Medicare supplement insurance, also known as Medigap, is a private plan that covers additional costs not included in Original Medicare. It is important to understand the tax implications of Medicare supplement insurance when filing your tax returns. Generally, Medicare premiums are not considered pretax deductions, unlike employer-provided insurance plans. However, under certain circumstances, Medicare supplement insurance premiums may be tax-deductible.

| Characteristics | Values |

|---|---|

| Are Medicare premiums tax-deductible? | Yes, if you meet certain criteria. |

| What are the criteria? | If your medical expenses, including Medicare plan premiums, add up to 7.5% or more of your adjusted gross income (AGI) and you itemize your deductions. |

| Are there any exceptions? | If you are self-employed, you can deduct your Medicare premiums pre-tax. If you are over 65, you can deduct medical expenses exceeding 7.5% of your AGI. If you are not over 65, the threshold is 10% of your AGI. |

| What Medicare parts are included? | Medicare Part A, Part B, Part D, Medicare Advantage, and Medigap. |

Explore related products

What You'll Learn

![]()

Medicare Supplement plans are deductible

Medicare Supplement insurance plans, also known as Medigap plans, are offered by private insurance companies to help cover some of the out-of-pocket costs that Original Medicare (including Part A and Part B) does not pay for. These plans are designed to help with the costs that Original Medicare does not cover, such as copays, deductibles, and coinsurance. For example, most Medicare Supplement plans cover the Medicare Part A hospital deductible, while you are typically responsible for the Medicare Part B deductible.

Medicare Supplement plans can be deductible under certain circumstances. The Internal Revenue Service (IRS) allows the deduction of medical expenses, including health insurance premiums, from yearly taxes if they exceed 7.5% of the adjusted gross income (AGI). This applies to Medicare Supplement plans as well. This means that any premiums, deductibles, copayments, or coinsurance paid out of pocket for Medicare Supplement plans can be included in the list of tax deductions if they surpass 7.5% of the AGI.

It is important to note that the method of deduction matters. Unlike premiums for employer-provided insurance plans, Medicare premiums are generally not considered pretax and are not deducted from wages before taxes. Instead, Medicare premiums and other medical expenses must be deducted when filing your tax return. Additionally, these deductions can only be claimed on income tax returns, not employment taxes.

To determine the total medical expenses for tax itemized deductions, individuals should gather all medical receipts, SSA-1099 forms, summary notices, and insurance statements. This information, along with the individual's AGI, can be used to calculate the deductible amount.

In summary, Medicare Supplement plans can be deductible, but it depends on the individual's AGI and the amount spent on medical expenses, including premiums, deductibles, copayments, and coinsurance. It is always recommended to consult with a licensed tax professional to understand exactly what expenses are deductible and to maximize tax refunds.

Insurance Access to Medical Records: What's the Scope?

You may want to see also

Explore related products

![]()

Self-employed people can deduct health insurance premiums

If you are self-employed and your business shows a profit, you can claim your health insurance premiums as a tax deduction. This includes premiums for Medicare Parts A and B, Medicare Advantage, Part D prescription drug plans, and Medicare Supplement plans. However, you can only claim these deductions on your income tax return, not your employment taxes.

To qualify for deducting health insurance premiums, you must have reported net profit income as a sole proprietor on Schedule C or as a farmer on Schedule F. You can also qualify if you are a general partner, a limited partner receiving guaranteed payments, or an S corporation shareholder who owns more than 2% of the S corporation and receives W-2 wages.

It is important to note that the IRS Tax Code is very specific about what can and cannot be deducted, and not all regularly incurred expenses are eligible for deduction. Medicare costs are considered health expenses that can be deducted if they exceed 7.5% of your annual adjusted gross income for the current tax year. This includes not only Medicare premiums but also any unreimbursed medical or dental costs, such as copayments, deductibles, or coinsurance paid out of pocket.

