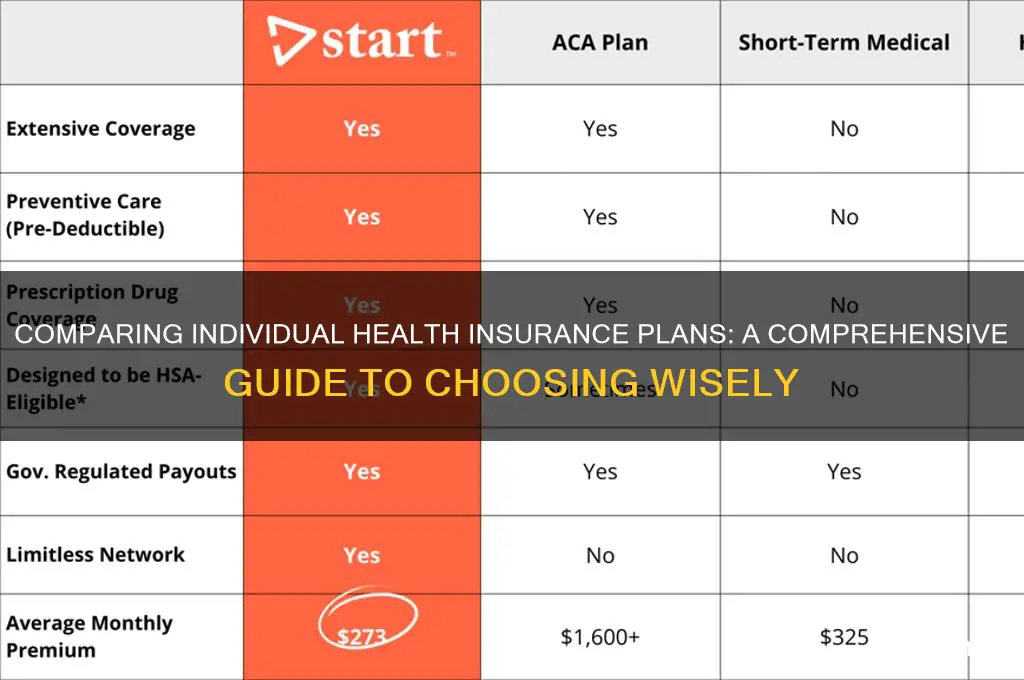

Comparing individual health insurance plans is a crucial step in ensuring you find the best coverage to meet your specific healthcare needs and budget. With numerous options available, it’s essential to evaluate factors such as premiums, deductibles, out-of-pocket maximums, and network coverage to determine which plan offers the most value. Additionally, consider the types of services covered, including preventive care, prescription drugs, and specialist visits, as these can vary significantly between plans. Understanding your own health requirements and financial situation will help you prioritize features that matter most, whether it’s lower monthly costs or comprehensive benefits. By carefully reviewing plan details, reading customer reviews, and using comparison tools, you can make an informed decision that provides peace of mind and financial protection.

Explore related products

What You'll Learn

- Coverage Limits: Compare maximum payouts, exclusions, and coverage for hospitalization, treatments, and pre-existing conditions

- Premium Costs: Evaluate monthly premiums, deductibles, and out-of-pocket expenses for different plans

- Network Providers: Check in-network hospitals, doctors, and specialists included in each insurance plan

- Policy Benefits: Compare additional benefits like maternity care, mental health, and wellness programs

- Claim Process: Review ease of filing claims, settlement ratios, and customer service efficiency

![]()

Coverage Limits: Compare maximum payouts, exclusions, and coverage for hospitalization, treatments, and pre-existing conditions

Understanding coverage limits is crucial when comparing individual health insurance plans. Maximum payouts, often referred to as policy limits, dictate the highest amount an insurer will pay for covered services. For instance, one plan might cap hospitalization expenses at $500,000 annually, while another offers unlimited coverage. This disparity can significantly impact out-of-pocket costs if you require extensive medical care. Always scrutinize these limits, especially if you have a high-risk lifestyle or chronic conditions that may necessitate costly treatments.

