Health insurance is a critical aspect of modern healthcare systems, providing financial protection and access to medical services for individuals and families. The question of whether health insurance is nationwide pertains to the scope and reach of these systems across different countries. In some nations, health insurance is indeed universal, covering all citizens and residents regardless of their employment status or income level. Examples include countries like Canada, the United Kingdom, and Australia, which have publicly funded healthcare systems that ensure comprehensive coverage. In contrast, other countries, such as the United States, have a more fragmented approach, with a mix of private insurance providers and public programs like Medicare and Medicaid, resulting in varying levels of coverage and access to care. This disparity highlights the ongoing debate about the most effective and equitable ways to organize and fund healthcare systems on a national scale.

Explore related products

What You'll Learn

- Eligibility Criteria: Varying requirements across states for Medicaid and other state-sponsored programs

- Coverage Options: Differences in private insurance plans, state-specific policies, and federal programs like Medicare

- Cost Variations: How premiums, deductibles, and out-of-pocket costs differ by state and plan type

- Provider Networks: Availability and accessibility of healthcare providers under different insurance plans across states

- State Regulations: Overview of how each state regulates health insurance, including consumer protections and market rules

![]()

Eligibility Criteria: Varying requirements across states for Medicaid and other state-sponsored programs

Eligibility criteria for Medicaid and other state-sponsored programs vary significantly across the United States, creating a complex landscape for individuals seeking health insurance coverage. While Medicaid is a federal program, states have considerable leeway in determining who is eligible for coverage, leading to a patchwork of different requirements and qualifications.

For instance, some states have expanded Medicaid under the Affordable Care Act (ACA), extending coverage to low-income adults who do not have children. However, other states have chosen not to expand Medicaid, leaving many low-income individuals without access to health insurance. Additionally, states may impose different income limits, asset tests, and work requirements for Medicaid eligibility, further complicating the application process.

The variation in eligibility criteria also extends to other state-sponsored programs, such as the Children's Health Insurance Program (CHIP) and state-funded health insurance exchanges. While CHIP is designed to provide coverage to low-income children, states may set different income limits and eligibility requirements, potentially leaving some children without access to health insurance. Similarly, state-funded health insurance exchanges may offer different plans and subsidies, depending on the state's policies and budget.

Navigating these varying eligibility criteria can be challenging for individuals and families seeking health insurance coverage. It is essential to understand the specific requirements and qualifications for each state-sponsored program to determine eligibility and access the necessary coverage. Resources such as the Medicaid website and state-specific health insurance exchanges can provide valuable information and guidance for those navigating the complex landscape of health insurance eligibility in the United States.

Understanding Blood Test Coverage: What Your Health Insurance Includes

You may want to see also

Explore related products

![]()

Coverage Options: Differences in private insurance plans, state-specific policies, and federal programs like Medicare

Private insurance plans offer a wide range of coverage options, varying significantly from one provider to another. These plans can be tailored to individual needs, offering flexibility in terms of deductibles, co-pays, and out-of-pocket maximums. However, the extent of coverage and the specific services included can differ greatly, with some plans providing comprehensive care while others may have more limited benefits. It's crucial for individuals to carefully review and compare private insurance plans to ensure they select one that meets their healthcare needs and budget.

State-specific policies play a significant role in shaping the healthcare landscape within each state. These policies can dictate the types of services that must be covered by insurance providers operating within the state, as well as the regulations governing the insurance market. For example, some states may require insurance plans to cover certain pre-existing conditions or provide specific benefits, such as mental health services or prescription drugs. Understanding state-specific policies is essential for residents to navigate their healthcare options effectively.

Federal programs like Medicare provide a safety net for millions of Americans, particularly those aged 65 and older, as well as certain younger individuals with disabilities. Medicare is a standardized program that offers a specific set of benefits, including hospital care, physician services, and prescription drug coverage. While Medicare provides essential coverage, it also has its limitations, such as deductibles, co-pays, and gaps in coverage for certain services. Beneficiaries may choose to supplement their Medicare coverage with additional private insurance plans or state-specific programs to address these gaps.

The differences between private insurance plans, state-specific policies, and federal programs like Medicare highlight the complexity of the healthcare system in the United States. Each type of coverage has its own unique features, benefits, and limitations, making it challenging for individuals to navigate their options and select the best plan for their needs. It's essential for consumers to educate themselves about the various coverage options available to them and to carefully consider their healthcare needs and budget when making decisions about health insurance.

Understanding Co-Payment in Health Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Cost Variations: How premiums, deductibles, and out-of-pocket costs differ by state and plan type

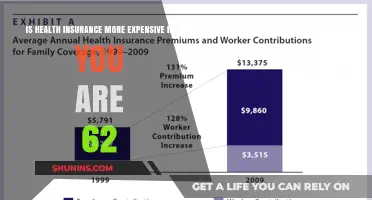

Health insurance costs can vary significantly across different states and plan types, making it essential for consumers to understand these differences when selecting a policy. Premiums, deductibles, and out-of-pocket costs are key components that contribute to the overall expense of health insurance.

