Medicaid is a joint federal and state program that provides health insurance coverage to millions of Americans, primarily those with low income, including eligible low-income adults, children, pregnant women, elderly adults, and people with disabilities. Established in 1965 under the Social Security Act, Medicaid is administered by states, which operate their own programs within federal guidelines, ensuring a safety net for vulnerable populations who might otherwise lack access to healthcare. Unlike Medicare, which is primarily for individuals aged 65 and older, Medicaid eligibility is based on income and other criteria, making it a critical component of the U.S. healthcare system. The program covers a wide range of medical services, including doctor visits, hospital stays, long-term care, and preventive care, though specific benefits can vary by state. As a means-tested entitlement program, Medicaid plays a vital role in reducing health disparities and improving health outcomes for low-income individuals and families across the nation.

Explore related products

What You'll Learn

- Eligibility Requirements: Income limits, citizenship status, and residency rules for Medicaid qualification

- Covered Services: Doctor visits, hospital stays, prescriptions, and preventive care included in Medicaid

- Application Process: Steps to apply, required documents, and online/in-person submission methods

- State Variations: Differences in Medicaid benefits, eligibility, and programs across states

- Managed Care Plans: How Medicaid uses managed care organizations for coordinated healthcare services

![]()

Eligibility Requirements: Income limits, citizenship status, and residency rules for Medicaid qualification

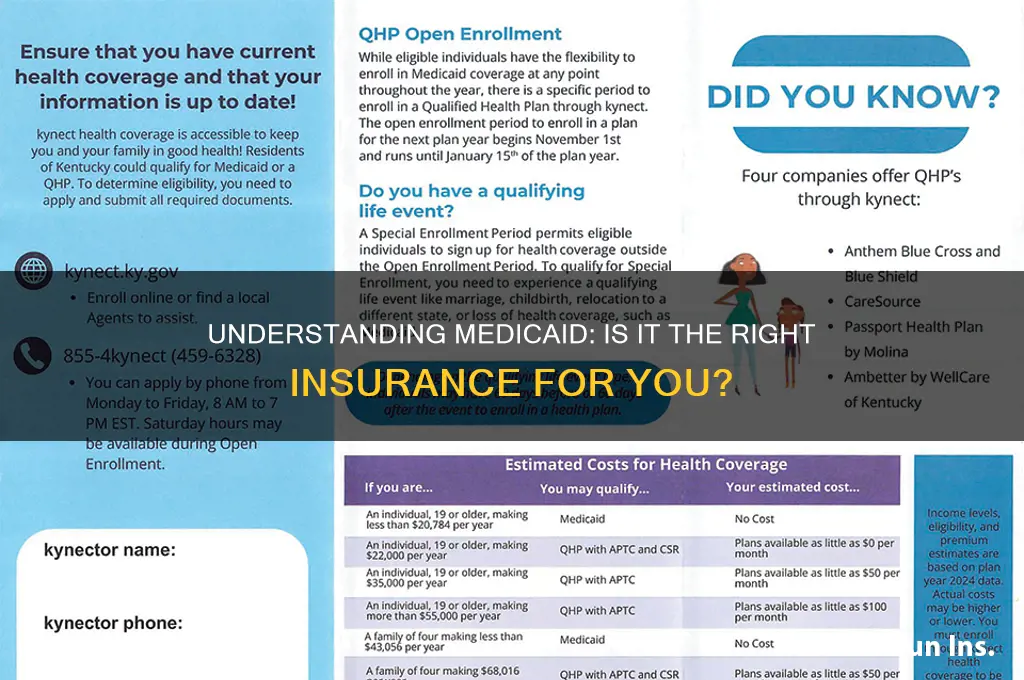

Medicaid eligibility is a complex interplay of financial, legal, and geographic criteria, each designed to ensure the program serves its intended population: low-income individuals and families. At its core, Medicaid is a needs-based program, but "need" is defined far beyond income alone. Understanding these requirements is crucial for anyone navigating the application process, as missing even one criterion can result in disqualification.

