Navigating the complex landscape of private health insurance can be a daunting task, especially with the myriad of options available. This guide aims to demystify the process, providing you with the essential steps and considerations to find a plan that best suits your needs and budget. From understanding your coverage requirements to comparing different providers and policies, we'll walk you through the key aspects to consider. Whether you're new to private health insurance or looking to switch plans, this comprehensive overview will empower you to make informed decisions about your healthcare coverage.

| Characteristics | Values |

|---|---|

| Target Audience | Individuals or families seeking private health insurance |

| Purpose | To guide the process of selecting and purchasing private health insurance |

| Content Type | Informational guide or article |

| Format | Online resource, PDF document, or printed brochure |

| Language | English |

| Length | Approximately 2,000-3,000 words |

| Topics Covered | Types of private health insurance, coverage options, cost factors, provider networks, enrollment process, FAQs |

| Visual Elements | Infographics, charts, or illustrations explaining insurance concepts |

| Style | Clear, concise, and easy to understand |

| Tone | Neutral and informative |

| Call to Action | Encourage readers to compare quotes, consult with an insurance agent, or enroll in a plan |

| Author | Insurance expert, healthcare professional, or content writer |

| Publisher | Insurance company, healthcare provider, or independent website |

| Date of Publication | June 2024 |

| Update Frequency | Annually or as needed to reflect changes in insurance options and regulations |

| Keywords | Private health insurance, coverage, costs, providers, enrollment |

| Meta Description | A comprehensive guide on how to look for private health insurance, including tips on comparing plans and understanding coverage options |

Explore related products

What You'll Learn

- Assess Your Needs: Identify your healthcare requirements, such as prescription coverage, dental, and vision care

- Research Providers: Compare different insurance companies and their plans, looking at provider networks and customer reviews

- Understand Costs: Evaluate premiums, deductibles, copays, and coinsurance to determine the total cost of each plan

- Check Eligibility: Ensure you meet the eligibility criteria for the plans you're considering, such as age and health status

- Seek Professional Advice: Consult with an insurance broker or healthcare advisor to get personalized recommendations based on your needs

![]()

Assess Your Needs: Identify your healthcare requirements, such as prescription coverage, dental, and vision care

To effectively assess your healthcare needs, begin by reviewing your medical history and current health status. This involves considering any chronic conditions, medications you're currently taking, and any anticipated health changes, such as pregnancy or upcoming surgeries. Evaluate the frequency and type of medical services you typically use, including doctor visits, lab tests, and hospitalizations. This self-assessment will help you determine the level of coverage you require.

Next, consider your prescription needs. If you take multiple medications, look for plans that offer comprehensive prescription coverage. Pay attention to the formulary, which is the list of drugs covered by the insurance plan, and ensure your medications are included. Also, check the out-of-pocket costs for prescriptions, as these can vary significantly between plans.

Dental and vision care are often overlooked but are crucial components of overall health. If you have a family history of dental issues or wear glasses or contacts, prioritize plans that include robust dental and vision coverage. Look for plans that cover routine check-ups, cleanings, and major procedures like root canals or LASIK surgery.

Additionally, consider any specialized care you may need. For example, if you have a chronic illness like diabetes or heart disease, you may require more frequent doctor visits and specialized treatments. Ensure the plan you choose covers these specific needs.

Finally, think about your budget and how much you can afford to pay in premiums, deductibles, and co-pays. While it's essential to have adequate coverage, you also need to ensure the plan is financially sustainable for you. Compare the costs of different plans and consider the long-term financial impact of each option.

By carefully assessing your healthcare needs and considering the specifics of prescription, dental, and vision coverage, as well as any specialized care requirements and your budget, you can make an informed decision when selecting a private health insurance plan.

Understanding Health Insurance Responsibilities for Non-Custodial Parents in California

You may want to see also

Explore related products

![]()

Research Providers: Compare different insurance companies and their plans, looking at provider networks and customer reviews

To effectively research providers and compare different insurance companies and their plans, it's crucial to start by gathering a list of potential insurers. This can be done through online searches, recommendations from friends and family, or by consulting with a licensed insurance agent. Once you have a list of companies, visit their websites to obtain detailed information about their plans, including coverage options, premiums, deductibles, and out-of-pocket costs.