Medical Insurance Essentials for African Safari Trips

You may want to see also

Explore related products

![]()

Deductibles, copays and out-of-pocket expenses

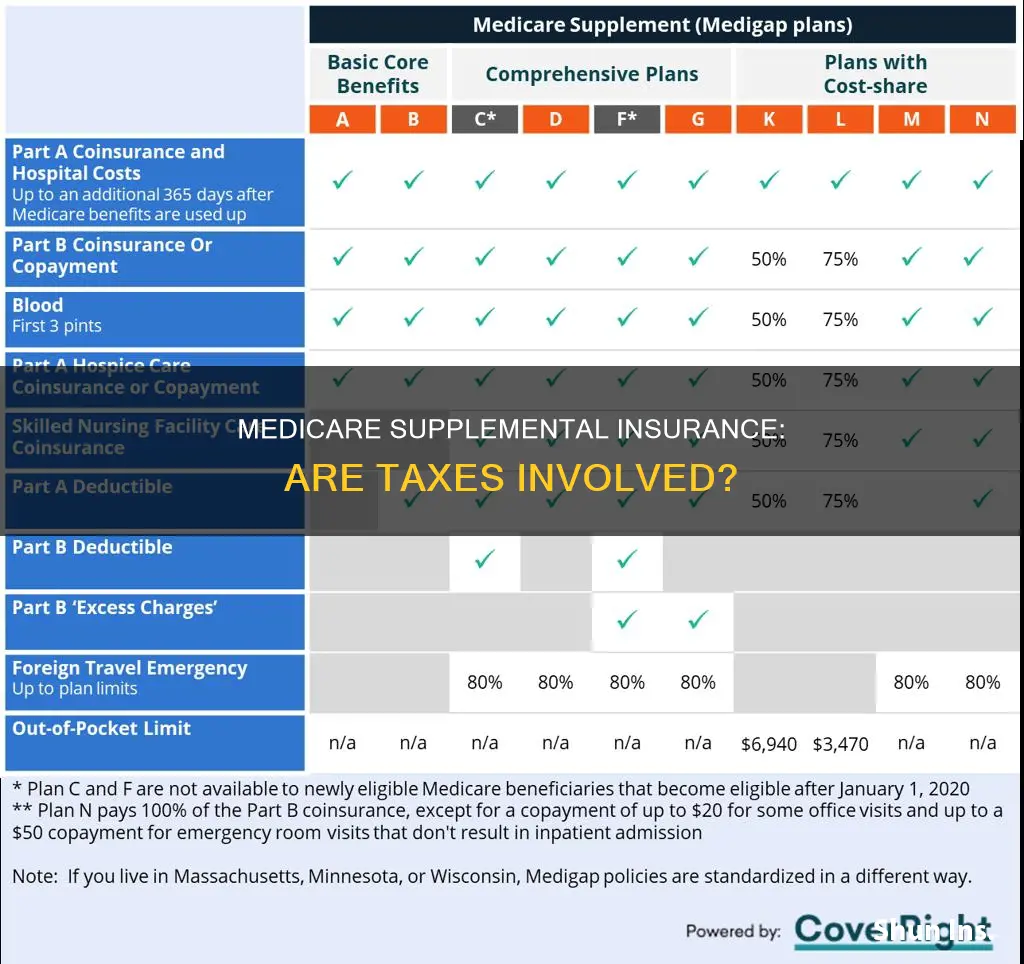

Medicare Supplement Insurance, also known as Medigap, helps fill the "gaps" in Original Medicare and is sold by private insurance companies. It can help cover most of the out-of-pocket costs that Original Medicare doesn't cover, including copays, coinsurance, and deductibles.

Medigap policies are sold by private carriers to provide wraparound coverage for Medicare Parts A and B costs. The way they set the price determines how much you'll pay in out-of-pocket costs. The Medicare deductible is the annual amount you pay for covered health care services before your Medicare plan starts to pay. Once you've met your deductible, you'll typically only pay a copayment or coinsurance, and Medicare pays the rest. For example, a hospital stay in 2025 that's covered under Medicare Part A will cost you $1,676 before Medicare coverage takes effect.

Medicare Supplement Insurance plans also provide flexibility in choosing any doctor or hospital in the US that accepts Medicare patients. These plans typically are standardized by the federal government and are named with a letter, like A, F, G, and N. You'll pay a monthly premium, for example, between $102 and $226, but it can help cover most of your out-of-pocket costs.

Medicare Supplement Plan F, for instance, has the broadest coverage of Original Medicare out-of-pocket costs. It helps cover Medicare deductibles, as well as some copayments and coinsurance. Plan F is only available to those who became eligible for Medicare before January 1, 2020. Plan G is another popular option, offering the broadest coverage for most people. It will pay for out-of-pocket costs that Original Medicare doesn't cover, except the Medicare Part B deductible.