Income Limits: The Foundation of Eligibility

Medicaid income limits vary significantly by state and household size, but they are universally tied to the Federal Poverty Level (FPL). For example, in 2023, a single adult in most states may qualify with an annual income up to 138% of the FPL ($18,754), while a family of four might qualify with an income up to $38,295. However, not all income is counted equally. States often exclude certain earnings, such as tax refunds or child support payments, from eligibility calculations. Practical tip: Use the Healthcare.gov subsidy calculator to estimate your eligibility before applying, as it accounts for state-specific variations.

Citizenship Status: A Non-Negotiable Requirement

To qualify for Medicaid, individuals must be either U.S. citizens or meet specific immigration status criteria. Lawful permanent residents (green card holders) typically become eligible for Medicaid after five years of residency, though some states offer exceptions for pregnant women, children, or refugees. Undocumented immigrants are generally ineligible, though emergency services may be covered in some cases. Caution: Providing false citizenship information can lead to legal consequences, including deportation or ineligibility for future benefits.

Residency Rules: Localized Access to Care

Medicaid is a state-administered program, meaning eligibility is tied to your state of residence. Applicants must prove they live in the state where they’re applying, typically through a driver’s license, utility bill, or lease agreement. Seasonal workers or students may face challenges, as some states require physical presence for a minimum number of months per year. Example: A college student living on campus in a different state may need to apply in their home state if they maintain residency there.

The Intersection of Criteria: A Case Study

Consider a 30-year-old pregnant woman earning $20,000 annually. In a state with expanded Medicaid, she likely qualifies based on income. However, if she’s a recent immigrant without lawful status, she may be ineligible despite meeting financial criteria. Conversely, a U.S. citizen with the same income would qualify, provided she resides in the state where she applies. This example underscores the importance of evaluating all three criteria together, not in isolation.

Navigating the System: Practical Steps

- Gather Documentation: Collect proof of income (pay stubs, tax returns), citizenship (birth certificate, passport), and residency (utility bills, lease).

- Check State Rules: Visit your state’s Medicaid website to confirm income limits and any unique requirements.

- Apply Early: Eligibility can take weeks to process, so apply as soon as you meet the criteria.

- Appeal if Denied: If disqualified, request a fair hearing to review your case, especially if you believe there’s been an error.

By understanding and addressing income limits, citizenship status, and residency rules, applicants can maximize their chances of qualifying for Medicaid. This safety net program is designed to be accessible, but its rules demand careful attention to detail.

Cashing in on Life Insurance: Prudential's 1938 Policy Explained

You may want to see also

Explore related products

![]()

Covered Services: Doctor visits, hospital stays, prescriptions, and preventive care included in Medicaid

Medicaid, a joint federal and state program, provides essential health coverage to millions of low-income individuals and families. Among its most critical features are the covered services, which include doctor visits, hospital stays, prescriptions, and preventive care. These services form the backbone of Medicaid’s mission to ensure access to comprehensive healthcare for vulnerable populations. Understanding what is covered can help beneficiaries maximize their benefits and maintain their health effectively.

Doctor visits are a cornerstone of Medicaid coverage, ensuring beneficiaries can access primary and specialty care without financial barriers. Routine check-ups, chronic disease management, and urgent care needs are all included. For example, a diabetic patient can receive regular consultations with an endocrinologist, while a child can see a pediatrician for vaccinations and developmental screenings. Medicaid typically covers these visits at no cost to the patient, though some states may impose nominal copays. To make the most of this benefit, beneficiaries should establish a relationship with a primary care provider who can coordinate their overall healthcare needs.

Hospital stays, another critical covered service, provide financial protection during emergencies or serious illnesses. Medicaid covers inpatient care, including surgeries, maternity care, and treatment for acute conditions like pneumonia or heart attacks. For instance, a beneficiary requiring a knee replacement surgery would have the procedure, hospital room, and post-operative care covered. It’s important to note that Medicaid also covers emergency room visits, though beneficiaries are encouraged to use urgent care or primary care providers for non-life-threatening issues to avoid unnecessary costs to the system.

Prescription medications are a vital component of Medicaid’s covered services, ensuring beneficiaries can afford the drugs they need to manage chronic conditions or treat acute illnesses. Medicaid’s drug coverage is comprehensive, including both generic and brand-name medications. For example, a beneficiary with hypertension might receive coverage for lisinopril, a common blood pressure medication, at a low or no cost. Some states may require prior authorization for certain high-cost drugs, so beneficiaries should work with their healthcare providers to navigate these requirements. Additionally, Medicaid’s Preferred Drug List (PDL) can guide beneficiaries toward cost-effective options.

