Borrowing from your 401(k) or life insurance is a complex topic and there is conflicting advice on which is better. Some experts say 401(k) loans should be a last resort, while others argue they should be the first choice for borrowing. Both options have pros and cons and it's important to understand the implications of each. 401(k) loans can provide quick access to cash with no impact on your credit score, but they may affect your investment growth and come with fees and tax implications. Life insurance loans may offer more flexibility in terms of repayment and borrowing limits, but it's important to consider the potential impact on your policy and the fees involved. Ultimately, the best option depends on individual circumstances and it's crucial to carefully evaluate both choices before making a decision.

| Characteristics | Values |

|---|---|

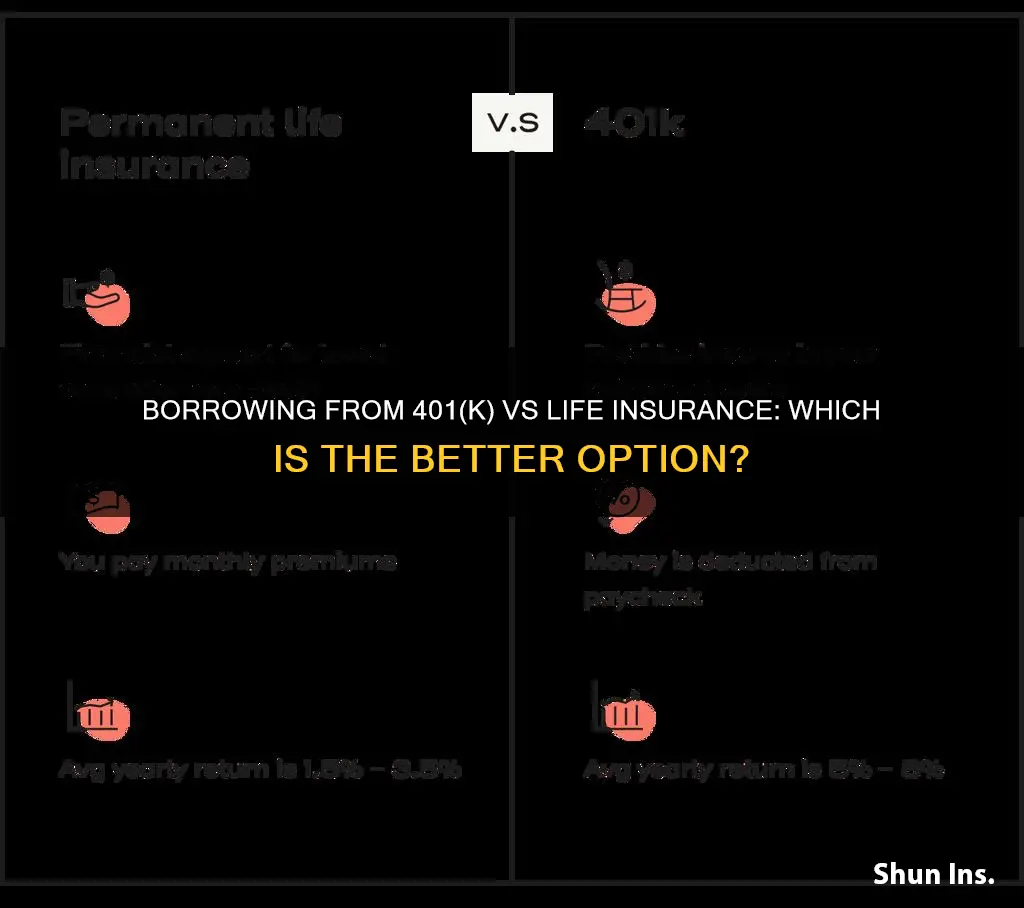

| Ease of Access | 401(k) loans are generally easier to access than life insurance loans, requiring no credit check or lengthy applications. |

| Speed | Life insurance loans are typically faster, with funds available in a few days compared to two weeks or more for 401(k) loans. |

| Convenience | 401(k) loans can be requested through a few clicks on a website and are often accompanied by privacy. |

| Repayment Flexibility | 401(k) loans have mandatory repayment schedules but allow for faster repayment without prepayment penalties. Life insurance loans offer more flexibility, with no set repayment schedules and the ability to skip payments. |

| Cost | 401(k) loans may have lower interest rates compared to other loan options, and interest is paid back into the participant's account. Life insurance loans may have higher fees and charges. |

| Impact on Investment Performance | 401(k) loans can negatively impact investment performance by reducing the balance and slowing down growth. Life insurance loans may not affect account growth, especially if funds are borrowed during a market downturn. |

| Tax Efficiency | 401(k) loans are not considered taxable events, but repayments are made with after-tax dollars, which can lead to double taxation. Life insurance loans are also not taxable events and do not impact credit ratings. |

| Default Consequences | Defaulting on a 401(k) loan can result in penalties and taxes, and leaving a job with an unpaid loan can lead to immediate repayment requirements. Defaulting on a life insurance loan may have less severe consequences, and there is more flexibility in repayment. |

| Purpose | 401(k) loans are intended for short-term liquidity needs and should be considered for specific situations rather than long-term borrowing. Life insurance loans can be used for various purposes, including financing vacations, education, or business expansion. |

Explore related products

What You'll Learn

![]()

Pros and cons of 401(k) loans

Borrowing from your 401(k) plan can be a quick and convenient way to access cash, but it's important to carefully consider the pros and cons before making a decision. Here are some key points to help you understand the potential benefits and risks of taking out a 401(k) loan:

Pros of 401(k) Loans:

- Simple application process: There is no lengthy loan application process as you are borrowing from yourself. You will still need to provide some basic information to your plan administrator, and spousal consent may be required for married individuals.

