There are several methods to calculate how much life insurance coverage you need, including the 10x rule, the Obligations-Earnings method, and the DIME method. The 10x rule is the most basic, where you multiply your annual salary by 10 to determine how much life insurance you need. The Obligations-Earnings method takes into account your future financial assets and obligations, while the DIME method considers your debts, income, mortgage, and education expenses. Ultimately, the amount of life insurance you need depends on your unique circumstances, such as your age, income, mortgage, debts, and anticipated funeral expenses.

| Characteristics | Values |

|---|---|

| Purpose | To calculate the amount of money your loved ones would need to remain on firm financial ground after you're gone |

| Factors | Annual income, number of years your dependents will need financial support, debt, future college costs, funeral needs, savings, other life insurance coverage, age, health, occupation, hobbies, number of children |

| Formula | Obligations – Earnings method, DIME method, 10x rule, Years-Until-Retirement method, Standard-of-Living method |

| Tips | Think of life insurance as part of your overall financial plan, don't skimp, talk numbers through with your family, consider buying multiple smaller life insurance policies |

Explore related products

What You'll Learn

![]()

Calculating life insurance for income replacement

Step 1: Understand the Purpose of Life Insurance

The primary purpose of life insurance is to replace your income and provide financial security for your dependents. It ensures that your beneficiaries can use the death benefit to pay for ongoing expenses and maintain their standard of living.

Step 2: Determine the Type of Life Insurance

There are two main types of life insurance: term life insurance and permanent life insurance. Term life insurance covers a set period, such as 10, 20, or 30 years, and is typically sufficient for most families. Permanent life insurance, on the other hand, lasts until a maximum age (usually 90-120) and tends to be more expensive.

Step 3: Calculate Your Annual Salary

To calculate the necessary coverage, start by considering your annual salary. This will form the basis for determining how much income replacement your beneficiaries will need.

Step 4: Multiply Annual Salary by Years of Coverage

One guideline for calculating coverage is to multiply your annual salary by the number of years you want to provide coverage. For example, if your annual salary is $60,000 and you want to provide five years of coverage, you would need a $300,000 policy.

Step 5: Account for Anticipated Raises and Expenses

Keep in mind that the calculation above only reflects your base salary. It is important to also consider any anticipated raises, promotions, or salary growth over time. Additionally, factor in other expenses such as college fees or childcare costs.

Step 6: Consider "Hidden Income"

Don't forget to include hidden income in your calculations. This refers to any amounts you receive beyond your base pay, such as 401(k) contributions or your employer's share of health insurance premiums. These amounts can significantly impact the cost of replacing your income.

Step 7: Evaluate Your Financial Situation

Your financial and family situation will play a significant role in determining the amount of life insurance you need. Consider your debts, mortgage, and other financial obligations. Additionally, take into account any existing life insurance policies or investments that your beneficiaries can rely on.

Step 8: Use a Life Insurance Calculator

While the above steps provide a general framework, you can also use a life insurance calculator to get a more precise estimate. These calculators consider factors such as your annual income, years of coverage, debts, future costs, savings, and existing life insurance coverage to determine the appropriate amount of life insurance for income replacement.

Remember, it is essential to reevaluate your life insurance needs periodically, especially if your job, income, or family situation changes. By following these steps, you can ensure that your loved ones will have the financial support they need in the event of your untimely death.

StateFarm's Life Insurance Offerings: What You Need to Know

You may want to see also

Explore related products

![]()

How to calculate life insurance for debt repayment

When calculating life insurance for debt repayment, it's important to consider your financial obligations and assets. This includes your annual salary, debts, future costs, savings, and existing life insurance coverage.

Step 1: Calculate your financial obligations

Start by adding up your annual salary multiplied by the number of years you want to replace that income. Then, include any debts you want to be covered, such as your mortgage balance, credit card debt, or loan amounts. Also, consider future needs such as college fees for your children and funeral costs. If you are a stay-at-home parent, calculate the cost of replacing services you provide, such as childcare.

Step 2: Assess your assets

Next, determine your liquid assets, such as savings and investment funds. Also, consider any existing college funds or life insurance policies that could be used to cover these expenses.

Step 3: Calculate the difference

Finally, subtract your total assets from your financial obligations. The resulting number is the amount of life insurance coverage you need to ensure your debts are repaid.

Keep in mind that this calculation is just an estimate, and it's always a good idea to consult with a licensed agent or financial planner to ensure your coverage level fits your specific needs. Additionally, life insurance rates vary based on factors such as age, health, occupation, and hobbies, so be sure to compare quotes from multiple companies to find the best coverage for your situation.