Premiums, which are the monthly payments made to the insurance company, can differ based on factors such as the state of residence, age, health status, and the type of plan chosen. For instance, a Bronze plan in Texas may have a lower premium compared to a Gold plan in California due to differences in healthcare costs and market conditions.

Deductibles, the amount paid out-of-pocket before the insurance company starts covering costs, also vary by plan and state. High-deductible plans, often associated with lower premiums, may be more suitable for individuals who are generally healthy and do not anticipate frequent medical expenses. Conversely, low-deductible plans, which typically have higher premiums, may be preferable for those with chronic conditions or who require regular medical care.

Out-of-pocket costs, including copayments and coinsurance, can also differ significantly depending on the plan and state. These costs represent the portion of medical expenses that the insured individual must pay after meeting the deductible. Understanding these variations is crucial for consumers to estimate their potential healthcare expenses accurately.

To navigate these cost variations effectively, it is advisable for individuals to compare plans and prices across different states, considering factors such as their health needs, budget, and eligibility for subsidies or tax credits. Utilizing online comparison tools or consulting with a licensed insurance agent can provide valuable insights and help consumers make informed decisions about their health insurance coverage.

Major Medical Insurance: Who Needs to Be Covered?

You may want to see also

Explore related products

![]()

Provider Networks: Availability and accessibility of healthcare providers under different insurance plans across states

The availability and accessibility of healthcare providers under different insurance plans can vary significantly across states. Insurance companies often negotiate contracts with healthcare providers to create networks that offer services at discounted rates to policyholders. However, these networks may not be uniform nationwide, leading to disparities in access to care depending on where you live.

For instance, a study by the Commonwealth Fund found that the percentage of primary care physicians accepting new patients with Medicaid varied widely across states, from as low as 43% in California to as high as 80% in New Hampshire. This variation can have a substantial impact on the ability of individuals to access timely and affordable healthcare services.

Moreover, the types of providers available within a network can also differ by state. Some states may have a higher proportion of specialists, while others may have more primary care physicians. This imbalance can affect the overall quality of care and the ability of patients to receive comprehensive healthcare services.

Another factor to consider is the impact of state regulations on provider networks. States may have different laws and regulations governing the formation and operation of these networks, which can influence the availability and accessibility of healthcare providers. For example, some states may require insurance companies to include certain types of providers in their networks, while others may not have such mandates.

In conclusion, the availability and accessibility of healthcare providers under different insurance plans are complex issues that can vary widely across states. Understanding these variations is crucial for policymakers, healthcare providers, and patients to ensure that everyone has access to high-quality, affordable healthcare services.

Does McDonald's Offer Health Insurance to Its Employees?

You may want to see also

Explore related products

![]()

State Regulations: Overview of how each state regulates health insurance, including consumer protections and market rules

While health insurance is a federal program in the United States, individual states play a significant role in regulating the industry within their borders. Each state has its own set of laws and regulations that govern how health insurance companies operate, what plans they can offer, and how they must protect consumers. This state-by-state approach can lead to a complex patchwork of rules and protections, which can vary widely from one state to another.

One key area of state regulation is consumer protection. States have laws that require health insurers to provide clear and accurate information about their plans, including coverage details, premiums, and out-of-pocket costs. Many states also have rules that protect consumers from unfair or deceptive practices, such as denying coverage for pre-existing conditions or canceling policies without proper notice. Additionally, some states have established their own health insurance exchanges, which allow consumers to compare and purchase plans from multiple insurers in a more transparent and competitive marketplace.

Another important aspect of state regulation is market rules. States can impose regulations on how health insurers set their premiums, what benefits they must offer, and how they can market their plans. For example, some states require insurers to spend a certain percentage of premium dollars on healthcare services and quality improvement, rather than on administrative costs or profits. Other states have laws that limit the ability of insurers to deny coverage or charge higher premiums to individuals with pre-existing conditions.

The variation in state regulations can have a significant impact on the availability and affordability of health insurance for consumers. In some states, consumers may have access to a wide range of plans and protections, while in others, they may face more limited options and fewer safeguards. This disparity can also affect the overall health of the population, as states with stronger regulations may be better able to ensure that their residents have access to necessary healthcare services.

In conclusion, while health insurance is a federal program, state regulations play a crucial role in shaping the industry and protecting consumers. The complex and varied nature of these regulations highlights the importance of understanding the specific rules and protections that apply in each state. By doing so, consumers can make informed decisions about their health insurance coverage and ensure that they are taking advantage of the protections available to them.

Living Without Health Insurance: Our Family's Risky Reality and Concerns

You may want to see also

Frequently asked questions

Nationwide health insurance refers to a policy that provides coverage across the entire country, allowing policyholders to access healthcare services and facilities in any state or region.

While nationwide health insurance offers extensive coverage, there may be some limitations or restrictions, such as out-of-network providers, pre-existing conditions, or specific treatments that may not be covered. It's essential to review the policy details carefully.

Nationwide health insurance provides coverage across the entire country, whereas local or regional health insurance typically restricts coverage to a specific geographic area, such as a city, state, or region. This means that policyholders with nationwide insurance have more flexibility in choosing healthcare providers and facilities.