Family health insurance is a crucial aspect of financial planning and healthcare management for many households. It provides a safety net against unexpected medical expenses, ensuring that all family members have access to necessary healthcare services without facing significant out-of-pocket costs. This type of insurance typically covers a range of medical services, including doctor visits, hospital stays, prescription medications, and preventive care. The value of family health insurance lies in its ability to protect the health and well-being of loved ones while also safeguarding the family's financial stability. However, determining whether family health insurance is worth it involves considering various factors such as the cost of premiums, the extent of coverage, and the overall health needs of the family members.

Explore related products

What You'll Learn

- Cost-Benefit Analysis: Evaluate the monthly premiums against the potential health care savings for your family

- Coverage Details: Understand what medical services and treatments are included and excluded from the insurance plan

- Network Providers: Check if your preferred doctors and hospitals are within the insurance network

- Deductibles and Co-Pays: Consider the out-of-pocket expenses you'll need to cover before insurance kicks in

- Peace of Mind: Reflect on the value of having financial protection against unexpected health issues for your loved ones

![]()

Cost-Benefit Analysis: Evaluate the monthly premiums against the potential health care savings for your family

To conduct a thorough cost-benefit analysis of family health insurance, begin by gathering detailed information on the monthly premiums associated with various plans. These premiums can vary widely depending on factors such as the insurance provider, the level of coverage, and the health status of the family members. Next, estimate the potential health care savings that could be realized with each plan. This involves considering the out-of-pocket costs for medical services, prescription medications, and other health-related expenses that would be covered by the insurance.

One approach to this analysis is to create a spreadsheet that lists the monthly premiums for each plan alongside the estimated annual savings. This allows for a clear visual comparison of the costs and benefits. Additionally, consider the potential risks and uncertainties associated with each plan, such as the possibility of rate increases or changes in coverage. It may be helpful to consult with an insurance professional to gain a better understanding of these factors and to identify any potential hidden costs or benefits.

When evaluating the potential health care savings, it is important to consider the specific health needs of the family members. For example, if a family member has a chronic condition that requires ongoing medical treatment, a plan with lower out-of-pocket costs for this treatment may be more beneficial, even if it has higher monthly premiums. Conversely, if the family members are generally healthy and do not anticipate significant medical expenses, a plan with lower monthly premiums may be more cost-effective.

Another important consideration is the potential for future changes in the family's health care needs. For example, if a family is planning to have children, they may want to consider a plan that provides comprehensive coverage for maternity and pediatric care. Similarly, if a family member is approaching retirement age, they may want to consider a plan that offers good coverage for age-related health issues.

Ultimately, the decision of whether or not family health insurance is worth it depends on a careful weighing of the costs and benefits. By conducting a thorough cost-benefit analysis and considering the specific health needs and circumstances of the family, individuals can make an informed decision that best meets their needs and budget.

Understanding AmBetter: Is It the Right Commercial Health Insurance for You?

You may want to see also

Explore related products

![]()

Coverage Details: Understand what medical services and treatments are included and excluded from the insurance plan

Understanding the coverage details of a family health insurance plan is crucial to determining its value. It's essential to know exactly what medical services and treatments are included and excluded from the plan to make an informed decision. This involves scrutinizing the policy documents to identify the specific procedures, medications, and healthcare providers that are covered. For instance, some plans may include comprehensive dental care, while others might only cover basic cleanings and exams. Similarly, certain medications may be fully covered, while others might require a copay or coinsurance.

One of the key aspects to consider is the inclusion of preventive care services. Preventive care, such as regular check-ups, vaccinations, and screenings, can significantly reduce the risk of developing chronic conditions and can lead to early detection and treatment of potential health issues. A plan that covers these services can provide substantial long-term benefits for a family's overall health and well-being.

Another important factor is the coverage for emergency services and hospitalizations. Emergencies can occur unexpectedly, and having a plan that covers ambulance rides, emergency room visits, and hospital stays can provide financial security during stressful times. It's also worth noting the plan's coverage for mental health services, as mental health is an integral part of overall health. Plans that include therapy sessions, counseling, and psychiatric care can be particularly beneficial for families.

When evaluating coverage details, it's also necessary to consider the exclusions. Some plans may exclude certain pre-existing conditions, alternative treatments, or experimental procedures. Understanding these exclusions can help families anticipate potential out-of-pocket expenses and plan accordingly. Additionally, it's important to be aware of any waiting periods or limitations on certain services, as these can impact the timing and accessibility of care.

In conclusion, a thorough understanding of the coverage details is essential for families to determine whether a health insurance plan meets their specific needs and provides adequate protection. By carefully reviewing the included and excluded services, families can make an informed decision about the value of the plan and its potential benefits for their health and financial well-being.

Higher Income, Better Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Network Providers: Check if your preferred doctors and hospitals are within the insurance network

One of the critical factors to consider when evaluating the worth of family health insurance is the network of providers it offers. Ensuring that your preferred doctors and hospitals are within the insurance network is essential to maximize the benefits of your plan. This involves researching the insurance provider's list of in-network healthcare professionals and facilities to confirm that they align with your family's healthcare needs and preferences.

To begin this process, obtain a comprehensive list of in-network providers from your insurance company. This list should include primary care physicians, specialists, hospitals, and other healthcare facilities. Carefully review the list to identify any gaps in coverage, such as missing specialists or limited hospital options. If your preferred healthcare providers are not included in the network, you may need to consider alternative plans or negotiate with your insurance company to add them to the network.

