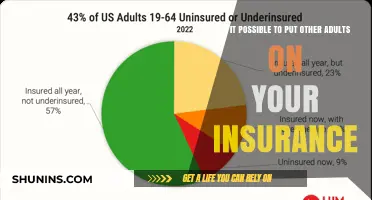

The question of whether it is normal for Americans not to have insurance is a complex and multifaceted issue deeply rooted in the country's healthcare system and cultural attitudes. Unlike many developed nations with universal healthcare, the United States relies heavily on employer-based insurance and private markets, leaving millions uninsured or underinsured. Factors such as high premiums, lack of employer-provided coverage, and gaps in public programs like Medicaid contribute to this reality. While recent reforms like the Affordable Care Act have reduced uninsured rates, significant disparities persist, particularly among low-income individuals, part-time workers, and those in states that have not expanded Medicaid. Thus, while it is not uncommon for some Americans to lack insurance, it remains a pressing societal concern with far-reaching implications for health, finances, and equity.

Explore related products

What You'll Learn

![]()

High healthcare costs deterring insurance enrollment

The soaring cost of healthcare in the United States has created a paradox: the very system designed to protect Americans from financial ruin is often unaffordable, leaving many uninsured. This isn't merely a matter of personal choice; it's a systemic issue where the fear of medical debt outweighs the perceived benefits of coverage.

A 2022 Commonwealth Fund survey revealed that 44% of underinsured adults reported problems paying medical bills, highlighting the financial strain even those with some coverage face.

Consider a hypothetical scenario: a 35-year-old individual earning $40,000 annually. A basic health insurance plan with a $4,000 deductible and $300 monthly premium would consume nearly 10% of their pre-tax income. Factor in potential out-of-pocket costs for doctor visits, prescriptions, and unforeseen medical events, and the financial burden becomes staggering. For many, this equation simply doesn't add up, leading them to gamble on their health rather than invest in insurance.

This isn't a lack of understanding of insurance's value; it's a calculated risk driven by economic necessity.

The consequences of this cost-driven deterrence are far-reaching. Uninsured individuals often delay preventative care, leading to more severe and costly health issues down the line. They're also more likely to rely on emergency rooms for primary care, further straining the healthcare system. This vicious cycle perpetuates high costs, making insurance even less attainable for those who need it most.

Breaking this cycle requires addressing the root cause: the exorbitant cost of healthcare itself. Policy solutions like negotiating drug prices, expanding Medicaid eligibility, and promoting price transparency are crucial steps. Until these systemic changes are implemented, the high cost of healthcare will continue to be a barrier to insurance enrollment, leaving millions of Americans vulnerable to financial hardship and compromising their overall health.

Soft Stool Solutions: Hemorrhoid Relief Through Smart Diet Choices

You may want to see also

Explore related products

![]()

Employer-based coverage limitations and gaps

Employer-based health insurance, while a cornerstone of the American healthcare system, is riddled with limitations and gaps that leave millions vulnerable. One glaring issue is the tie between employment and coverage, which means job loss often equates to insurance loss. During the COVID-19 pandemic, for instance, over 14 million Americans lost their employer-sponsored insurance as unemployment soared, highlighting the precarious nature of this arrangement. Even those who retain their jobs aren’t immune; part-time workers, freelancers, and employees of small businesses are frequently excluded from employer plans, creating a patchwork of coverage that disproportionately affects low-wage earners.

Another critical limitation is the rising cost burden on employees. While employers typically share the cost of premiums, the employee’s share has been steadily increasing. According to the Kaiser Family Foundation, the average annual premium for family coverage in 2023 was $23,968, with workers contributing $6,575—a 43% increase since 2013. High deductibles and out-of-pocket costs further strain budgets, making even "covered" individuals hesitant to seek care. For example, a plan with a $3,000 deductible means a family must pay that amount before insurance kicks in, a daunting figure for households living paycheck to paycheck.

The variability in plan quality and scope is another significant gap. Employer-based plans are not standardized, and benefits can differ widely. Some plans exclude critical services like mental health care, maternity care, or prescription drugs, leaving employees underinsured. A 2022 study found that 28% of workers in employer plans reported difficulty affording their deductibles, and 23% skipped care due to cost. This variability means that even insured Americans may face gaps in coverage, depending on their employer’s chosen plan.

