Gap insurance is not a form of PPI. It is a type of auto insurance that covers the difference between the amount owed on a car loan or lease and the vehicle's market value in the event of an accident or theft. This protection ensures that drivers are not left paying for a car they can no longer drive. While gap insurance is not mandatory, it might be required by financing agreements and lease contracts.

| Characteristics | Values |

|---|---|

| Type of insurance | Optional car insurance |

| Purpose | Covers the "gap" between what a car is worth and what the driver owes on their auto loan or lease if the car is totaled or stolen |

| Cost | $400 to $700 when purchased from a dealership; $20 to $40 per year when added to a car insurance policy; $3 per month |

| When to buy | When you owe more on your car than it is worth; when you have a small down payment; when you have a long-term loan; when you have a car that depreciates in value quickly |

| When to drop | When the amount you owe is less than the car's value or only slightly more |

| Where to buy | Car insurance companies; banks and credit unions; car dealerships |

Explore related products

What You'll Learn

![]()

When is gap insurance required?

Gap insurance is required when a driver's car loan requires it. It is also generally mandatory when leasing a vehicle.

Gap insurance is an optional form of auto insurance that covers the difference between the compensation received after a total loss of a vehicle and the amount still owed on the car loan. It is also known as guaranteed auto protection or guaranteed asset protection insurance.

Gap insurance is a good idea for drivers who:

- Made a small down payment or no down payment at all

- Have a long finance period

- Purchased a vehicle that depreciates faster than average

- Rolled over negative equity from an old car loan into the new loan

It is not required for drivers who:

- Made a down payment of at least 20% on the car

- Are paying off the car loan in less than five years

- Own their car outright

- Owe less on their car than its current actual cash value

Self-Insuring Vehicles in New York

You may want to see also

Explore related products

![]()

What is the cost of gap insurance?

Gap insurance is not a form of PPI, but rather a type of auto insurance. It covers the difference between the amount reimbursed by the driver's car insurance policy and the amount they owe on their financing in the event of a total loss. This includes incidents where the car is damaged, written off, or stolen.

The cost of gap insurance depends on several factors, including your state, driving record, and vehicle. It is typically purchased as an endorsement on an existing car insurance policy or as separate coverage from a dealer. The cost of adding gap insurance to an existing auto insurance policy is relatively low, at around $20 per year. However, purchasing gap insurance from a dealership is generally more expensive.

The average cost of gap insurance is $60 per year, but rates can vary depending on the insurance provider. For example, Travelers offers an average rate of $34 per year. It is recommended to shop around and compare rates from different insurers to find the best deal.

It is worth noting that gap insurance is not mandatory, but it may be required by your financing agreement. It is also important to review the terms of your car loan to determine if gap insurance is necessary. If you are leasing a car, you may be required to purchase gap insurance.

Additionally, gap insurance can be added to your existing car insurance policy as an endorsement, or you can purchase separate coverage from a dealer. It is worth comparing the costs of both options to determine which one best suits your needs.

Vehicle Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

What does gap insurance cover?

Gap insurance is an optional form of auto insurance that covers the difference between the amount you owe on your auto loan and the amount your insurance company pays if your car is stolen or totalled. This type of insurance is designed for people who finance or lease their vehicles. It is not required by law, but it might be required by your financing agreement.

