Medicare is the US health insurance program for people aged 65 or older. Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased to help cover out-of-pocket costs in Original Medicare. While there isn't a dedicated app specifically for Medicare supplemental insurance, there are several official Medicare apps that beneficiaries can use to access their health information, coordinate care with doctors, and find out if a procedure is covered by their insurance. These apps can be extremely beneficial for seniors who want to understand and maximize their Medicare coverage.

| Characteristics | Values |

|---|---|

| Name | Medicare Supplement Insurance (Medigap) |

| Type | Extra insurance to help pay your share of out-of-pocket costs in Original Medicare |

| Provider | Private insurance company |

| Eligibility | Must have Original Medicare Part A and Part B |

| Enrollment Period | 6-month "Medigap Open Enrollment" period starting the first month you have Medicare Part B and are 65 or older |

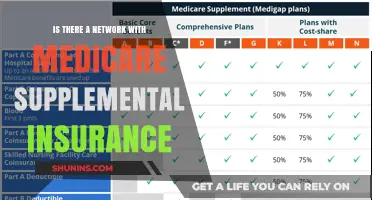

| Plans | 10 different types named by letters: A-D, F, G, and K-N; price is the only difference between plans with the same letter |

| State Variations | Discounts and plans may vary by state, e.g., Cigna's discount is not available in CT, DC, FL, MA, NJ, NY, OH, OR, and VT |

Explore related products

What You'll Learn

![]()

What is Medicare Supplement Insurance (Medigap)?

Medicare Supplement Insurance, also known as Medigap, is extra insurance that you can purchase from a private health insurance company. This insurance helps to pay your share of out-of-pocket costs in Original Medicare. Typically, to buy a Medigap policy, you must already have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). With a Medigap policy, both Medicare and your Medigap insurance will each pay their share of covered healthcare costs.

Medigap policies are standardised, meaning that insurance companies must offer the same benefits, with the only difference usually being the cost. You and your spouse must purchase separate Medigap policies, as a single policy will not cover healthcare costs for a spouse. Some Medigap policies may also offer additional benefits that are not covered by Medicare.

When purchasing a Medigap policy, you will need to pay a monthly premium for Medicare Part B, as well as a premium to the Medigap insurance company. As long as you continue to pay your premium, your Medigap policy is guaranteed to be renewable, meaning it will automatically renew each year. It's important to compare Medigap policies, as costs can vary.

While Medigap policies provide standardised benefits, they must also follow federal and state laws. These laws are in place to protect consumers. For example, in some states, insurance companies may refuse to renew a Medigap policy that was purchased before 1992. Additionally, the front of a Medigap policy must clearly identify it as "Medicare Supplement Insurance".

Should You Cancel Your Medical Insurance?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

What does Medigap cover?

Medigap, or Medicare Supplement Insurance, is extra insurance purchased from private health insurance companies to cover out-of-pocket costs associated with Original Medicare (Part A and Part B). While Medigap policies vary, they generally cover:

Deductibles

Medigap can help cover deductibles, which are the amounts you pay for covered health care services before your Medicare insurance starts paying.

Copayments

Medigap can also cover copayments, or copays, which are the fixed amounts you pay for specific covered health care services after you've met your deductible.

Coinsurance

Medigap can help with coinsurance, which is the percentage of the cost of a covered health care service that you share with your insurance provider. For example, if your Medicare Part B covers 80% of a service, your Medigap plan may cover the remaining 20%.

Foreign Travel Emergency Healthcare

Some Medigap plans cover foreign travel emergency healthcare, reimbursing a percentage of emergency medical costs incurred while travelling outside the United States. However, these plans often have specific requirements, such as a deductible and a lifetime coverage limit.

It's important to note that Medigap policies have varying coverage levels, and some services, like skilled nursing facility care or hospice care, may not be covered by all plans. Additionally, Medigap policies are subject to change annually, and factors like your location and age can influence the cost and availability of certain plans.

Islamic Perspective on Medical Insurance

You may want to see also

Explore related products

![]()

How much does Medigap cost?

The cost of Medigap, a private supplemental health insurance plan, varies depending on several factors. These include the insurance company, the plan, and the policyholder's location, age, health, and tobacco usage. The pricing method, state law, and other factors can also influence the cost.

Medigap premiums, which are paid monthly, can vary widely. On the lower end, plans can cost around $30 to $40 per month, while pricier plans can range from $150 to over $200 per month. The average monthly premium across all Medigap policyholders in 2023 was $217, but this varied by state, ranging from $191 in Alaska to $267 in New York.

The benefits offered by each lettered plan are standardised, but the premium amount can differ between insurance companies offering the same plan. For example, a $364 Medigap Plan G policy can offer the same coverage as one that costs $129. Companies may offer additional perks, such as discounted gym memberships, but the core Medicare benefits remain consistent.

Some Medigap plans have additional costs beyond their premiums. For example, Medigap Plan N has copays for certain office and emergency room visits, while Plans K and L require policyholders to pay a percentage of covered services out of pocket. High-deductible plans also require policyholders to meet a deductible before the Medigap policy pays out.