- No taxes or penalties: Unlike hardship withdrawals, 401(k) loans do not incur taxes or early withdrawal penalties as long as you make regular payments.

- Potentially lower interest rates: The interest rate on a 401(k) loan is usually a point or two above the prime rate, which can be more favourable than traditional loan interest rates. Additionally, the interest you pay goes back into your retirement account.

- No impact on your credit score: 401(k) loans are not reported to the major credit bureaus and do not affect your credit score. This can be advantageous if you have a low credit score or are concerned about maintaining your credit rating.

- Convenient repayment through payroll deductions: Repaying the loan is made easier as payments are automatically deducted from your paycheck.

Cons of 401(k) Loans:

- Strict repayment schedules: 401(k) loans typically have a maximum repayment period of five years, and this may be accelerated if you leave your job. Failing to repay the loan on time can result in taxes and penalties.

- Opportunity cost and loss of investment growth: By borrowing from your 401(k), you are missing out on potential investment returns and the power of compound interest. The money you borrow would have continued to grow in the market, and the longer it stays out of your account, the more you may lose out on potential gains.

- No bankruptcy protection: In the event of bankruptcy, 401(k) loans cannot be discharged, and you will still be responsible for repaying the loan or face early withdrawal penalties and taxes.

- Job loss concerns: If you change jobs or experience unemployment, you will likely be required to repay the outstanding loan balance within a short period, typically by the next tax day. This can put a strain on your finances during an already challenging time.

- Limited borrowing amount: The IRS sets loan limits, and you can borrow up to 50% of your vested account balance or $50,000, whichever is less. This restriction may not allow you to access as much cash as you need.

Collateral Assignment: Life Insurance Contract Flexibility

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

![]()

Pros and cons of life insurance loans

Pros of a Life Insurance Policy Loan

- You can skip the lengthy loan application process.

- You can borrow without a credit check or any questions from a lender if you have built up cash value on your policy.

- Policy loans don't show up on your credit report.

- You can repay the loan on your own schedule.

- You have the option of not repaying the loan and having it deducted from the policy's death benefit instead.

- You can access your loan funds quickly.

- You can use the loan funds for whatever you choose.

- Loans do not have to be paid back.

- Money from an insurance policy loan is not taxed as income.

Cons of a Life Insurance Policy Loan

- You may have to wait several years for the policy to build a cash value.

- You could risk a reduced death benefit for your family if the loan isn't repaid while you're living.

- There's a risk of losing your policy if the amount of interest plus the unpaid loan adds up to more than the remaining cash value of the policy.

- If you take the cash value as a loan, there is no protection from creditors.

- If you take many loans over many years, and that causes the policy to lapse, you could owe income tax on the amount you borrowed that was greater than your premium paid.

- You will owe interest on the loan.

- Failing to repay your loan may result in losing insurance coverage.

Cashing in on Mutual Savings: Life Insurance Options

You may want to see also

Explore related products

![]()

How to know which option is best for you

When deciding between borrowing from your 401(k) or life insurance, it's important to consider the pros and cons of each option and evaluate which one aligns better with your financial goals and situation. Here are some factors to help you determine the best choice for you:

- Speed and Convenience: If you need quick access to funds, borrowing from your 401(k) can be faster and more convenient than a traditional loan. It usually involves a simpler application process without lengthy paperwork or credit checks, and you can often receive the funds within a few days.

- Repayment Flexibility: 401(k) loans typically offer repayment flexibility, allowing you to repay the loan faster without prepayment penalties. However, life insurance loans may provide even more flexibility by letting you decide on a repayment schedule that suits you.

- Cost Advantage: Compare the cost of borrowing from your 401(k) with that of a traditional loan. Consider factors such as interest rates, fees, and the opportunity cost of missing out on potential investment growth. Calculate the potential cost advantage of each option to determine which is more financially beneficial for you.

- Tax Implications: Understand the tax implications of both options. Withdrawing from a 401(k) before retirement age usually incurs taxes and early withdrawal penalties. Life insurance loans, on the other hand, typically don't have the same tax consequences.

- Job Security: If you're confident about your job security and don't anticipate changing jobs soon, borrowing from your 401(k) may be a viable option. However, if you're concerned about potential job loss, life insurance loans may be a safer choice, as 401(k) loans typically need to be repaid immediately upon leaving a job.

- Investment Growth: By borrowing from your 401(k), you're reducing the balance of your account and missing out on potential investment growth. If investment performance is a priority for you, consider the impact of each option on your portfolio's long-term growth.