Finally, job lock—the phenomenon where employees stay in jobs solely to retain health insurance—stifles career mobility and entrepreneurship. A 2021 survey revealed that 38% of workers felt trapped in their jobs because of health benefits, limiting their ability to pursue better opportunities or start businesses. This not only harms individual growth but also stifles economic innovation. For those transitioning between jobs, COBRA continuation coverage is often prohibitively expensive, leaving a dangerous gap in protection during career shifts.

To mitigate these gaps, individuals should explore supplemental insurance options, negotiate employer benefits where possible, and stay informed about policy changes like the Affordable Care Act’s marketplace plans. Employers, meanwhile, can prioritize comprehensive, affordable plans to retain talent and foster employee well-being. Until systemic reforms decouple insurance from employment, these strategies offer practical ways to navigate the limitations of employer-based coverage.

Cashing in on Globe Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Young adults avoiding insurance due to perceived health

A significant number of young adults in the United States forgo health insurance, often citing their perceived good health as the primary reason. This demographic, typically aged 18 to 34, frequently believes they are invincible, immune to serious illnesses or accidents. However, this mindset overlooks the unpredictable nature of health and the potential financial devastation of unexpected medical expenses.

A 2020 Commonwealth Fund survey revealed that 15% of adults aged 19 to 25 were uninsured, the highest rate among all age groups. This statistic highlights a concerning trend, as young adulthood is a period marked by increased independence, new responsibilities, and often, a sense of invincibility.

This avoidance of insurance stems from a combination of factors. Firstly, young adults often prioritize other expenses, such as rent, student loans, and entertainment, over health insurance premiums. Secondly, the complexity of insurance plans and the perceived difficulty of navigating the healthcare system can be daunting. Lastly, the misconception that being young and healthy equates to not needing insurance persists, fueled by a lack of health literacy and a focus on short-term financial concerns.

A young adult might reason, "I'm healthy, I exercise, I eat well, why do I need insurance?" This line of thinking ignores the reality of accidents, sudden illnesses, and the long-term benefits of preventative care. A broken bone from a sports injury, a surprise diagnosis, or even routine check-ups can quickly accumulate significant costs without insurance coverage.

To combat this trend, it's crucial to educate young adults about the importance of health insurance. This includes highlighting the potential financial consequences of being uninsured, explaining the different types of plans available, and emphasizing the value of preventative care. Utilizing peer-to-peer communication and social media platforms can be effective in reaching this demographic. Additionally, simplifying the enrollment process and offering affordable, tailored plans specifically designed for young adults can increase accessibility and encourage participation.

Finding Life Insurance Prospects: Strategies for Success

You may want to see also

Explore related products

![]()

Policy complexities confusing potential enrollees

The labyrinthine nature of insurance policies often deters potential enrollees, leaving many Americans uninsured or underinsured. A 2021 Kaiser Family Foundation survey revealed that 40% of uninsured adults found the enrollment process "difficult" or "very difficult," citing complexity as a primary barrier. This confusion stems from a multitude of factors, including dense jargon, convoluted plan structures, and a lack of standardized terminology across providers.

Consider the following scenario: A 35-year-old individual earning $40,000 annually seeks health insurance. They encounter terms like "deductible," "coinsurance," and "out-of-pocket maximum," each with varying definitions and implications. Without a clear understanding of these concepts, they may inadvertently choose a plan with a $6,000 deductible, only to realize later that they cannot afford the upfront costs. This example highlights the need for simplified, standardized language in policy documents.

To navigate this complexity, potential enrollees should follow a structured approach. First, identify key terms and their definitions using resources like Healthcare.gov's glossary. Next, compare plans based on specific needs, such as prescription drug coverage or specialist visits. For instance, a diabetic individual should prioritize plans with lower copays for insulin and regular check-ups. Caution should be exercised when considering plans with unusually low premiums, as these often come with higher out-of-pocket costs.