Insurance companies may offer discounts that can reduce the cost of Medigap policies. These discounts may be available for women, non-smokers, married people, yearly payments, electronic funds transfers, or multiple policies. Additionally, certain Medigap policies, such as Medicare SELECT, may have lower premiums if they require the use of specific providers.

Navigating State Insurance Cancellation with Medicaid Coverage

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)

![]()

Who can buy Medigap?

Medicare Supplement Insurance, or Medigap, is extra insurance that can be purchased from a private health insurance company. It helps to pay for out-of-pocket costs that Original Medicare (Part A and Part B) does not cover. Generally, to be eligible to buy a Medigap policy, you must already have Original Medicare.

Medigap policies are available to anyone who has Original Medicare, regardless of age, and there is no specific Medigap policy for spouses—each person must buy their own policy. However, it's important to note that Medigap policies are not available to those who have Medicare Advantage instead of Original Medicare. Additionally, those who are eligible for Medicaid do not need Medigap insurance as Medicaid covers their health care expenses.

The best time to buy a Medigap policy is during your Medigap Open Enrollment Period. This is a period when you can enroll in a Medigap policy with a guaranteed issue right, meaning you cannot be denied coverage or be charged more due to pre-existing health conditions. This period typically starts when you are enrolled in Part B of Medicare and are over the age of 65, and it lasts for six months. During this time, you have a guaranteed right to buy a Medigap policy, meaning insurance companies cannot deny you coverage, regardless of your health status.

If you miss your Medigap Open Enrollment Period, you may still be able to buy a Medigap policy, but you are not guaranteed the same level of coverage or protection. Insurance companies may consider your health status and charge you more or deny you coverage if you have pre-existing health conditions. Therefore, it is important to plan ahead and be aware of your Medigap Open Enrollment Period to ensure you get the best coverage possible.

Double Up: Can You Have Two Aetna Insurance Policies?

You may want to see also

Explore related products

![]()

How to buy Medigap

Medicare Supplement Insurance, or Medigap, is an extra insurance policy that can be purchased from a private health insurance company. It helps to cover some of the costs that the Original Medicare Plan does not, by paying its share of covered healthcare costs. Generally, you must have Original Medicare, including Part A (Hospital Insurance) and Part B (Medical Insurance), to be eligible to buy a Medigap policy. Here is a step-by-step guide on how to buy a Medigap policy:

Step 1: Compare the benefits of each plan

Firstly, you need to compare the benefits of each lettered plan. Think about your current and future healthcare needs and decide which benefits you will require. Remember, you might not be able to switch policies later, so it is important to choose a plan that meets your needs both now and in the future.

Step 2: Select your plan

Once you have compared the benefits, you need to select the plan that best suits your needs. It is important to note that not all plans are offered in every state, so be sure to check the availability in your state.

Step 3: Find insurance companies selling your desired plan

After selecting your plan, you need to find insurance companies that are licensed in your state to sell that particular plan. You can buy a Medigap policy from any of these companies, but remember that not all insurance companies sell policies for every plan. You can contact your local State Health Insurance Assistance Program (SHIP) to get free help in choosing an insurance company in your area. They may also have a Medigap rate comparison shopping guide for your state.

Step 4: Get an official quote and review the policy

Before purchasing, be sure to get an official quote from the insurance company. Read the policy carefully and ask questions if anything is unclear. The insurance company must provide you with a clearly worded summary of the Medigap policy, which you should keep for your records.

Step 5: Purchase the policy

When you are ready to buy, contact the insurance company and fill out their application form. After your Medigap Open Enrollment Period ends, insurance companies are not obligated to sell you a Medigap policy unless you have Medigap protections, also known as "guaranteed issue rights". If you qualify under specific circumstances, you will need to provide proof of your situation to the company.

Important considerations:

- Medigap policies generally begin on the first of the month after you apply.

- If you do not receive your Medigap policy within 30 days, contact your insurance company. If it has been 60 days and you still have not received it, contact your State Insurance Department.

- Medigap policies must follow federal and state laws, which are designed to protect you. Be cautious of illegal practices by insurance companies and protect yourself when shopping for a Medigap policy.

Workers' Comp: Should Sole Proprietors Get It?

You may want to see also

Frequently asked questions

Medicare Supplemental Insurance, also known as Medigap, is extra insurance you can purchase from a private health insurance company to help pay for out-of-pocket costs in Original Medicare (Part A and Part B).

The "What's Covered" app is a Medicare-approved application that helps seniors quickly access information about their healthcare coverage. It allows users to find out if specific items or services are covered by their Medicare insurance.

The app provides instant access to health information, helps coordinate care with doctors and providers, and allows users to determine if a procedure is covered. It is a convenient way for seniors to understand and maximize their Medicare coverage by having immediate access to their health history, insurance claims, potential costs, and more.

The "What's Covered" app is available for free on both iOS and Android devices. You can download it from the App Store or Google Play.

Yes, there are several other Medicare-connected apps available. Additionally, you can use the Medicare Care Compare tool to find Medicare psychiatrists near you or visit online directories. You can also call the Medicare coverage helpline at 1-800-MEDICARE (1-800-633-4227) for assistance with Part A and/or Part B coverage.