- Fees and Penalties: Evaluate the fees and penalties associated with each option. 401(k) loans may have processing and maintenance fees, while life insurance loans could have surrender charges if you withdraw money early. Understand the fee structure of each choice to make an informed decision.

- Credit Score Impact: Borrowing from your 401(k) typically doesn't affect your credit score, whereas taking out a traditional loan might. If maintaining your credit score is important, this could be a factor in your decision.

- Loan Amount: Consider your required loan amount. 401(k) loans usually have limits on how much you can borrow, while life insurance loans may provide more flexibility in this regard.

- Financial Emergency: Evaluate your financial situation and the nature of your need for funds. If you're facing a true financial emergency and have limited options, borrowing from your 401(k) might be a last resort. However, it's crucial to consider all other alternatives first.

Remember, it's always a good idea to consult a financial professional or advisor before making significant financial decisions. They can provide personalized advice based on your unique circumstances.

Life Insurance Agents: How Their Pay Structure Works

You may want to see also

Explore related products

![]()

How to avoid needing a 401(k) loan

Borrowing from your 401(k) should be a last resort, but there are ways to avoid needing to do so. Here are some strategies to avoid taking a loan from your 401(k):

Preemptive planning

If you know you have a large expense coming up, such as a college tuition bill, try to pre-plan and set financial goals for yourself. This way, you can save up the funds in a different account and won't need to borrow from your 401(k). Mike Loo, vice president of wealth management at Trilogy Financial, advises that "if you are able to take the time to preplan, set financial goals for yourself, and commit to saving some of your money both often and early, you may find that you have the funds available to you in an account other than your 401(k), thereby preventing the need to take a 401(k) loan."

Compare all your borrowing options

Before taking a loan from your 401(k), consider all the other ways you could borrow money. For example, you could take out a personal loan, use a home equity line of credit (HELOC), or tap into your emergency savings. Weigh the pros and cons of each option and choose the one that best suits your needs and financial situation.

Keep contributing to your 401(k)

It might be tempting to reduce or pause your contributions to your 401(k) while you're paying off a loan, but it's essential to keep up with your regular contributions to maintain your retirement strategy. Remember that the money you borrow from your 401(k) is losing out on potential investment growth, so continuing to contribute can help offset this.

Only borrow for a short-term, necessary expense

If you're considering borrowing from your 401(k), make sure it's for a necessary, one-time expense and not for elective purchases like entertainment or gifts. Borrowing from your 401(k) should be a rare occurrence and only done when you need a meaningful amount of cash in the short term.

Life Insurance and Tax Returns: What's the Connection?

You may want to see also

Explore related products

![]()

What to do if you lose your job with a 401(k) loan

If you lose your job, your 401(k) plan will likely require you to pay back the loan within 60 to 90 days. If you are unable to do so, the outstanding balance will be treated as a distribution, which has tax implications and may include an early withdrawal penalty if you are under 55 or 59.5 years old. Here are some steps you can take to manage this situation:

- Review your plan's rules: Check your plan's summary description to understand the specific requirements and deadlines for loan repayment in the event of job loss. Some plans may offer a short grace period after employment ends.

- Explore repayment options: If possible, use your available cash or savings to pay off the loan. If your savings are limited, consider taking out a new 401(k) loan with your new employer or borrowing from your spouse's 401(k) plan, if applicable.

- Roll over the loan offset: If you cannot repay the loan in full, you may be able to roll over the loan offset amount into a new employer's 401(k) plan or a rollover IRA to avoid immediate tax consequences. You typically have 60 days or until the tax filing deadline (including extensions) to complete the rollover.

- Understand the tax implications: If you don't repay the loan or roll over the offset amount, the loan offset will be treated as a taxable distribution. You will owe regular income taxes on the offset amount, plus an early distribution penalty if you are under the applicable age.

- Consider the impact on your credit: Defaulting on a 401(k) loan typically does not affect your credit score since these loans are not reported to credit bureaus. However, the reduction in your retirement savings may impact your overall financial health.

- Seek alternative sources of funding: If you need additional funds to repay the loan, consider taking out a personal loan or a home equity loan. Review your credit report and score to improve your chances of obtaining favourable loan rates and terms.

- Consult a financial advisor: Before making any decisions, consider speaking with a financial advisor or tax professional to understand your options and the potential short-term and long-term financial implications.

Life Insurance Trust: Protecting Your Family's Future

You may want to see also

Frequently asked questions

Borrowing from a 401(k) can be a quick, simple, and low-cost way to get cash. There is no credit check or impact on your credit score, and you pay yourself back with interest.

Borrowing from your 401(k) can reduce your investment growth, create another monthly expense, and lead to a balloon payment situation if you lose your job. Additionally, there are limits on how much you can borrow, and you may have to pay loan processing and maintenance fees.

Borrowing from life insurance can be more flexible, with no government restrictions on how much you can borrow or when you repay. There are also no taxes, penalties, or fees for skipping payments.

Life insurance loans may have high fees and can reduce your policy's cash value. Additionally, the interest rates on life insurance loans may be higher than those on 401(k) loans.