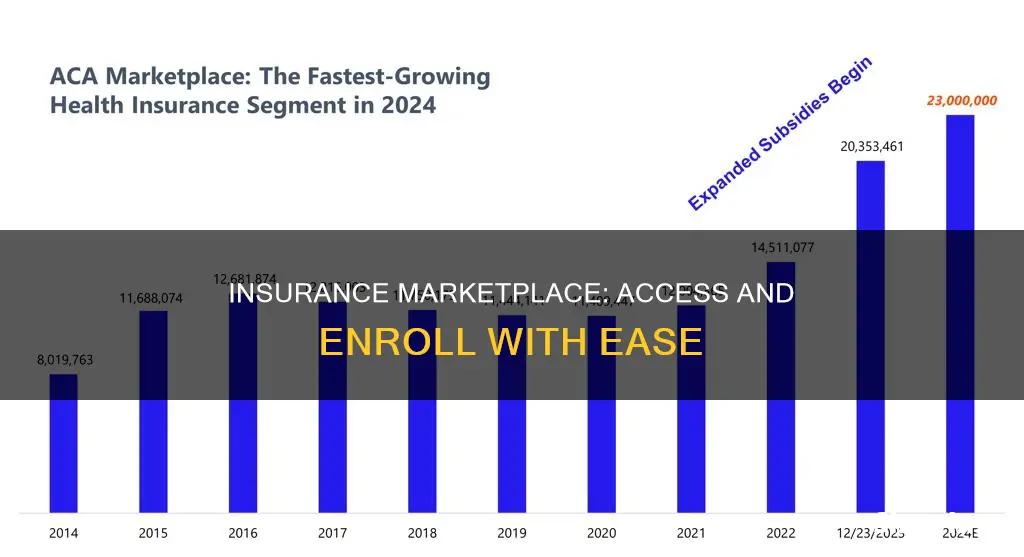

The Health Insurance Marketplace's open enrollment period is the time of year when anyone can enroll in a health insurance plan. The open enrollment period for 2025 in most states is November 1 to January 15. However, some state-run exchanges have different schedules. For example, in 2025, open enrollment in Virginia ended on January 22, while in Idaho it ended in December.

If you enroll by December 15, your coverage can start from January 1. If you enroll by January 15, your coverage can start from February 1.

Outside of the yearly open enrollment period, you can still sign up for health insurance during a Special Enrollment Period. You may qualify for a Special Enrollment Period if you've had certain life events, including losing health coverage, moving, getting married, having a baby, or adopting a child. You may also qualify if your household income is below a certain amount. For example, in 2025, consumers with an annual income up to 200% of the Federal Poverty Level ($30,120 for an individual or $62,400 for a family of four) can qualify for a Special Enrollment Period and access nearly free health plans throughout the year. If you qualify for a Special Enrollment Period, you usually have up to 60 days after the event to enroll or change your plan.

To get started, go to Healthcare.gov to find your state Health Insurance Marketplace. Each state's marketplace has its own enrollment instructions.

Bank Insurance: Is Your Phone Covered?

You may want to see also

Explore related products

![]()

Payment: tax credits, monthly premiums, cost-sharing

When you apply for insurance on HealthCare.gov, you will need to fill out an application and provide household and income information. This will determine whether you qualify for a tax credit to lower your monthly insurance payment (premium). The size of your premium tax credit is based on a sliding scale, so those with lower incomes get larger credits to help cover the cost of their insurance.

After you fill out your application, you will be informed of the estimated amount of Premium Tax Credit you may be able to claim for the tax year. This will be based on the information you provide about your family composition, projected household income, and other factors. You can then decide how much of your estimated credit you would like to be paid in advance directly to your insurance company to lower your monthly premiums. You will be required to file Form 8962 with your income tax return to reconcile the amount of advance payments with the Premium Tax Credit that you may claim based on your actual household income and family size.

If you qualify for savings on out-of-pocket costs and enroll in a Silver plan, you will benefit from a lower deductible. This means the insurance plan starts to pay its share of your medical costs sooner. For example, if a Silver plan has a deductible of $750, you would usually need to pay the first $750 of medical care yourself before the insurance company pays anything. However, if you qualify for cost-sharing reductions, your deductible could be lowered to $300 or $500, depending on your income. You will also benefit from lower copayments or coinsurance. These are the payments you make each time you get care, such as $30 for a doctor's visit. If you enroll in a plan with cost-sharing reductions, you may only need to pay $20 or $15 for a doctor's visit.

