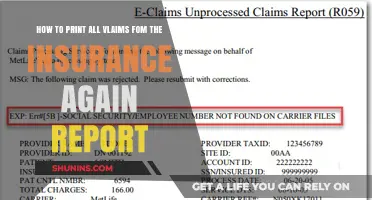

Reading an insurance summary report can be a daunting task, but it is important to understand the coverage provided by your insurance plan. Insurance summary reports provide a detailed overview of an individual's insurance policies, including personal and commercial lines. These reports can be generated for a quick summary of insurance details, such as the insured's name, policy type, premium amount, benefit amount, and coverage limitations. Understanding insurance terminology is crucial when interpreting these reports, as terms like premium and policy owner may have specific meanings in the insurance context. Life insurance policies, for example, differentiate between whole life and universal life insurance, each with unique characteristics. Health insurance plans, on the other hand, offer a Summary of Benefits and Coverage (SBC), which outlines cost-sharing structures and common medical events, helping consumers compare plans easily. By familiarizing yourself with the key sections and terms, you can confidently navigate your insurance summary report and make informed decisions about your coverage.

| Characteristics | Values |

|---|---|

| Purpose | To provide a summary of an insured person's policies and/or submissions |

| Format | Only available in landscape layout and can be exported in several formats |

| Content | Name of the insurance provider, type of policy, insured's name, name of the policy owner, premium amount, benefit amount, coverage limitations, list of riders, beneficiaries, and other vital components |

| Common Confusions | Death benefit and face amount reported as separate values, guaranteed cash value vs. paid-up additions cash value |

| Additional Information | Definitions of terms used in the policy, trial period/free-look period, policy loan, variable premiums, and common medical events |

Explore related products

What You'll Learn

- Understanding the structure: Know what to expect, from the summary to the fine print

- Definitions: Learn the meanings of key terms and jargon

- Insured, policyholder, and beneficiaries: Identify who is covered and their rights

- Premiums: Understand the costs and payment frequencies

- Exclusions and limitations: Know what the policy doesn't cover and any restrictions

![]()

Understanding the structure: Know what to expect, from the summary to the fine print

Understanding the structure of an insurance summary report is crucial for making informed decisions about your coverage. Here's what you can expect to find in such a report, from the summary to the fine print:

The Summary Section

The first page of an insurance summary report typically provides a concise overview of the policy's key details. This includes essential information such as the insurance provider's name, the type of policy, the name of the insured, and the policy owner's name. This section serves as a quick reference, giving you a snapshot of the coverage and its fundamental aspects.

Policy Details and Definitions

Beyond the initial summary, the report delves into the specifics of the insurance policy. This includes important elements such as the premium amount (the cost of the policy), the benefit amount or coverage limits, and any additional riders or add-ons that enhance the coverage. It is crucial to understand the terminology used in this section, as insurance policies often include technical terms with specific meanings within the industry.

Insured and Policyholder Information

The insurance summary report will provide detailed information about the insured individual or entity, as well as the policyholder if they are different. This includes personal or business information, such as names, ages, addresses, and other relevant details that define the scope of the coverage.

Coverage Limitations and Exclusions

This section outlines any limitations or restrictions on the insurance coverage. It specifies what is not covered by the policy, providing clarity on the circumstances under which the insurer will not provide benefits. Understanding exclusions is critical to managing expectations and ensuring you are adequately protected.

Beneficiaries and Rights

The report should also include information about beneficiaries, who are the individuals or entities entitled to receive benefits from the policy. Additionally, it should outline the rights of the policy owner, such as their ability to make changes, cancel the policy, or file claims.

Financial Details and Loan Information

For life insurance policies, the summary report will often include financial details, such as the current loan balance, loan interest, and information about policy loans or withdrawals. This section provides transparency on the monetary aspects of the policy, including any accrued cash value or dividends.

Fine Print and Additional Information

Lastly, the fine print of the insurance summary report may include various other details, such as the frequency of payments, trial periods or free-look periods, and information on how to compare plans or file complaints. This section typically contains important nuances that further define the scope and conditions of the coverage.