Next, focus on provider networks. Insurance companies often have networks of preferred providers, which can include doctors, hospitals, and specialists. These networks can vary significantly between companies, so it's important to ensure that the providers you prefer or require are included in the network of the insurance company you're considering. You can typically find this information on the insurer's website or by contacting their customer service department.

Customer reviews are another valuable resource when comparing insurance companies. Look for reviews on independent websites, such as Yelp or Healthgrades, as well as on the websites of the insurance companies themselves. Pay attention to both positive and negative reviews, and consider the overall trends in customer satisfaction. Keep in mind that individual experiences can vary, but consistent patterns in reviews can provide valuable insights into the quality of service and coverage provided by an insurer.

In addition to provider networks and customer reviews, consider the financial stability and reputation of the insurance companies you're comparing. Look for ratings from organizations such as A.M. Best, Moody's, or Standard & Poor's, which can provide information about an insurer's financial strength and ability to meet its obligations. You may also want to research any complaints filed against the companies with your state's insurance department or other regulatory bodies.

Finally, take the time to compare the specific benefits and features of each plan you're considering. This may include additional perks such as wellness programs, telemedicine services, or prescription drug coverage. By carefully evaluating all of these factors, you can make an informed decision about which insurance company and plan best meet your needs and budget.

Which Insurers Offer Medicare Part D Prescription Drug Plans?

You may want to see also

Explore related products

![]()

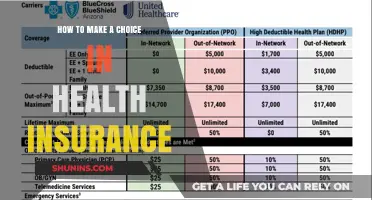

Understand Costs: Evaluate premiums, deductibles, copays, and coinsurance to determine the total cost of each plan

To truly grasp the financial implications of private health insurance, it's crucial to dissect the various components that contribute to the overall cost. Premiums, deductibles, copays, and coinsurance are key terms that often get thrown around, but understanding how they interact can make a significant difference in your decision-making process.

Let's start with premiums, which are the monthly payments you make to maintain your insurance coverage. While it might be tempting to opt for a plan with lower premiums, it's essential to consider the bigger picture. Plans with lower premiums often come with higher deductibles, which means you'll need to pay more out-of-pocket before your insurance kicks in. This can be a double-edged sword, especially if you anticipate needing frequent medical attention.

Deductibles are the amounts you must pay before your insurance begins to cover your medical expenses. A high deductible can be daunting, but it's not the only factor to consider. Plans with high deductibles often have lower premiums, which can be beneficial if you're generally healthy and don't expect to need extensive medical care. However, if you do require frequent medical attention, a high deductible can quickly add up, making it more expensive than a plan with a lower deductible and higher premiums.

Copays and coinsurance are additional costs that come into play once you've met your deductible. Copays are fixed amounts you pay for each medical service or prescription, while coinsurance is a percentage of the cost that you're responsible for. These costs can vary significantly between plans, so it's important to compare them carefully. A plan with lower copays might be more appealing if you need frequent medical care, while a plan with lower coinsurance might be more cost-effective if you anticipate needing expensive treatments or procedures.

To determine the total cost of each plan, you'll need to consider all of these factors together. Calculate the annual premium cost, the potential deductible amount, and the estimated copays and coinsurance based on your expected medical needs. This will give you a more comprehensive understanding of the true cost of each plan and help you make a more informed decision.

Remember, the goal is to find a balance between affordability and coverage that meets your specific needs. By carefully evaluating the costs associated with each plan, you can make a more confident choice and avoid unexpected financial burdens down the line.

The Risks of Living Without Health Insurance in the USA

You may want to see also

Explore related products

![]()

Check Eligibility: Ensure you meet the eligibility criteria for the plans you're considering, such as age and health status

Before diving into the specifics of checking eligibility for private health insurance plans, it's crucial to understand that eligibility criteria can vary significantly between providers and plans. Typically, factors such as age, health status, pre-existing conditions, and even lifestyle choices can influence whether you qualify for certain coverage options. For instance, some plans may have age limits, excluding applicants above a certain age, while others might require a medical examination to assess your health status.

To navigate this complex landscape, start by gathering detailed information about your personal health history. This includes any pre-existing conditions, medications you're currently taking, and any previous hospitalizations or surgeries. Being upfront about your health status is essential, as failing to disclose relevant information could lead to your application being denied or, worse, your coverage being revoked later on.