Exclusions are another critical aspect to examine. These are specific services or conditions not covered by the policy, such as cosmetic surgery, fertility treatments, or certain pre-existing conditions. For example, a plan might exclude coverage for diabetes management if diagnosed before the policy start date. To avoid surprises, create a list of your current and anticipated healthcare needs, then cross-reference it with each plan’s exclusion list. If you’re unsure about a term, contact the insurer directly for clarification—ambiguity can lead to unexpected expenses.

Hospitalization coverage varies widely across plans, often with sub-limits for room rent, ICU stays, and surgical procedures. Some policies cover only up to a certain percentage of the total bill, while others offer full coverage but with a co-pay clause. For instance, a plan might cover 100% of ICU charges but limit room rent to 1% of the sum insured per day. If you’re in an age group (e.g., over 50) or profession with higher hospitalization risks, prioritize plans with comprehensive inpatient coverage and minimal co-pays.

Treatment coverage is equally important, particularly for specialized therapies like chemotherapy, dialysis, or mental health services. Some plans impose waiting periods (e.g., 2–4 years) before covering pre-existing conditions, while others offer immediate coverage at a higher premium. For example, if you have hypertension, compare how each plan handles medication costs, doctor consultations, and complications like stroke. Look for policies that align with your specific treatment needs, ensuring they cover both preventive care and emergency interventions.

Finally, pre-existing conditions require careful consideration. Insurers often define these broadly, including ailments like asthma, thyroid disorders, or even past injuries. Some plans permanently exclude these conditions, while others offer coverage after a waiting period or at an additional cost. If you have a pre-existing condition, opt for a plan with shorter waiting periods or consider a critical illness rider for added protection. Remember, transparency about your health history is essential—withholding information can lead to claim rejections later.

By meticulously comparing maximum payouts, exclusions, hospitalization benefits, treatment coverage, and pre-existing condition policies, you can select a plan that offers both financial security and peace of mind. Use online comparison tools, consult insurance advisors, and read policy documents thoroughly to make an informed decision tailored to your health profile.

Homeowners Insurance Without Credit Checks: Top Companies to Consider

You may want to see also

Explore related products

![]()

Premium Costs: Evaluate monthly premiums, deductibles, and out-of-pocket expenses for different plans

Monthly premiums are the most visible cost of health insurance, but they’re only part of the financial equation. A plan with a lower premium might seem like a bargain until you factor in deductibles and out-of-pocket expenses. For instance, a 35-year-old individual might pay $250 monthly for a plan with a $1,500 deductible, while another plan at $350 monthly could have a $500 deductible. The higher-premium plan could save money if you anticipate frequent doctor visits or prescriptions, as you’d meet the deductible faster and reduce overall costs. Always calculate your expected annual healthcare usage against these costs to determine the better value.

Deductibles are a critical pivot point in health insurance plans. A high-deductible plan (e.g., $4,000 for an individual) often pairs with lower premiums but requires paying more out-of-pocket before coverage kicks in. These plans are ideal for healthy individuals who rarely need medical care beyond preventive services, which are typically covered at 100% even before the deductible is met. Conversely, a low-deductible plan (e.g., $1,000) suits those with chronic conditions or families expecting significant medical expenses, as it minimizes upfront costs for frequent care.

Out-of-pocket maximums cap your financial liability in a worst-case scenario, but they vary widely between plans. For example, a plan with a $6,000 out-of-pocket max might have lower premiums but expose you to higher risk if you require hospitalization. A plan with a $3,500 max offers more protection but at a steeper monthly cost. For a 50-year-old with a history of health issues, the higher premium might be justified to limit financial strain during emergencies. Always compare this limit alongside premiums and deductibles to balance affordability and risk.

To evaluate premium costs effectively, simulate your healthcare spending for the year. List expected expenses like medications, specialist visits, or ongoing treatments. For instance, if you take a $200 monthly prescription, factor in how quickly you’d meet deductibles under different plans. Use online calculators or consult an insurance broker to model scenarios. A practical tip: if your annual medical costs are predictable (e.g., $3,000 for a chronic condition), prioritize plans where the premium plus deductible stays below that amount. This approach ensures you’re not overpaying for coverage you won’t fully utilize.