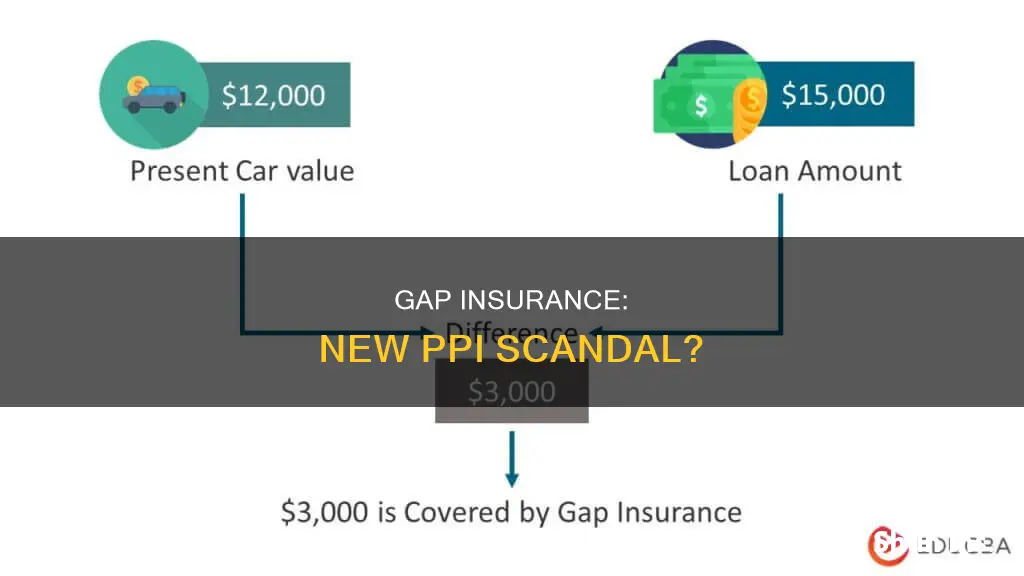

Gap insurance covers the "gap" between your car's actual value (not the amount you paid) and your outstanding lease or loan balance. For example, if you finance a $25,000 car and it is totalled in an accident a few months later, your insurance company will reimburse you based on the car's current value, not the price you paid. If the insurance adjuster determines that the actual cash value of your car is $20,000, but your loan balance is $24,000, you will be short $4,000 of what you owe, even though you no longer have a car. Gap insurance would cover this $4,000 difference.

Gap insurance is worth considering if you made a small down payment (less than 20%), financed for 60 months or longer, leased the vehicle, purchased a vehicle that depreciates faster than average, or rolled over negative equity from an old car loan. It is also a good idea if you plan to put a lot of miles on your vehicle, which can speed up depreciation.

On the other hand, gap insurance may not be necessary if you own your vehicle outright or if you make a large down payment that brings your loan amount below the car's value. Gap insurance also does not cover costs related to vehicle repairs, personal injuries, or other accident-related expenses. If you want coverage for these types of expenses, you will need to purchase additional policies, such as liability insurance, uninsured motorist insurance, or personal injury protection (PIP).

Fault and Insurance: Who's Liable?

You may want to see also

Explore related products

![]()

When should you get gap insurance?

Gap insurance is an optional form of auto insurance that covers the difference between the compensation you receive after a total loss of your vehicle and the amount you still owe on a car loan. It is not a form of PPI.

You should consider getting gap insurance if:

- You made a small down payment on your vehicle.

- You have a long finance period.

- You purchased a vehicle that depreciates quickly.

- You leased the vehicle (gap insurance is generally required for a lease).

- You rolled over negative equity from an old car loan into the new loan.

- You plan to put miles on quickly.

- You took out a car loan with a long term (more than 60 months).

Gap insurance is typically inexpensive, costing around $40 to $60 per year if added to a car insurance policy that includes collision and comprehensive insurance. It can also be purchased from a dealer, but this option tends to be more expensive, costing hundreds of dollars per year.

U.S.A.A. Insurance: Kia Coverage

You may want to see also

Explore related products

![]()

Where can you buy gap insurance?

Gap insurance is not a form of PPI. It is a type of auto insurance that covers the difference between a car's actual value and the balance left on a loan or lease. It is designed to protect automobile owners if their car is totalled or stolen. It is not mandatory, but it might be required by your financing agreement.

You can buy gap insurance from your car dealer, your auto insurance company, or a company offering stand-alone gap insurance policies. If you're buying or leasing a new car, the dealer will likely ask if you want to purchase gap insurance when you discuss your financing options. Buying gap insurance from a dealer can be more expensive if the cost of the coverage is bundled into your loan amount, which means you'd be paying interest on your gap coverage.

You can typically add gap coverage to an existing car insurance policy or a new policy, as long as your loan or lease hasn't been paid off. Buying gap insurance from an insurance company may be less expensive, and you won't pay interest on your coverage. If you already have car insurance, you can check with your current insurer to determine how much it would cost to add gap coverage to your existing policy. Note that you need comprehensive and collision coverage in order to add gap coverage to a car insurance policy.

It may be worth comparing the costs of both options to see which one is the best fit for your needs. The cost of gap insurance depends on your state, driving record, age, vehicle, and other factors.

Motor Vehicle Insurance: Protection and Peace of Mind

You may want to see also

Frequently asked questions

Gap insurance is a type of auto insurance that covers the difference between the amount reimbursed by the driver's car insurance policy and the amount they owe on their financing or lease agreement.

PPI stands for Payment Protection Insurance.

No, gap insurance is not a form of PPI. Gap insurance is a type of auto insurance, whereas PPI is typically associated with loans or credit deals.

Gap insurance covers the "gap" between what a car is worth and what the driver owes on their auto loan or lease if the car is totaled or stolen.

Gap insurance is worth it if you owe more on your car loan or lease than your car is worth. It is also useful if you've made a small down payment, have a long-term loan, or own a car that depreciates quickly.