Comparing spouse health insurance plans is a crucial step in ensuring both partners have adequate coverage while maximizing cost-effectiveness. Start by evaluating each plan’s premiums, deductibles, and out-of-pocket maximums to understand the financial commitment. Assess the network of providers to ensure access to preferred doctors and specialists for both individuals. Review coverage for essential services such as preventive care, prescriptions, and maternity care, as needs may differ between spouses. Consider whether a joint plan or individual policies offer better value based on age, health status, and employer contributions. Finally, compare additional benefits like mental health services, telehealth options, and wellness programs to align with both partners’ health priorities. Taking these factors into account will help make an informed decision that balances coverage, cost, and convenience for both spouses.

Explore related products

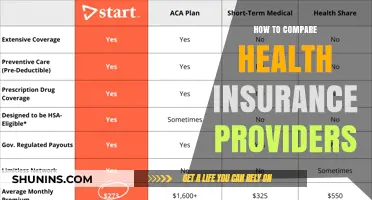

What You'll Learn

- Coverage Limits: Compare individual vs. family coverage limits for medical, dental, and vision care

- Premiums & Deductibles: Evaluate monthly premiums, annual deductibles, and out-of-pocket maximums for each plan

- Network Providers: Check if preferred doctors, hospitals, and specialists are in-network for both plans

- Prescription Benefits: Compare copays, formularies, and coverage for essential medications under each policy

- Additional Benefits: Assess extras like mental health, maternity care, or wellness programs offered by each plan

![]()

Coverage Limits: Compare individual vs. family coverage limits for medical, dental, and vision care

Health insurance plans often cap the amount they’ll pay for medical, dental, and vision care, and these limits can vary dramatically between individual and family policies. For instance, an individual plan might cover up to $1 million per year for medical expenses, while a family plan could cap at $3 million—but that total is shared among all members. If one spouse requires extensive treatment, the family limit could be exhausted quickly, leaving the other spouse or children underinsured. Always check the annual and lifetime maximums for each category of care to avoid unexpected out-of-pocket costs.

Dental and vision coverage limits are particularly important to scrutinize, as they are often lower and more restrictive than medical limits. An individual dental plan might cover up to $1,500 annually for preventive and basic services, while a family plan could cap at $3,000. However, if both spouses need orthodontic work—which can cost $5,000 or more per person—the family limit would fall short. Similarly, vision plans may limit coverage to one pair of glasses or contacts per year per person, but a family plan might not allow members to pool these benefits. For example, if one spouse needs progressive lenses ($300+) and the other prefers contacts ($200+), the combined cost could exceed the individual allowance, even under a family plan.

When comparing coverage limits, consider the health needs and history of both spouses. If one spouse has a chronic condition requiring frequent medical care, a family plan with higher limits might be more cost-effective, despite higher premiums. However, if both spouses are generally healthy and rarely use dental or vision services, individual plans with lower limits could save money. Use a spreadsheet to tally estimated annual expenses for each category of care, then compare these totals against the limits of both individual and family plans. Tools like Healthcare.gov’s plan comparison feature can help visualize these differences.

A practical tip: Look for plans that offer separate limits for each family member, even within a family policy. Some insurers provide individual sub-limits for dental and vision care, ensuring that one spouse’s high-cost needs don’t deplete the entire family’s coverage. For example, a family plan might allocate $2,000 per person for dental care, rather than a shared $4,000 limit. This structure provides more predictable protection and reduces the risk of one spouse’s expenses affecting the other’s coverage.

Finally, don’t overlook the role of deductibles and out-of-pocket maximums in relation to coverage limits. A family plan with a $10,000 out-of-pocket maximum might seem generous, but if the coverage limit for medical care is only $3 million, catastrophic expenses could still leave you financially vulnerable. Pairing a high-deductible health plan (HDHP) with a health savings account (HSA) can offset some costs, but ensure the coverage limits align with both spouses’ needs. For instance, an HDHP with a $7,000 family deductible might work if both spouses are healthy, but could be risky if one has ongoing medical needs. Always balance the trade-off between premiums, deductibles, and coverage limits to find the best fit for your household.

Medicaid vs Insurance: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Premiums & Deductibles: Evaluate monthly premiums, annual deductibles, and out-of-pocket maximums for each plan

Monthly premiums are the recurring cost of your health insurance, but they’re only part of the financial equation. A plan with a lower premium might seem appealing, but it often comes with higher deductibles or out-of-pocket costs. For example, a plan with a $200 monthly premium and a $3,000 deductible could end up costing more than a $300 premium plan with a $1,000 deductible if you anticipate frequent medical needs. Analyze your spouse’s health history and expected healthcare usage to determine which premium-deductible balance aligns best with your budget and needs.