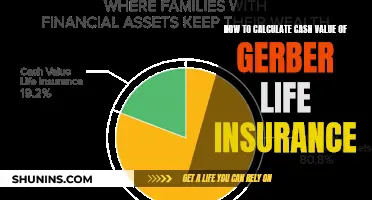

Gerber Life Insurance: Calculating Your Cash Value

You may want to see also

Explore related products

![]()

Factoring in funeral costs

When it comes to life insurance, factoring in funeral costs is a crucial consideration. The passing of a loved one is an emotionally challenging time, and the last thing you want is to burden your family with financial stress. Here's a detailed guide on how to factor funeral costs into your life insurance planning:

Understanding Funeral Costs

Funerals can be expensive, often costing upwards of $10,000. This includes various expenses such as the funeral service, burial or cremation, casket or urn, transportation, and other related fees. It's important to research the average funeral costs in your area to get an accurate sense of the financial burden.

Choosing the Right Insurance Policy

There are several types of life insurance policies available, and not all of them are designed to cover funeral expenses. Here are a few options to consider:

- Whole Life Insurance: This is a permanent life insurance policy that covers you for your entire life. It typically has higher premiums but guarantees a fixed rate throughout the policy. Whole life insurance often includes a portion of the premium set aside as a growing cash investment. This type of policy is ideal if you want to leave money to your heirs and can afford the higher premiums.

- Term Life Insurance: Term life insurance covers you for a chosen period, such as 20 or 30 years. It tends to be more affordable since it doesn't build cash value. This option is suitable if you only need short-term coverage or are on a tight budget. However, keep in mind that if you outlive the policy, there will be no payout for funeral expenses.

- Universal Life Insurance: Universal life insurance is another type of permanent coverage that offers more flexibility than whole life insurance. It allows you to adjust the death benefit and premium according to changes in your life. A portion of your premium goes into a cash account that grows at the market rate and can be borrowed against. However, it requires more attention to monitor the growth and manage fees.

- Burial Insurance/Final Expense Insurance: This type of insurance is specifically designed to cover funeral expenses and typically offers coverage from $5,000 to $25,000. It usually has an easy or non-existent application process, but it may only pay out a prorated amount based on the premiums paid. Burial insurance is a good option if you can't qualify for other policies or need a simple solution.

- Preneed Funeral Insurance: This insurance is purchased through a funeral home and covers services provided by that specific establishment. The payout goes directly to the funeral home rather than individual beneficiaries.

Calculating the Coverage Amount

When calculating how much life insurance you need for funeral costs, consider the following:

- Estimate Funeral Expenses: Research the average funeral costs in your area, including burial or cremation, casket or urn, funeral home fees, and other related expenses.

- Consider Additional End-of-Life Expenses: Funeral costs may also include medical bills, estate settlement costs, and other outstanding debts. Make sure to factor these into your calculations.

- Choose the Right Policy: As mentioned earlier, different types of life insurance policies have varying coverage amounts and premiums. Consider your financial situation, the desired coverage period, and whether you want to leave money to your heirs.

- Use Online Calculators: Many websites offer life insurance calculators that can help you estimate the coverage you need based on your income, debts, future costs, and savings. These calculators provide a more precise estimate by considering multiple factors.

Regularly Review and Update Your Policy

Life insurance needs may change over time, so it's essential to review and update your policy periodically. Significant life events, such as marriage, the birth of a child, or a change in financial circumstances, may require adjusting your coverage amount or policy type.

In conclusion, by carefully considering funeral costs and choosing the right life insurance policy, you can ensure that your loved ones have the financial support they need during a difficult time. Remember to seek advice from a licensed agent or financial planner to find the best coverage for your specific situation.

Life Insurance Surrender: Understanding the 10% Penalty

You may want to see also

Explore related products

![]()

Calculating life insurance for mortgage repayment

Understanding Life Insurance for Mortgage Repayment

Life insurance for mortgage repayment is designed to protect your loved ones in the event of your death. It ensures that the outstanding mortgage balance on your property is covered, providing financial security for your family. This type of insurance is typically recommended for homeowners with dependents, especially if their income contributes significantly to the household.

Factors to Consider

When calculating life insurance for mortgage repayment, there are several factors to take into account:

- Mortgage Balance: Calculate the remaining balance on your mortgage. This will give you an idea of the coverage amount needed to pay off the loan in full.

- Loan Tenure: Consider the remaining duration of your mortgage. Longer loan tenures may require higher coverage amounts to ensure the loan can be repaid in full.

- Income Replacement: If your income contributes significantly to household expenses, you may want to include income replacement in your calculation. Multiply your annual income by the number of years you want to replace that income for your dependents.

