Hurricane insurance is not a separate coverage, and it is included in homeowners insurance to an extent. Homeowners insurance policies typically cover wind damage, but damage caused by flooding may not be covered. If you live in a high-risk area, such as along the Atlantic Coast, you may need a separate home insurance deductible for hurricane losses. In some states, a hurricane deductible will only apply if the National Weather Service declares the storm to be a hurricane, while in other states, the hurricane must reach a specific category level.

| Characteristics | Values |

|---|---|

| Hurricane insurance | Doesn't exist as a separate coverage |

| Flood insurance | Not included in homeowners insurance; must be purchased separately |

| Wind damage | Usually covered by homeowners insurance |

| Hurricane deductible | May be higher than the standard deductible; depends on the state |

| Loss of use coverage | May be included in homeowners insurance and cover hotel, meals, and living expenses |

| High-risk areas | Insurers may limit or withhold wind damage coverage; higher deductibles may apply |

Explore related products

What You'll Learn

![]()

Hurricane insurance doesn't exist as a separate coverage

The term "hurricane deductible" refers to a specific type of deductible that comes into play when dealing with claims related to hurricane damage. It is important to note that the conditions under which a hurricane deductible will apply may vary from state to state. Some states require the National Weather Service to declare the storm a hurricane, while others mandate that the hurricane reaches a specific category level, such as 3 or 4.

In the context of homeowner's insurance, a deductible refers to the amount you must pay out of pocket before your insurance policy begins to cover your losses. A hurricane deductible is typically a percentage of the insured value of your home, ranging from 2% to 5%. For example, if your dwelling coverage is $200,000 and you file a $10,000 claim for hurricane damage, your insurer will pay you $6,000 if your claim is approved, and you will be responsible for the remaining $4,000.

Additionally, if you live in a high-risk area for hurricanes, such as along the Atlantic Coast, your policy may include a "named storm" deductible. This deductible will apply once a storm has reached a certain strength, such as when it becomes a named hurricane. It is important to review your homeowner's insurance policy carefully to understand the specific deductibles and coverages that apply to hurricane damage.

Furthermore, it is worth noting that some states, such as Mississippi, have made changes to windstorm and flood policies. In these states, insurers have imposed percentage deductibles instead of fixed-dollar deductibles to limit their liability in coastal areas. As a result, homeowners in these states may face higher out-of-pocket expenses when filing hurricane-related insurance claims.

Foal Insurance: Proving Their Worth and Value

You may want to see also

Explore related products

$9.99 $9.99

![]()

Home insurance covers wind damage

Home insurance typically covers wind damage, including that caused by hurricanes and tornadoes. However, it's important to note that coverage may vary depending on your location and the specifics of your policy. Some policies may have higher deductibles or exclusions for windstorm damage, so it's essential to carefully review your policy to understand what is covered.

Wind damage is one of the most common causes of damage from storms, and it can lead to destruction to roofs, windows, siding, and other parts of your home. Home insurance policies usually offer coverage for the costs of repair and replacement associated with wind damage. This includes damage to the structure of your home as well as your personal belongings. If you have ""other structures coverage," wind damage to roofs on other structures on your property, like a shed or freestanding garage, may also be covered.

In the case of high-risk areas, such as along the Atlantic Coast or in certain coastal states, insurers may limit or withhold wind damage coverage. Some states also have specific triggers for hurricane deductibles, and your policy may include a ""named storm" deductible, which applies once a storm reaches a certain strength. For example, if a hurricane causes damage to your property, your hurricane deductible will apply.

Additionally, it's worth noting that standard home insurance policies typically do not cover flood damage, especially when caused by weather-related events. If you live in an area prone to flooding or hurricanes, you may need to purchase separate flood insurance or seek out a special endorsement to ensure coverage for water damage.

Overall, while home insurance typically covers wind damage, it's important to carefully review your policy, understand your deductibles, and be aware of any exclusions or limitations to ensure you have the necessary coverage in the event of a storm or hurricane.

Shared Property: What's Covered by Homeowners Insurance?

You may want to see also

Explore related products

![]()

Flood damage usually requires separate insurance

Hurricane damage can come from many sources, including wind, rain, and flooding. While homeowners insurance policies typically cover wind damage, they often exclude flood damage. This means that if your home is damaged by flooding during a hurricane, your insurance policy may not cover the repairs.

Flood damage is usually considered a separate risk and requires its own insurance policy. This is because flooding can cause extensive and costly damage to properties, and insurers want to limit their exposure to such risks. As a result, you will likely need to purchase separate flood insurance to protect your home against flooding from external sources, such as storm surges or heavy rainfall.