Remember, while this provides a general structure, the specific content and organization of an insurance summary report can vary depending on the type of insurance and the provider. Always take the time to carefully review the entire report and clarify any questions with a financial or insurance professional.

Speeding Tickets: Insurance Reporting and Its Impact

You may want to see also

Explore related products

![]()

Definitions: Learn the meanings of key terms and jargon

When it comes to insurance, there is a lot of jargon and technical language to get your head around. Many terms may seem like common words, but their definition in an insurance context differs from how you use a word in everyday conversation. So, it's a good idea to read through the definitions section of your insurance summary report to make sure you understand the essential terms used in the document.

For example, the term "premium" refers to the monthly or yearly payments needed to keep the insurance contract in effect. "Variable premiums" refer to premiums that will change over time, and these should be indicated in a chart. "Policy loan" is the value of a whole life or universal life policy that you can borrow against. "Affiliate" refers to a person or entity that has control over the insurer, or is controlled by the insurer, or is under common control with the insurer. "Agent" is an individual who sells, services, or negotiates insurance policies, either on behalf of a company or independently. "Aggregate" is the maximum dollar amount or total amount of coverage payable for a single loss, or multiple losses, during a policy period, or on a single project. "Accident insurance" is insurance for unforeseen bodily injury. "Accident only" is an insurance contract that provides coverage, singly or in combination, for death, dismemberment, disability, or hospital and medical care caused by or resulting from an accident. "Fair value" is the amount at which an asset or liability could be bought or sold in a current transaction between willing parties. "Farmowners insurance" is a package policy that includes both property and liability coverage for personal and business losses. "Identity theft coverage" pays for expenses as a direct result of identity theft or fraud during the policy period. "Insurable interest" must be present for an insurance contract to be legal and valid; a person with insurable interest will suffer a genuine hardship if a loss occurs to the person or property they've insured.

Bahamas: Home Insurance a Must?

You may want to see also

Explore related products

![]()

Insured, policyholder, and beneficiaries: Identify who is covered and their rights

When reading an insurance summary report, it is important to identify who is covered and their rights. This includes understanding the roles of the insured, policyholder, and beneficiaries.

The insured is the person or entity that is covered by the insurance policy. In the case of life insurance, the insured is the person whose life is insured, and in the event of their death, the beneficiaries would receive the benefits outlined in the policy. The insured is typically listed on the first page of the insurance contract, along with the insurance provider's name, the type of policy, and the name of the policy owner.

The policyholder is the person or organization in whose name the insurance policy is registered. They are the ones who have control over the policy and can make changes or additions to it. In some cases, the policyholder and the insured may be the same person, especially in the case of life insurance policies taken out by an individual for themselves. However, in other cases, such as employer-provided insurance, the employer may be the policyholder while the employee is the insured.

The beneficiary is the person or entity that receives the benefits or proceeds from the insurance policy. In the case of life insurance, the beneficiary is typically the spouse or children of the insured, but it can be any person designated as such in the policy. The beneficiary has the right to receive the indemnity calculated according to the claim and any damage caused. It is important to note that a single insurance policy can have multiple beneficiaries but only one policyholder.

Understanding these roles is crucial when reviewing an insurance summary report. It helps to clarify who is covered by the policy, who has the authority to make changes, and who will receive the benefits in the event of a claim. It is also important to note that the specific rights and responsibilities of each party may vary depending on the insurance provider and the specific terms of the policy. Therefore, it is always a good idea to carefully review the entire policy document and seek clarification from a financial professional if needed.

Home Insurance Calculation Factors

You may want to see also

Explore related products

![]()

Premiums: Understand the costs and payment frequencies

When it comes to insurance, premiums refer to the monthly or yearly payments required to maintain an active insurance policy. In the context of life insurance, premiums are necessary to keep the contract in effect. There are two types of permanent life insurance: whole life and universal life. Whole life insurance premiums remain constant throughout the policy's duration, and the cash value grows at a guaranteed rate. Conversely, universal life insurance premiums can vary, making the policy more complex and potentially less expensive.