Preventive care is a key focus of Medicaid, aimed at detecting and addressing health issues before they become serious. Covered services include screenings for cancer, diabetes, and heart disease, as well as immunizations and counseling for healthy behaviors. For instance, women can access mammograms starting at age 40, while children receive regular well-child visits and vaccinations according to the CDC’s recommended schedule. Beneficiaries should take advantage of these services to prevent costly and debilitating health problems down the line. Practical tips include scheduling annual physicals, staying up-to-date on vaccinations, and discussing family medical history with providers to identify potential risk factors.

In summary, Medicaid’s covered services—doctor visits, hospital stays, prescriptions, and preventive care—provide a robust safety net for beneficiaries. By understanding and utilizing these benefits, individuals can maintain their health, manage chronic conditions, and avoid financial hardship. Whether it’s a routine check-up, emergency surgery, or a lifesaving medication, Medicaid ensures that essential healthcare remains within reach for those who need it most.

Leaving Insurance Money to Loved Ones: A Comprehensive Guide

You may want to see also

Explore related products

$14.52 $19.95

![]()

Application Process: Steps to apply, required documents, and online/in-person submission methods

Applying for Medicaid involves a structured process that varies slightly by state but generally follows a consistent framework. The first step is to determine your eligibility, which is primarily based on income, household size, and sometimes specific health conditions. Each state has its own income thresholds, often aligned with the Federal Poverty Level (FPL), so it’s crucial to check your state’s guidelines. For instance, pregnant women, children, and disabled individuals may qualify under different criteria than able-bodied adults. Once eligibility is confirmed, the application process begins.

The required documents for Medicaid applications typically include proof of identity (such as a driver’s license or state ID), Social Security numbers for all household members, and income verification (pay stubs, tax returns, or employer letters). Additional documents may be needed, such as proof of citizenship or immigration status, and medical records if applying due to a disability. Organizing these documents beforehand streamlines the process, as incomplete applications often result in delays. For families with children, school enrollment records or birth certificates may also be requested.

Applicants have two primary methods for submitting their Medicaid application: online or in-person. Online submission is the most convenient option, available through the Health Insurance Marketplace or directly on your state’s Medicaid website. The online portal guides you through each step, allowing you to upload documents and track your application status. In-person submission, on the other hand, involves visiting a local Department of Social Services office. This method is beneficial for those who prefer face-to-face assistance or lack internet access. Some states also offer mail-in applications, though this method is slower and less common.

Regardless of the submission method, accuracy is key. Double-check all entered information and ensure documents are legible if scanned or copied. Common mistakes, such as incorrect income reporting or missing signatures, can lead to application rejection. If you’re unsure about any part of the process, many states offer helplines or in-person assistance to guide applicants. For example, some states provide Medicaid navigators who can help you understand eligibility, gather documents, and complete the application.

After submission, the processing time varies but typically takes 45 days or less. Expedited processing is available for those in urgent need, such as pregnant women or individuals with severe health conditions. Once approved, beneficiaries receive a Medicaid card and information about their coverage. It’s essential to keep this documentation handy, as it’s required for accessing healthcare services. Understanding the application process and preparing accordingly can make the experience less daunting and increase the likelihood of a smooth approval.

Life Insurance and STD Testing: What You Need to Know

You may want to see also

Explore related products

![]()

State Variations: Differences in Medicaid benefits, eligibility, and programs across states

Medicaid, as a joint federal-state program, is not a one-size-fits-all solution. Each state has the flexibility to design its own Medicaid program within federal guidelines, leading to significant variations in benefits, eligibility criteria, and program structures. For instance, while all states must cover certain mandatory benefits like hospital stays and physician services, optional benefits such as dental care for adults or physical therapy vary widely. This state-level autonomy means that a low-income individual in Texas might have access to different services than someone in New York, even if their income levels are identical.