It's also important to consider the geographic location of the providers. Ensure that the in-network doctors and hospitals are conveniently located near your home or workplace to minimize travel time and expenses. Additionally, verify the credentials and reputation of the providers to ensure that they meet your standards for quality care.

Another aspect to consider is the continuity of care. If you have existing health conditions or ongoing treatments, it's crucial to ensure that your current healthcare providers are included in the network to maintain continuity of care. Disruptions in treatment can lead to negative health outcomes and increased costs.

Finally, don't overlook the importance of mental health coverage. Ensure that the insurance network includes mental health professionals and facilities to address any mental health needs that may arise. This is particularly important for families with children, as access to mental health services can be critical for their overall well-being.

In conclusion, thoroughly vetting the network of providers is a key step in determining the value of family health insurance. By confirming that your preferred doctors and hospitals are included, you can ensure that your family receives the best possible care while maximizing the benefits of your insurance plan.

Understanding the Role of a Producer in Health Insurance Plans

You may want to see also

Explore related products

![]()

Deductibles and Co-Pays: Consider the out-of-pocket expenses you'll need to cover before insurance kicks in

Understanding deductibles and co-pays is crucial when evaluating the worth of family health insurance. A deductible is the amount you must pay out of pocket before your insurance coverage begins. For instance, if your deductible is $1,000, you'll need to cover the first $1,000 of medical expenses each year before your insurance takes effect. Co-pays, on the other hand, are fixed amounts you pay for each medical service or prescription, usually after meeting your deductible. For example, you might have a $20 co-pay for doctor visits and a $10 co-pay for generic medications.

When considering whether family health insurance is worth it, it's essential to weigh the potential out-of-pocket expenses against the benefits of having coverage. High deductibles and co-pays can make insurance seem less attractive, especially for families on a tight budget. However, insurance can still provide significant savings in the event of major medical expenses, such as hospitalizations or surgeries, which can cost tens of thousands of dollars without coverage.

To determine if family health insurance is worth it, you should calculate your expected annual medical expenses, including deductibles and co-pays. Compare this amount to the cost of insurance premiums and the potential savings from having coverage. Additionally, consider the peace of mind that comes with knowing your family is protected in case of unexpected health issues.

It's also important to note that some insurance plans offer ways to reduce out-of-pocket expenses, such as health savings accounts (HSAs) or flexible spending accounts (FSAs). These accounts allow you to set aside pre-tax dollars for medical expenses, which can help offset the cost of deductibles and co-pays. Furthermore, many insurers offer telemedicine services, which can provide convenient and cost-effective access to medical care for minor issues.

In conclusion, while deductibles and co-pays are important factors to consider when evaluating family health insurance, they should not be the sole determining factor. By carefully weighing the costs and benefits of insurance, families can make an informed decision about whether coverage is worth it for their specific situation.

NAU Student Medical Insurance: What's Covered?

You may want to see also

Explore related products

![Health Insurance Benefits Advisory Council annual report on Medicare covering the period ... Volume 1966-1967 1967 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Peace of Mind: Reflect on the value of having financial protection against unexpected health issues for your loved ones

Reflecting on the value of having financial protection against unexpected health issues for your loved ones brings to light the profound peace of mind it can offer. This isn't merely about the monetary aspect; it's about ensuring that your family can navigate through health crises without the added burden of financial strain. Imagine a scenario where a family member falls ill unexpectedly. Without adequate health insurance, the costs of treatment can quickly escalate, leading to difficult decisions about care and potentially significant debt.

The psychological impact of such situations can be immense. Financial stress can exacerbate the emotional toll of a health crisis, affecting not just the patient but the entire family. Having a robust family health insurance plan in place acts as a safety net, allowing you to focus on what truly matters – the health and recovery of your loved one. It's about having the assurance that, regardless of the medical expenses incurred, your family's financial stability remains intact.

Moreover, health insurance often provides access to better healthcare facilities and specialists, which can be crucial in critical situations. This access can lead to quicker diagnoses, more effective treatments, and ultimately, better health outcomes. In the long term, this can translate into fewer complications, reduced recovery times, and a higher quality of life for your family members.

Considering these aspects, the value of family health insurance extends far beyond its financial benefits. It's an investment in your family's overall well-being, offering a layer of security that allows you to face health challenges with confidence and resilience. The peace of mind that comes with knowing your loved ones are protected against unexpected health issues is invaluable, making family health insurance a worthwhile consideration for anyone looking to safeguard their family's future.

Medicare Health Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Family health insurance can be worth the cost if it provides comprehensive coverage for all family members, potentially saving money in the long run by covering unexpected medical expenses.

The benefits of family health insurance include financial protection against high medical costs, access to a network of healthcare providers, and the convenience of managing one plan for all family members.

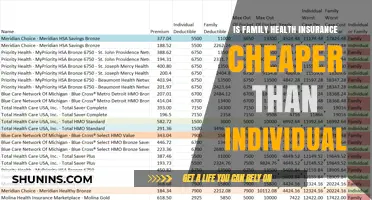

Family health insurance typically offers a lower cost per person compared to purchasing individual plans for each family member. It also simplifies the process of managing multiple policies.

When choosing a family health insurance plan, consider factors such as the plan's coverage, premiums, deductibles, co-pays, network of providers, and any additional benefits or riders that may be available.

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UY218_.jpg)