It is essential to understand the payment frequency of your insurance premiums. The annual statement of a whole life insurance policy typically outlines the premiums associated with the policy, including the base whole life premium and any additional premiums, such as a term rider premium. The statement may or may not specify the exact amounts paid towards each premium and whether it includes elective paid-up additions. Paid-up additions refer to the additional payments made towards the policy, enhancing its overall value.

Variable premiums refer to premiums that fluctuate over time. Your insurance contract should include a chart or graph illustrating how these changes will occur. It is crucial to review this information carefully to anticipate future adjustments in your premium payments. Understanding the payment frequency and potential variability of your premiums ensures that you are well-informed about your financial commitments and enables you to plan your expenses effectively.

Additionally, it is worth noting that whole life insurance premiums offer tax-deferred benefits. The premiums you pay can accumulate tax-deferred cash value within the policy, which can be accessed later in life through loans or withdrawals. This feature provides added flexibility and financial security. However, it is important to remember that taking out loans or making withdrawals against the policy will likely reduce the death benefit and cash values guaranteed by the insurance company.

Death Benefits and Taxes: Do Insurance Payouts Get Taxed?

You may want to see also

Explore related products

![MINORITY REPORT [LIMITED EDITION STEELBOOK 4K UHD + BLU-RAY + DIGITAL]](https://m.media-amazon.com/images/I/71ei+mc9AuL._AC_UY218_.jpg)

![MINORITY REPORT [4K UHD + BLU-RAY + DIGITAL]](https://m.media-amazon.com/images/I/71OtfWmyQEL._AC_UY218_.jpg)

![]()

Exclusions and limitations: Know what the policy doesn't cover and any restrictions

When it comes to insurance, exclusions refer to specific conditions, treatments, or services that an insurer will not pay for, while limitations refer to the restrictions imposed by the insurance company on what they will cover. Understanding these aspects is crucial to avoid unexpected out-of-pocket expenses when seeking medical care or filing a claim.

Exclusions and limitations can vary depending on the type of insurance, such as health, life, property, or auto insurance, and they are often outlined in the insurance contract or policy document. It is important to carefully review these documents to identify any exclusions or limitations that may impact your coverage.

In health insurance, common exclusions include cosmetic procedures aimed at enhancing appearance rather than treating an illness. For example, surgeries such as facelifts or liposuction are typically not covered unless they are part of reconstructive surgery following an accident or for a congenital disability. Additionally, emerging therapies, off-label drug use, and certain advanced procedures may be excluded if they are not considered standard medical practice. It is also important to note that insurers may define "insured persons" in a way that limits coverage, such as excluding roommates or extended family members unless they are explicitly listed.

In life insurance, pre-existing medical conditions may be excluded or require a waiver for coverage. Property insurance may exclude certain types of damage, such as wind-related damage in hurricane-prone areas. Auto insurance may have limitations on the types of damage covered, and certain exclusions may apply, such as for unauthorised drivers or specific types of accidents.

Understanding the fine print and seeking clarification from insurance professionals can help individuals make informed decisions about their coverage and avoid unexpected expenses.

Farmers Insurance Subscription Agreement: Understanding the Fine Print

You may want to see also

Frequently asked questions

The Summary of Insurance Report allows you to create a summary of an insured individual's personal, commercial, and policy/submission information.

An SBC contains information about the coverage provided by a health insurance plan, the cost-sharing structure, and common medical events. It also includes a clarification page, which provides information about how costs are covered, excluded services, and other covered services.

Whole life insurance policies outline the insured and policyholder's information, the type of policy, the premium amount, the benefit amount, any coverage limitations, a list of riders, beneficiaries, and other vital components.

Whole life insurance premiums remain the same, the death benefit is guaranteed, and the cash value grows at a guaranteed rate. Universal life insurance premiums, death benefits, and cash account growth rates can vary, making the policy more complex.

Many insurance terms may seem like common words but have different meanings in an insurance context. It is important to refer to the definitions section of the report or a glossary of terms provided by the insurer to fully understand the content of the summary report.