It is important to note that cost-sharing reductions are not provided as a tax credit and do not need to be reconciled when filing taxes for the year they were received.

Insured Chicagoans: Northside's Health Coverage

You may want to see also

Explore related products

![]()

Plan options: at least three issuers, Medicaid, CHIP

When it comes to plan options, the Health Insurance Marketplace offers a range of choices to meet diverse needs. Firstly, individuals have the option to select from multiple issuers, with 97% of HealthCare.gov consumers having access to at least three health insurance issuers for 2025. This allows for a diverse selection of plans with varying coverage options and provider networks, ensuring that individuals can find a plan that aligns with their specific healthcare needs and preferences.

Medicaid is another essential plan option available through the Health Insurance Marketplace. Medicaid is a federal-state collaboration that provides free or low-cost health coverage to individuals and families who meet specific income and eligibility criteria. Each state sets its own eligibility standards, and in many states, individuals with incomes just above the Medicaid threshold can still obtain affordable coverage through the Marketplace. Additionally, all states are required to offer Medicaid coverage to young people transitioning from foster care to adulthood until they turn 26, as long as certain conditions are met.

The Children's Health Insurance Program (CHIP) is a joint federal-state program that fills a critical gap in healthcare coverage for children and, in some states, pregnant women. CHIP targets families with incomes too high to qualify for Medicaid but too low to afford private insurance. CHIP eligibility is based on financial and non-financial criteria, and states have the flexibility to expand eligibility and implement various enrollment strategies to ensure that more individuals can access the coverage they need.

The Health Insurance Marketplace also offers cost-saving opportunities for those with limited Medicaid coverage. Individuals with limited benefits through Medicaid may qualify for reduced costs on their Marketplace plan based on income and other factors. This ensures that even those with limited access to Medicaid can still obtain affordable healthcare coverage through the Marketplace.

The Mystery of Insurance Billing Cycles: Unraveling Weekly vs. Monthly Payments

You may want to see also

Explore related products

![]()

Assistance: Navigators, certified assisters, virtual appointments

Navigators are experts who help consumers, especially those in underserved communities, understand their benefits and rights, review plan options, and enroll in Marketplace coverage. They are not licensed health insurance producers (agents/brokers), so they cannot recommend one plan over another or direct consumers toward a particular policy. Instead, they provide consumers with general information that can make it easier to understand what’s available in terms of coverage and financial assistance. They also provide outreach and education to raise awareness about the Marketplace, and refer consumers to health insurance ombudsman and consumer assistance programs when necessary.

Navigators are paid by state and federal grant programs, and they cannot be compensated by insurance companies. They must meet cultural competency standards and go through training and certification. CMS has awarded $100 million in Navigator cooperative agreement awards to 44 organizations who will serve as Navigator awardees in the 28 states with a FFM.

Certified application counselors (CACs) are a vital component of the assister community. They are designated organizations that help consumers navigate coverage transitions from Medicaid into Qualified Health Plans (QHPs) through the Federally-facilitated Marketplace (FFM). Agents and brokers also play a key role in the Health Insurance Marketplace. They educate consumers about Marketplaces and insurance affordability programs, and help consumers receive eligibility determinations and apply for premium tax credits.

Certified assisters, such as the PBIN team at Whitman-Walker, serve as DC Health Link Assisters, providing critical consumer outreach and enrollment assistance to uninsured and under-insured DC residents. They help with insurance enrollment, renewals, and reducing care costs. They can also help fix coverage problems, denials, and re-certifying/renewing coverage, as needed. They offer virtual appointments aimed at reducing transportation barriers and making it easier for consumers to get help signing up for quality, affordable healthcare coverage.

Amica Insurance in Florida: What You Need to Know

You may want to see also

Frequently asked questions

The Open Enrollment Period for the Health Insurance Marketplace usually runs from November 1 to January 15. The deadline for full-year coverage that starts in January of the following year is midnight on December 15.

To be eligible to enroll in health coverage through the Marketplace, you must be a U.S. citizen or national, or be lawfully present in the United States, and not be incarcerated. There is no income limit.

Each state's Marketplace has its own enrollment instructions. You can find your state's Health Insurance Marketplace on Healthcare.gov. You can also get free local help from a certified assister or agent.