Next, research the specific eligibility requirements for each plan you're considering. This information is usually available on the provider's website or can be obtained by contacting their customer service directly. Pay close attention to any exclusions or limitations listed, as these can impact your coverage. For example, some plans may not cover certain pre-existing conditions for a specified period, known as a waiting period, while others might offer limited coverage for specific health issues.

It's also important to consider the impact of your lifestyle choices on your eligibility. Factors such as smoking status, alcohol consumption, and even your occupation can affect your premiums and coverage options. Some providers may offer discounts or special rates for non-smokers or individuals with certain professions that are deemed lower risk.

Finally, don't hesitate to seek professional advice if you're unsure about your eligibility or how to navigate the application process. Insurance brokers or financial advisors can provide valuable insights and help you find a plan that meets your specific needs and circumstances. Remember, the key to securing the right private health insurance coverage is to be well-informed and proactive in understanding and meeting the eligibility criteria.

Does Your Health Insurance Cover Weight Loss Surgery? Find Out Here

You may want to see also

Explore related products

![]()

Seek Professional Advice: Consult with an insurance broker or healthcare advisor to get personalized recommendations based on your needs

Navigating the complex landscape of private health insurance can be daunting, but seeking professional advice can make the process significantly smoother. Consulting with an insurance broker or healthcare advisor offers personalized recommendations tailored to your unique needs, ensuring you make informed decisions.

One of the primary benefits of professional consultation is the expertise these advisors bring to the table. They are well-versed in the intricacies of various insurance plans, including coverage options, premiums, deductibles, and co-pays. By understanding your specific healthcare requirements, they can help you identify plans that offer the best value for your money.

Moreover, insurance brokers and healthcare advisors often have access to a wide range of insurance providers, allowing them to compare policies and negotiate better terms on your behalf. This can result in cost savings and more comprehensive coverage than you might achieve by shopping around on your own.

Another advantage of seeking professional advice is the time-saving aspect. Instead of spending hours researching different plans and trying to decipher the fine print, you can rely on your advisor to do the legwork for you. They will present you with a curated selection of options that meet your criteria, streamlining the decision-making process.

Additionally, these professionals can provide valuable insights into the potential risks and benefits associated with each plan. They can help you understand the implications of choosing a high-deductible plan versus a low-deductible plan, for example, and how these choices might impact your out-of-pocket expenses.

In conclusion, seeking professional advice when looking for private health insurance is a smart strategy that can lead to better-informed decisions, cost savings, and more comprehensive coverage. By leveraging the expertise of insurance brokers or healthcare advisors, you can navigate the complexities of the insurance market with confidence and ease.

Decoding Health Insurance: Are Chips Covered?

You may want to see also

Frequently asked questions

When searching for private health insurance, consider factors such as the cost of premiums, the level of coverage provided, the types of healthcare services covered, the quality of customer service, and the reputation of the insurance provider. Additionally, think about your specific healthcare needs and whether the policy offers flexibility in choosing healthcare providers.

To compare different private health insurance plans, start by reviewing the policy summaries and comparing the benefits, exclusions, and limitations of each plan. Look at the premium costs, deductibles, co-payments, and out-of-pocket maximums. Consider the network of healthcare providers associated with each plan and whether your preferred doctors and hospitals are included. Reading customer reviews and checking the financial stability of the insurance companies can also help in making an informed decision.

HMO (Health Maintenance Organization) plans typically require you to choose a primary care physician and get referrals for specialist care. They often have lower premiums and out-of-pocket costs but offer less flexibility in choosing healthcare providers. PPO (Preferred Provider Organization) plans allow you to see any healthcare provider within the network without a referral, but you may pay more in premiums and out-of-pocket costs. EPO (Exclusive Provider Organization) plans are similar to HMO plans but do not require referrals for specialist care. They offer a balance between cost and flexibility.

Yes, you can get private health insurance if you have a pre-existing condition, but it may affect the cost of your premiums or the coverage you receive. Some insurance companies may exclude coverage for pre-existing conditions for a certain period, while others may charge higher premiums. It's important to disclose your pre-existing conditions when applying for insurance to ensure you get the appropriate coverage.

To enroll in a private health insurance plan, you can typically do so through the insurance company's website, by phone, or through an insurance broker. You will need to provide personal information, such as your name, address, and social security number, as well as details about your healthcare needs and preferences. Once you've selected a plan, you can complete the enrollment process by paying the first premium and signing the necessary documents.