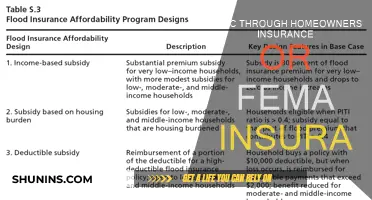

The National Flood Insurance Program (NFIP), managed by FEMA, is the largest single-line insurance program in the nation, providing $1.3 trillion in coverage against floods. You can purchase flood insurance through the NFIP directly or through a network of over 50 insurance companies. It's important to note that there is typically a 30-day waiting period for a new NFIP policy to take effect, so it's crucial to plan ahead and not wait until the last minute.

Some private insurers also offer flood endorsements that can be added to your existing homeowners policy. These endorsements provide additional coverage for flood-related incidents. However, it's important to carefully review the terms and conditions of any insurance policy, including flood endorsements, to fully understand what is and isn't covered.

If you live in a high-risk flood zone or an area prone to hurricanes, it's essential to consider the potential impact of flooding and ensure you have adequate coverage. Don't wait until it's too late; prepare in advance by reviewing your insurance policies and making any necessary adjustments to protect your home and belongings.

Air Vac Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

High-risk areas may have higher deductibles

Homeowners in high-risk areas may face higher deductibles. A hurricane deductible is the amount of money you must pay toward a hurricane-related loss before your insurance company starts to pay. This replaces your regular deductible and is laid out in the policy. Currently, homeowners in 19 states and Washington, D.C., must pay hurricane deductibles instead of their regular deductibles when making a hurricane damage claim.

The typical hurricane deductible is 1% to 5% of the home’s insured value, although policies in some vulnerable coastal areas can see deductibles as high as 10%. Florida has a mandated $500 flat fee hurricane deductible option in addition to designated percentages. Each state and insurer has its own definition, but generally, it means a weather system declared a hurricane by the National Weather Service’s National Hurricane Center.

In certain states, the National Weather Service must declare the storm to be a hurricane for the deductible to apply. In other states, the hurricane must reach a specific category level, such as 3 or 4. A "named storm" deductible, commonly referred to as a "hurricane deductible," will apply once a storm has reached a certain strength. For example, if a storm moves beyond a tropical depression and becomes a named hurricane that causes damage to your property, your hurricane deductible will apply.

Insurers in hurricane-prone states may limit or withhold wind damage coverage. If wind coverage is not included in your home insurance policy, you can seek out a special endorsement. Many coastal states subsidize wind pools, providing coverage for those in high-risk areas.

Homeowners Insurance: Moving Damage Covered by State Farm?

You may want to see also

Explore related products

![]()

Loss of use coverage pays for temporary living expenses

Loss of use coverage, also known as Additional Living Expenses (ALE) insurance or Coverage D, is typically included in standard homeowners, condo, or renters policies. It pays for temporary living expenses and additional costs incurred when a covered event makes a house uninhabitable while it is being repaired or rebuilt. This includes expenses that you would not have incurred if you were living in your own home, such as the cost of temporary housing (e.g. a hotel), transportation, boarding a pet, and additional food expenses. Loss of use coverage will pay the difference between your normal expenses and the increased expenses due to the loss. For example, if you normally spend $100 on gas but this increases to $150 because you are staying in a hotel further from work, loss of use coverage will reimburse you for the $50 difference.

It is important to note that loss of use coverage does not pay for expenses that you were already responsible for before the loss, such as mortgage payments, insurance, or childcare expenses. It only covers additional expenses that occur because you cannot live in your home. The coverage is typically limited by time, often for 12 or 24 months, or by a monetary amount, usually capped at 15-20% of the dwelling coverage amount. To make a claim, you must provide receipts for all your additional living expenses and proof of your normal expenses to show the increase in costs.

Home Insurance: Can You Expect a Decrease in Premiums?

You may want to see also

Frequently asked questions

Hurricane insurance does not exist as a separate coverage. The damage caused by hurricanes comes from different sources, including wind and flooding from storm surges and rain.

Most homeowners insurance policies cover wind damage. However, if you live in an area with a high risk of hurricanes, insurers may limit or withhold wind damage coverage.

Flood damage is typically not covered by standard homeowners insurance policies. If you live in a high-risk area, you may need to purchase separate flood insurance.

A hurricane deductible is a percentage deductible that applies specifically to hurricane damage claims. Instead of paying a fixed amount, you pay a percentage of the insured value of your home, typically between 2% and 5%.

First, contact your insurance agent to file a claim and initiate the recovery process. Take pictures and videos of the damage, as these may be needed by the insurance company. If necessary, take steps to prevent further damage, such as covering holes with a tarp.