Finally, don’t overlook hidden costs tied to premiums and deductibles. Some plans with low premiums restrict access to specific providers or require higher copays for specialist visits. For example, a $200 premium plan might charge $75 per specialist visit, while a $300 premium plan offers $30 copays. Similarly, generic drug coverage can vary—one plan might cover 80% after deductible, while another covers 100% from day one. Scrutinize the Summary of Benefits and Coverage (SBC) document for each plan to uncover these nuances and make an informed decision.

Does UCLA Medical Accept Medicare Insurance?

You may want to see also

Explore related products

![]()

Network Providers: Check in-network hospitals, doctors, and specialists included in each insurance plan

One of the most critical yet overlooked aspects of comparing individual health insurance plans is the network of providers. A plan’s network—the list of hospitals, doctors, and specialists it covers—directly impacts your access to care and out-of-pocket costs. For instance, visiting an in-network provider typically results in lower copays and coinsurance compared to out-of-network services, which may not be covered at all. Before enrolling, verify if your preferred healthcare providers are included in the plan’s network. Most insurers offer online tools where you can search for specific doctors or facilities by name, specialty, or location. If you have a trusted physician or require specialized care, this step is non-negotiable.

Consider a scenario where you’re managing a chronic condition like diabetes. Your endocrinologist, primary care physician, and local lab must all be in-network to avoid unexpected bills. Similarly, if you’re planning a family, ensure obstetricians and pediatricians are covered. Plans with narrow networks often have lower premiums but limit your choices, while broader networks offer flexibility at a higher cost. For example, an HMO (Health Maintenance Organization) typically requires referrals and has a smaller network, whereas a PPO (Preferred Provider Organization) allows out-of-network care but at a steeper price. Understanding these trade-offs is essential for aligning your plan with your healthcare needs.

To effectively compare networks, start by listing all providers you currently see or anticipate needing. Include specialists, therapists, and even pharmacies, as some plans have preferred pharmacy networks for prescription coverage. Next, cross-reference this list with each plan’s provider directory. Pay attention to details like whether the provider is accepting new patients and if the plan covers telehealth services, which can expand your access to care. For instance, a plan with a robust telehealth network might be ideal if you live in a rural area or have mobility challenges.

A common pitfall is assuming that a provider’s participation in one plan means they’re in all plans offered by the same insurer. Networks can vary significantly even within the same company, depending on the plan type and tier. For example, a Bronze-level plan might have a narrower network than a Gold-level plan from the same insurer. Always confirm by checking the specific plan’s directory, not just the insurer’s general network. Additionally, if you’re transitioning from employer-sponsored insurance, don’t assume your current providers will be covered under an individual plan.

Finally, consider the geographic reach of the network, especially if you travel frequently or split time between locations. Some plans offer national networks, while others are regional or local. If you’re a snowbird spending winters in Florida and summers in New York, ensure your plan covers providers in both states. Similarly, if you have children attending college out of state, verify if their campus health services are in-network or if the plan includes urgent care centers nationwide. By meticulously evaluating network providers, you can avoid costly surprises and ensure seamless access to the care you need.

Travel Medical Insurance: Applying for Coverage

You may want to see also

Explore related products

$7 $19.95

![]()

Policy Benefits: Compare additional benefits like maternity care, mental health, and wellness programs

Maternity care, mental health coverage, and wellness programs are not just add-ons—they’re critical differentiators when comparing individual health insurance policies. For instance, maternity care often includes prenatal visits, delivery costs, and postpartum care, but the extent of coverage varies widely. Some plans cap the number of prenatal visits to 12 per pregnancy, while others offer unlimited access. If you’re planning a family, scrutinize whether the policy covers complications like preeclampsia or neonatal intensive care unit (NICU) stays, as these can incur significant out-of-pocket costs.

Mental health coverage is another area where policies diverge sharply. Federal law mandates parity between mental and physical health benefits, but the devil is in the details. Check if the plan covers telehealth therapy sessions, which can be a lifeline for those in rural areas or with busy schedules. Also, verify the frequency of covered visits—some plans limit therapy to 20 sessions per year, while others align with your provider’s recommendation. For medication management, ensure the formulary includes your prescribed drugs, as exclusions can force you into costly alternatives.