A comparative analysis of policy structures reveals that high-deductible health plans (HDHPs) paired with health savings accounts (HSAs) can be cost-effective for healthy individuals under 40. However, this option may not suit those with chronic conditions or families with children, who typically require more frequent medical services. For example, a family of four with an annual income of $70,000 might benefit from a PPO plan with a $3,000 deductible and comprehensive coverage for pediatric care.

Ultimately, addressing policy complexities requires a two-pronged strategy: insurers must simplify their documentation, and enrollees must proactively educate themselves. Practical tips include attending enrollment workshops, using online calculators to estimate costs, and consulting licensed brokers. By demystifying the process, more Americans can make informed decisions, reducing the number of uninsured individuals and improving overall health outcomes.

How to Apply for Life Insurance on Someone Else's Behalf

You may want to see also

Explore related products

$14.77 $18

![]()

Cultural attitudes toward personal responsibility in healthcare

In the United States, the notion of personal responsibility in healthcare is deeply ingrained in cultural attitudes, often influencing decisions about health insurance. Unlike many developed nations with universal healthcare systems, the U.S. relies heavily on employer-based or privately purchased insurance, leaving a significant portion of the population uninsured. This gap is not merely a policy issue but a reflection of broader societal beliefs about self-reliance and individual accountability. For many Americans, forgoing insurance is seen as a calculated risk, a choice rooted in the cultural ethos of independence. This mindset is particularly prevalent among younger, healthier individuals who may view insurance premiums as an unnecessary expense, prioritizing immediate financial needs over potential future health costs.

Consider the case of Sarah, a 28-year-old freelance graphic designer in Texas. She earns just above the threshold for Medicaid eligibility but cannot afford private insurance. Sarah rationalizes her decision by emphasizing her healthy lifestyle—regular exercise, a balanced diet, and no chronic conditions. Her perspective mirrors a common cultural narrative: if you take care of yourself, you shouldn’t need insurance. However, this logic overlooks the unpredictability of accidents or sudden illnesses, which can lead to catastrophic debt. Sarah’s situation highlights how personal responsibility, when taken to an extreme, can become a double-edged sword, fostering resilience but also vulnerability.

From a comparative standpoint, this attitude contrasts sharply with countries like Germany or Japan, where health insurance is mandatory and viewed as a collective responsibility. In the U.S., the emphasis on individual choice often frames healthcare as a commodity rather than a right. This perspective is reinforced by political discourse that equates government intervention with overreach, further entrenching the idea that managing one’s health is a personal duty. For instance, the Affordable Care Act’s individual mandate, which required most Americans to have insurance or pay a penalty, was met with resistance from those who saw it as an infringement on personal freedom.

To navigate this cultural landscape, practical steps can be taken to balance personal responsibility with risk mitigation. For those without insurance, community health clinics offer affordable preventive care, while short-term health plans can provide temporary coverage for unexpected illnesses. Additionally, health savings accounts (HSAs) allow individuals to set aside pre-tax dollars for medical expenses, combining self-reliance with financial planning. However, these solutions are not without limitations—short-term plans often exclude pre-existing conditions, and HSAs require consistent income to fund effectively.

Ultimately, the cultural attitude toward personal responsibility in healthcare in the U.S. reflects a complex interplay of individualism and systemic challenges. While self-reliance is a cherished value, its application to healthcare can lead to unintended consequences, such as delayed treatment or financial hardship. Bridging this gap requires not only individual action but also a reevaluation of societal norms and policies. Until then, Americans like Sarah will continue to weigh their beliefs against the realities of an unpredictable health landscape.

Understanding Insurance Premiums: How to Calculate and Charge Fairly

You may want to see also

Frequently asked questions

While many Americans have health insurance, it is not uncommon for some to be uninsured. Factors like cost, employment status, and eligibility for government programs contribute to gaps in coverage.

Some Americans forgo insurance due to high premiums, deductibles, or a belief they don’t need it. Others may fall into coverage gaps, such as not qualifying for Medicaid but unable to afford private plans.

Yes, it is legal to be uninsured in most states. The federal penalty for not having insurance under the Affordable Care Act (ACA) was eliminated in 2019, though some states have their own mandates.