Deductibles represent the amount you must pay out of pocket before insurance coverage kicks in. High-deductible plans (e.g., $5,000 or more) typically pair with lower premiums but require significant upfront spending. If your spouse rarely visits the doctor, this might be cost-effective. However, for chronic conditions or frequent care, a lower deductible (e.g., $1,000–$2,000) could save money long-term, even with higher monthly premiums. Compare deductibles across plans, considering how much you can afford to pay before coverage begins.

Out-of-pocket maximums cap your total annual expenses for covered services, offering financial protection. A plan with a $6,000 out-of-pocket maximum limits your liability, regardless of medical costs. When comparing spouse plans, prioritize this figure if there’s a risk of major medical events. For instance, a plan with a $400 premium, $2,500 deductible, and $7,000 out-of-pocket maximum might be riskier than a $500 premium plan with a $3,000 deductible and $5,500 maximum, especially for older adults or those with pre-existing conditions.

To evaluate these factors effectively, create a cost-scenario spreadsheet. Input monthly premiums, deductibles, and out-of-pocket maximums for each plan. Simulate low, medium, and high healthcare usage (e.g., 1 annual checkup vs. multiple specialist visits vs. hospitalization). For instance, if your spouse needs regular prescriptions, calculate how quickly they’d reach the deductible and how copays factor in. This approach reveals the true cost of each plan under different circumstances, ensuring you choose the most financially sound option.

Finally, don’t overlook hidden costs tied to deductibles and premiums. Some plans exclude certain services (e.g., physical therapy) from the deductible, meaning you pay full price until the out-of-pocket maximum. Others may have tiered deductibles for individuals vs. families. For spouses, ensure both parties’ needs are covered without duplicating costs. For example, if one spouse has employer-sponsored insurance, compare the cost of adding the other as a dependent versus purchasing a separate plan, factoring in premiums, deductibles, and maximums for both scenarios.

Choosing the Right Health Insurance for a Healthy Pregnancy Journey

You may want to see also

Explore related products

![]()

Network Providers: Check if preferred doctors, hospitals, and specialists are in-network for both plans

One of the most critical yet overlooked aspects of comparing spouse health insurance plans is verifying network providers. Simply put, an in-network doctor or hospital can save you hundreds, if not thousands, of dollars annually. Out-of-network services often come with higher out-of-pocket costs, surprise bills, and limited coverage. For instance, a routine specialist visit might cost $150 in-network but soar to $400 out-of-network. Start by listing all preferred healthcare providers—primary care physicians, OB/GYNs, pediatricians, and specialists—then cross-reference them against both plans’ provider directories. Many insurers offer online tools or customer service hotlines to streamline this process.

Consider a scenario where one spouse relies on a specific endocrinologist for diabetes management. If this specialist is only in-network for Plan A, switching to Plan B could disrupt care continuity and increase costs. Similarly, hospitals matter—especially for families planning pregnancy or managing chronic conditions. For example, if your preferred maternity hospital is in-network for one plan but not the other, factor in potential out-of-network costs like facility fees, which can range from $5,000 to $15,000 for an uncomplicated vaginal delivery. Use this analysis to weigh the financial and logistical implications of staying with preferred providers versus switching plans.

Persuasively, prioritizing in-network providers isn’t just about cost—it’s about preserving choice and quality. Out-of-network care often requires prior authorization, higher deductibles, and coinsurance rates that can reach 50% or more. For couples with ongoing treatments, such as physical therapy or mental health counseling, staying in-network ensures predictable expenses and uninterrupted care. Proactively, call providers to confirm their participation in both plans, as directories can be outdated. Additionally, ask about tiered networks, where certain providers within a network may still incur higher costs due to their designation as "elite" or "premium."

Comparatively, some plans offer out-of-network benefits, but these typically come with caveats. For example, a PPO might cover 60% of out-of-network costs after a separate, higher deductible is met, while an HMO may offer no out-of-network coverage at all except in emergencies. If both spouses have strong ties to specific providers, consider a PPO despite higher premiums, as it provides flexibility. Conversely, if you’re open to switching providers, an HMO or EPO with robust in-network options could save money. The key is aligning network coverage with your family’s healthcare habits and priorities.

Descriptively, imagine a couple where one spouse sees a therapist weekly and the other requires frequent orthopedic visits. If the therapist is in-network for Plan X but the orthopedist isn’t, and vice versa for Plan Y, they face a dilemma. Here, a practical tip is to calculate the annual cost difference between staying in-network versus going out-of-network for each provider. For instance, if the therapist charges $120 per session out-of-network and the orthopedist $300 per visit, compare these costs against the plans’ premiums and out-of-pocket maximums. This granular approach ensures you’re not just comparing plans but optimizing them for your unique needs.

Rising Health Insurance Costs: What’s Driving the Increase in 2023?