Wellness programs are increasingly popular but vary in scope and utility. Some insurers offer gym memberships or fitness trackers, while others provide cash incentives for completing health challenges. For example, a plan might reward you with $100 for logging 10,000 steps daily for 30 days. However, evaluate whether these perks align with your lifestyle. If you’re not a gym-goer, a discounted membership is worthless. Instead, look for programs offering nutrition counseling, smoking cessation support, or stress management workshops, which provide tangible health benefits.

When comparing these benefits, consider your life stage and priorities. A 25-year-old single professional might prioritize mental health coverage and wellness incentives over maternity care, while a 35-year-old couple may focus on comprehensive maternity and fertility treatments. Use online comparison tools to filter plans by these specific benefits, but don’t rely solely on summaries—read the policy documents or consult an agent to clarify exclusions and limitations.

Finally, weigh the cost against the value. A plan with robust additional benefits may have higher premiums but could save you money in the long run. For example, a policy with comprehensive mental health coverage might prevent costly emergency room visits for untreated anxiety or depression. Conversely, if you rarely use wellness programs, opting for a lower-premium plan with basic coverage might be more cost-effective. The key is aligning the policy’s benefits with your current and anticipated health needs.

Pre-Tax vs. After-Tax Health Insurance: Which Saves You More?

You may want to see also

Explore related products

![]()

Claim Process: Review ease of filing claims, settlement ratios, and customer service efficiency

Filing a health insurance claim should be straightforward, but the reality often involves navigating complex paperwork, unclear guidelines, and frustrating delays. When comparing individual health insurance plans, scrutinize the claim process as if you’re already in a hospital bed—because that’s when it truly matters. Look for insurers that offer digital claim filing via apps or portals, as these reduce errors and speed up processing. For instance, some companies allow policyholders to upload medical bills and receipts directly, eliminating the need for physical documentation. However, don’t assume all digital systems are created equal; check user reviews to ensure the platform is intuitive and reliable.

Settlement ratios are the unsung heroes of health insurance comparisons. This metric, often overlooked, reveals the percentage of claims an insurer settles against the total received. A high settlement ratio (above 90%) indicates a company’s willingness to honor claims, while a low one suggests frequent rejections or disputes. For example, if Insurer A has a 95% settlement ratio and Insurer B has 78%, the former is statistically more likely to pay out when you need it. Cross-reference these ratios with customer reviews to identify patterns—do denied claims stem from policyholder errors, or is the insurer overly stringent?

Customer service efficiency during the claim process can make or break your experience. Imagine calling for assistance post-surgery, only to be met with long hold times or uninformed representatives. Test insurers’ responsiveness by calling their claim support line with hypothetical scenarios. Note how quickly they answer, the clarity of their guidance, and whether they follow up. Some companies offer dedicated claim managers, a boon for complex cases. Additionally, 24/7 support isn’t just a perk—it’s essential, as medical emergencies don’t adhere to business hours.

Finally, don’t overlook the fine print in claim policies. Some insurers impose sub-limits on specific treatments (e.g., ₹50,000 for cataract surgery) or require pre-authorization for hospital admissions. Others may exclude certain pre-existing conditions for the first 2–4 years. These details can derail a claim, even if the process itself is seamless. Pro tip: Use comparison tools that highlight such exclusions, and if in doubt, ask the insurer directly for clarification. A transparent claim policy is as valuable as a high settlement ratio.

Malpractice Insurance: Protecting Doctors, Saving Patients

You may want to see also

Frequently asked questions

Key factors include monthly premiums, deductibles, out-of-pocket maximums, network coverage (in-network vs. out-of-network providers), prescription drug coverage, and additional benefits like mental health or maternity care.

Check if your preferred doctors, hospitals, and specialists are in the plan’s network. Plans with narrower networks often have lower premiums but limit provider choices, while broader networks offer more flexibility but may cost more.

HMO (Health Maintenance Organization) plans typically require you to choose a primary care physician and get referrals for specialists, with lower premiums and out-of-pocket costs. PPO (Preferred Provider Organization) plans offer more flexibility to see any provider without a referral but usually have higher costs.

Calculate your expected yearly medical expenses, including doctor visits, prescriptions, and procedures. Compare this to the plan’s deductible, copays, and coinsurance to estimate total costs. Tools like online calculators or insurance brokers can help with this analysis.