- Other Debts and Expenses: Besides the mortgage, consider any other debts or future expenses, such as college fees or funeral costs, that your loved ones might need financial assistance with.

- Existing Assets and Insurance: Don't forget to subtract any existing assets, such as savings or investments, and any current life insurance policies that could be used to cover these expenses.

Using a Calculator or Agent

To simplify the calculation process, you can use an online life insurance calculator. These tools will guide you through inputting relevant information, such as income, debts, future costs, savings, and insurance, to estimate the coverage amount needed. Alternatively, consider working with a licensed agent or financial planner who can help you assess your unique situation and determine the appropriate level of coverage.

Pros and Cons of Mortgage Life Insurance

Mortgage life insurance is specifically designed to pay off your mortgage if you pass away during the policy term. Some benefits include no medical exam requirement, level premiums, and the ability to add riders for customized coverage. However, there are also drawbacks, such as a decreasing payout as you pay down your mortgage, limited flexibility in how beneficiaries can use the death benefit, and potentially high costs.

Comparing with Other Policies

When considering mortgage life insurance, it's worth comparing it with traditional life insurance policies like term life insurance and whole life insurance. Term life insurance offers lower premiums and fixed periods, while whole life insurance lasts for the insured's lifetime, has level premiums, and includes a cash value growth component. These options may provide more flexibility in how the death benefit can be used and may be more cost-effective depending on your circumstances.

Full Force Life Insurance: Maximizing Your Coverage and Benefits

You may want to see also

Explore related products

![]()

Calculating life insurance for college fees

Step 1: Estimate Future College Costs

Start by researching the average cost of tuition, room and board, books, and other related expenses for the specific colleges or types of colleges your children might attend. Consider the potential increase in college fees over time due to inflation or other factors. This estimation will give you a rough idea of the future financial obligation for your child's education.

Step 2: Assess Your Current Savings and Investments

Take an inventory of your current financial situation, including any savings accounts, investment portfolios, or other liquid assets that could be used to pay for college fees. This step is crucial because it will help you understand how much additional coverage you need from life insurance to bridge the gap between your current assets and the estimated future college costs.

Step 3: Calculate the Coverage Gap

Subtract your total assets (from step 2) from the estimated future college costs (from step 1). This calculation will give you an idea of the coverage gap that life insurance needs to fill. For example, if you estimate that future college costs will be $100,000, and you currently have $40,000 in savings, the coverage gap would be $60,000.

Step 4: Choose an Appropriate Life Insurance Policy

When selecting a life insurance policy, you have two main options: term life insurance or permanent life insurance. Term life insurance covers a specific period, such as the duration of your child's college education, while permanent life insurance provides coverage for the insured's entire life. Consider the duration of coverage needed and the affordability of premiums when making your choice.

Step 5: Determine the Desired Coverage Amount

Based on the coverage gap calculated in step 3, decide on the desired coverage amount for your life insurance policy. You may also want to include additional funds to account for any potential increases in college fees or other unforeseen expenses.

Step 6: Obtain Life Insurance Quotes

Contact reputable insurance companies or brokers to obtain quotes for the desired coverage amount. Compare the premiums, policy terms, and conditions offered by different insurers. This step will help you find the most suitable policy for your needs at the best available rate.

Step 7: Regularly Review and Adjust Your Policy

Life insurance needs may change over time, so it's essential to review your policy periodically. As your children get older, the cost estimates for their college education may change, or you may accumulate more savings or investments. Adjusting your life insurance coverage ensures that it remains aligned with your evolving financial situation and goals.

ADHD and Life Insurance: Does It Impact Premiums?

You may want to see also

Frequently asked questions

The simplest method is the multiple-of-income approach, which aims to replace the primary breadwinner's salary for a predetermined number of years. You can calculate this by multiplying your annual income by the number of years you want to provide financial support to your survivors.

You can use the DIME method, which stands for Debt, Income, Mortgage, and Education. Calculate your total debt (excluding your mortgage), your annual income (multiplied by the number of years you want to provide income replacement), your mortgage balance, and the cost of your children's education. Add these amounts together to get your total life insurance needs.

One way to do this is by multiplying your annual income by the number of years left until your retirement. This will give you an estimate of the total income that needs to be replaced. You can also use the Standard-of-Living Method, which involves multiplying your annual income by 20 if you are between 41-50 years old, or by 15 if you are between 51-60 years old.

Yes, there are life insurance calculators available on websites such as NerdWallet, Forbes, and Bankrate. These calculators will ask you to input information such as your annual income, the number of years you want to replace your income, your debts, future expenses, and your current assets. The calculator will then provide you with an estimate of the amount of life insurance coverage you need.