Medicare Supplement Plan N offers a lower premium with some copays and a small annual deductible. This plan may be suitable if you're mainly concerned about covering Original Medicare Part A and Part B coinsurance costs. After enrolling in this plan, you'll need to continue paying your Original Medicare Part A and Part B premiums.

It's important to note that Medicare Supplement plans do not include prescription drug coverage, and most do not include dental, vision, or hearing coverage. Therefore, you may need to consider adding these benefits with standalone plans, including a prescription drug plan (Medicare Part D) for an additional premium.

Cigna-Healthspring Alliance Insurance: Accepted by TriStar Medical?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Tax-free withdrawals from health savings accounts

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that you can set up with a qualified HSA trustee to pay or reimburse certain medical expenses. You must be an eligible individual to contribute to an HSA. A qualified HSA trustee can be a bank, an insurance company, or anyone already approved by the IRS to be a trustee of individual retirement arrangements (IRAs) or Archer MSAs.

HSA contributions made by your employer (including contributions made through a cafeteria plan) may be excluded from your gross income. The contributions remain in your account until you use them. The interest or other earnings on the assets in the account are tax-free. HSA distributions may be tax-free if you pay qualified medical expenses.

If you receive distributions for other reasons, the amount you withdraw will be subject to income tax and may be subject to an additional 20% tax. You don’t have to make withdrawals from your HSA each year. If you are no longer an eligible individual, you can still receive tax-free distributions to pay or reimburse your qualified medical expenses. Generally, a distribution is money you get from your HSA. Your total distributions include amounts paid with a debit card and amounts withdrawn from the HSA by other individuals that you have designated.

Qualified medical expenses include (but aren’t limited to) incidental expenses for items like transportation, parking, meals, and hotels required for medical treatment. You can use your HSA contributions to pay for these expenses for yourself and your dependents.

Applying for CarePlus Insurance: A Simple Guide

You may want to see also

Explore related products

![]()

Additional out-of-pocket medical expenses

Medicare Supplement Insurance (Medigap) is extra insurance that can be purchased from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. Out-of-pocket (OOP) costs refer to what you're obliged to pay beyond what Medicare covers. These costs can change annually and are a significant consideration when choosing coverage.

Medigap policies are sold by private carriers to provide wraparound coverage for Medicare Parts A and B costs. For instance, the 2025 out-of-pocket maximum for Medigap Plan K is $7,220, while for Medigap Plan L, the MOOP (Maximum Out-of-Pocket) is $3,610. After reaching these limits, the plan pays 100% of approved service costs for the rest of the year.

Medicare Part D, which covers prescription drugs, also has out-of-pocket costs. In 2025, the Part D deductible can be no more than $590 per year, and the annual out-of-pocket cost is capped at $2,000. This cap ensures that those taking high-cost medications covered by Part D can benefit from significant savings.

Medicare Advantage (Part C) plans also have out-of-pocket maximums. In 2025, the standard maximum for Part C plans is $9,350 for approved services, but individual plans can set lower limits. Additionally, starting in 2025, all Medicare Advantage plans will have a $2,000 annual cap on out-of-pocket prescription drug costs, providing financial relief for those on fixed or limited incomes.

It's important to note that out-of-pocket costs can be mitigated through tax deductions. Medicare premiums, deductibles, and copayments can be deducted from your tax bill if they exceed 7.5% of your Adjusted Gross Income (AGI). This includes costs from Medicare Supplement plans, Medicare Advantage, and Medicare Part D. However, the IRS has specific criteria for deductions, and not all expenses are eligible.

Medical Insurance: A Universal Right or Privilege?

You may want to see also

Frequently asked questions

Medicare supplemental insurance premiums are deductible if they exceed a certain threshold. This is usually 7.5% of your annual adjusted gross income (AGI) for the current tax year.

If you or your spouse is over 65, you can deduct medical expenses that exceed 7.5% of your AGI. If you are under 65, the threshold is 10% of your AGI.

You can deduct any unreimbursed medical or dental costs, including copayments, deductibles, and coinsurance. You can also include the cost of eye surgery, medical equipment, and certain home improvements to accommodate a disability.

You can deduct your Medicare premiums when you file your tax return. You will need to itemize your deductions and include them in Schedule A, Itemized Deductions, for Form 1040.

Medicare premiums are generally not considered pre-tax. However, if you are self-employed, you can deduct your Medicare premiums pre-tax.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)