You may want to see also

Explore related products

![]()

Prescription Benefits: Compare copays, formularies, and coverage for essential medications under each policy

Prescription medications can account for a significant portion of healthcare costs, especially for chronic conditions like hypertension, diabetes, or asthma. When comparing spouse health insurance plans, scrutinize the prescription benefits to ensure essential medications are covered without breaking the bank. Start by listing all medications each spouse takes regularly, including dosage and frequency. For example, if one spouse requires 20mg of atorvastatin daily for cholesterol management, check how each plan categorizes this drug—as generic, preferred brand, non-preferred brand, or specialty. This classification directly impacts the copay amount, which can range from $10 for generics to $75 or more for non-preferred brands.

Next, examine the formulary—the list of drugs covered by each plan. Not all medications are included in every formulary, and some plans may require prior authorization or step therapy (trying a lower-cost drug first). For instance, if a spouse relies on a specific insulin brand like Lantus, verify if it’s covered and under which tier. If it’s excluded, calculate the out-of-pocket cost for purchasing it without insurance coverage. Additionally, check if the plan offers mail-order pharmacy options, which often provide 90-day supplies at a lower copay than retail pharmacies. For example, a 90-day supply of metformin might cost $20 via mail order versus $10 per 30-day refill at a local pharmacy.

Coverage gaps during the deductible phase can also affect prescription costs. Some plans cover medications at a reduced rate even before the deductible is met, while others require full payment until the deductible is reached. For high-cost medications like Humira (used for rheumatoid arthritis), this difference can mean paying $500 per month versus $4,000 until the deductible is satisfied. Use each plan’s cost estimator tool to model these scenarios based on your medication list and anticipated healthcare usage for the year.

Finally, consider the plan’s pharmacy network. Some insurers partner with specific pharmacy chains, and using an out-of-network pharmacy can result in higher costs or no coverage at all. For example, if one spouse prefers CVS and the other uses Walgreens, ensure both pharmacies are in-network for the chosen plan. If not, weigh the convenience of staying with a preferred pharmacy against the potential savings of switching to an in-network option.

In summary, comparing prescription benefits requires a detailed analysis of copays, formularies, coverage policies, and pharmacy networks. By focusing on these elements, you can select a plan that minimizes out-of-pocket costs for essential medications while maximizing convenience and accessibility for both spouses.

Staying Healthy: Choosing the Right Health Insurance

You may want to see also

![]()

Additional Benefits: Assess extras like mental health, maternity care, or wellness programs offered by each plan

Mental health coverage varies wildly across plans, and overlooking this can leave you vulnerable during a crisis. For instance, some policies limit therapy sessions to 10 per year, while others offer unlimited visits with a copay as low as $20. Look for plans that cover evidence-based treatments like cognitive behavioral therapy (CBT) and include access to psychiatrists for medication management. If your spouse has a history of mental health concerns or works in a high-stress field, prioritize plans with robust mental health benefits. Pro tip: Check if the plan covers telehealth services for mental health, as this can provide flexibility and immediate support.

Maternity care is another critical area where plans differ significantly, especially in terms of pre- and postnatal services. Some plans cover only the delivery, while others include prenatal vitamins, breastfeeding support, and postpartum mental health screenings. For example, a plan might offer a $500 stipend for breastfeeding supplies or cover up to six postpartum therapy sessions. If you’re planning to expand your family, compare the out-of-pocket costs for maternity care, including deductibles and coinsurance rates. A plan with a higher monthly premium might save you thousands in the long run if it offers comprehensive maternity benefits.

Wellness programs are often overlooked but can add significant value to a health insurance plan. These programs may include gym memberships, smoking cessation aids, or discounts on healthy groceries. For instance, some plans reimburse up to $200 annually for fitness-related expenses, while others provide free access to apps like Headspace or MyFitnessPal. If your spouse is focused on preventive care or has chronic conditions like diabetes, a plan with robust wellness incentives can encourage healthier habits and reduce long-term healthcare costs.

When comparing these additional benefits, don’t just skim the summaries—dive into the details. For example, a plan might claim to cover “mental health services” but exclude treatment for eating disorders or substance abuse. Similarly, a wellness program might offer gym discounts but only at specific chains, limiting accessibility. Use the plan’s Summary of Benefits and Coverage (SBC) document to compare specifics side by side. This ensures you’re not just choosing a plan with flashy extras but one that genuinely aligns with your spouse’s health needs and lifestyle.

Pet Medical Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Key factors include coverage scope (e.g., doctor visits, prescriptions, maternity care), out-of-pocket costs (deductibles, copays), provider networks, and whether both spouses’ preferred doctors are in-network. Also, compare premiums and whether the plan covers pre-existing conditions.

A family plan often costs less than two individual plans and simplifies billing. However, compare the total cost and coverage of both options. If one spouse has access to employer-subsidized insurance, individual plans might be more cost-effective.

Look for plans with comprehensive coverage for pre-existing conditions and no exclusions. Compare the cost of medications, specialist visits, and treatments. Plans with lower out-of-pocket maximums are often better for chronic conditions.

Ensure both spouses’ preferred doctors, specialists, and hospitals are in-network to avoid higher out-of-network costs. Compare network sizes and check if the plan offers out-of-network coverage, though it’s usually more expensive.