Consider eligibility criteria, which differ dramatically across states, particularly in those that have expanded Medicaid under the Affordable Care Act (ACA). As of 2023, 38 states and the District of Columbia have adopted expansion, raising the income eligibility threshold to 138% of the federal poverty level (FPL). In contrast, non-expansion states like Texas and Florida maintain much stricter eligibility limits, often below 50% of the FPL. This disparity leaves millions of low-income adults in a "coverage gap" where they earn too much to qualify for Medicaid but too little to afford private insurance. For example, a single adult in Texas earning $12,000 annually would not qualify for Medicaid, while someone with the same income in California would be eligible.

Program structures also vary, with states implementing different delivery models to manage care. Some states, like Oregon, use coordinated care organizations (CCOs) to integrate physical, mental, and dental health services. Others, like Florida, rely heavily on managed care organizations (MCOs) to administer benefits. These models influence not only the cost-effectiveness of the program but also the patient experience. For instance, a Medicaid beneficiary in Oregon might receive more holistic care through a CCO, while a beneficiary in Florida could face more fragmented services due to the MCO model.

Practical tips for navigating these variations include understanding your state’s specific Medicaid handbook, which outlines covered services and eligibility rules. For example, if you’re a pregnant woman in a non-expansion state, you may qualify for Medicaid even if your income exceeds standard limits, as pregnancy is a federally mandated eligibility category. Additionally, leveraging resources like the Healthcare.gov eligibility tool can help determine if you qualify based on your state’s criteria. If you’re moving across state lines, be aware that your Medicaid coverage may not transfer, and you’ll need to reapply under the new state’s rules.

In conclusion, the patchwork nature of Medicaid across states underscores the importance of local research and advocacy. While federal guidelines provide a baseline, state-level decisions ultimately shape who qualifies and what services are covered. Understanding these variations is crucial for individuals seeking coverage and for policymakers aiming to address disparities in access to care.

Can Joining AMA Lower Your Insurance Costs? Exploring the Benefits

You may want to see also

Explore related products

![]()

Managed Care Plans: How Medicaid uses managed care organizations for coordinated healthcare services

Medicaid, a joint federal and state program, provides health coverage to over 70 million low-income Americans. To streamline costs and improve care coordination, many states rely on Managed Care Organizations (MCOs). These entities act as intermediaries, contracting with Medicaid to deliver a defined set of services to enrollees for a fixed payment. This model shifts the financial risk from the state to the MCO, incentivizing efficient care delivery.

Consider a 35-year-old Medicaid beneficiary with diabetes. Under traditional fee-for-service Medicaid, she might see multiple specialists (endocrinologist, dietitian, ophthalmologist) who operate independently, leading to fragmented care. In a managed care plan, her MCO assigns her a primary care physician who coordinates her care, ensuring regular A1C tests (target: <7%), annual eye exams, and access to diabetes education classes. This coordinated approach reduces hospital admissions and improves health outcomes.

MCOs achieve coordination through several mechanisms. First, they establish provider networks, ensuring beneficiaries have access to necessary specialists. Second, they implement care management programs, such as case management for high-risk patients or disease management for chronic conditions like asthma (e.g., providing peak flow meters and action plans). Third, MCOs use data analytics to identify gaps in care, such as missed preventive screenings, and proactively intervene.

However, managed care isn’t without challenges. Critics argue that MCOs may prioritize profits over patient care, leading to denied services or narrow provider networks. For instance, a beneficiary needing a specific medication might face prior authorization delays. States must carefully monitor MCO performance through metrics like access to care, quality measures (e.g., childhood immunization rates), and beneficiary satisfaction surveys to ensure accountability.

For beneficiaries, understanding their managed care plan is crucial. Practical tips include: verifying that preferred providers are in-network, knowing how to appeal denied services, and utilizing care coordination resources like nurse hotlines. By leveraging MCOs effectively, Medicaid can balance cost control with the delivery of comprehensive, coordinated healthcare services.

Get Your Massachusetts Life Insurance License: A Guide

You may want to see also

Frequently asked questions

Yes, Medicaid is a government-funded health insurance program that provides coverage to eligible low-income individuals and families.

Eligibility for Medicaid varies by state but generally includes low-income adults, children, pregnant women, elderly individuals, and people with disabilities.

Medicaid covers a wide range of services, including doctor visits, hospital stays, and preventive care, but specific benefits may differ from private insurance and vary by state.