Life insurance payouts are generally not taxed, but there are some exceptions. The type of policy, the size of the estate, and the method of payment can determine whether life insurance proceeds are taxed. For example, if the policy accrues interest, taxes are usually due on the interest earned. If the policyholder names their estate as the beneficiary, taxes may apply depending on the estate's value. Additionally, if the insured and the policy owner are different individuals, taxes may be involved. It is important to consult a tax advisor to understand the specific circumstances and any potential tax liabilities.

Explore related products

What You'll Learn

![]()

Interest accrued on the policy

Life insurance payouts are typically not taxed as income. However, any interest accrued on the policy is taxable and must be reported as interest received. The interest that accrues from a life insurance policy payout is generally subject to federal income tax, whether received as a lump sum or in periodic payments. This interest is taxable to the beneficiary, while the unearned premium is not as the insured party paid using after-tax dollars.

In the United States, the Internal Revenue Service (IRS) states that any interest received on life insurance proceeds is taxable and should be reported. The IRS further clarifies that if the policy was transferred for cash or other valuable consideration, the exclusion for proceeds is limited to the sum of the consideration paid, additional premiums paid, and certain other amounts. The taxable amount is generally reported based on the type of income document received, such as a Form 1099-INT or Form 1099-R.

The taxation of interest accrued on life insurance policies also depends on the jurisdiction. For example, in New York, interest on life insurance proceeds is computed from the date of death of the insured to the date of payment, according to N.Y. Ins. Law § 3214(c) (McKinney 2000). This means that interest begins to accrue from the date of death, regardless of when the claim is filed with the life insurer. Additionally, the interest rate is determined by the rate in effect as of the date of death, and it is subject to fluctuations during the period until the payment date.

Becoming a Top Life Insurance Agent: Strategies for Success

You may want to see also

Explore related products

![]()

Estate tax

In the United States, life insurance payouts are generally not considered taxable income for the beneficiary. However, there are some instances where life insurance proceeds may be subject to estate tax.

- The proceeds are paid to the insured's estate: This means that if the policyholder designates their estate as the beneficiary of the insurance policy, the payout may be subject to estate tax.

- The insured retained "incidents of ownership" in the policy: Incidents of ownership refer to certain rights and benefits associated with the policy. Even if the insured is not the named beneficiary, retaining specific rights related to the policy can trigger estate tax. These rights include:

- The right to change beneficiaries

- The right to assign or revoke the policy

- The right to pledge the policy as security for a loan

- The right to borrow against the policy's cash surrender value

- The right to surrender or cancel the policy

It is important to note that simply having these rights attached to the policy, regardless of whether they are exercised, can result in the proceeds being taxed as part of the insured's estate.

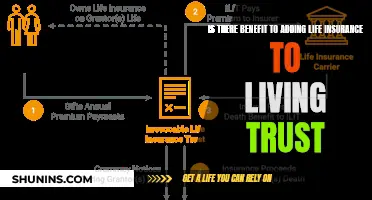

To avoid estate tax on life insurance proceeds, careful planning is necessary. One common strategy is to set up an irrevocable life insurance trust (ILIT). With an ILIT, the trust owns the life insurance policy, and the insured individual does not retain any incidents of ownership. This ensures that the proceeds are not included in the taxable estate. Another strategy is to have another person or entity apply for and purchase a new policy on the insured's life, ensuring that the insured never directly owns the policy.

The federal estate tax exemption amount is subject to change over time. For example, in 2023, the exemption was $12.92 million per person, but it is expected to decrease to approximately $6 million in 2026. Therefore, it is essential to stay informed about the current tax laws and consult with a tax professional or financial advisor when making decisions regarding life insurance and estate planning.

BECU's Whole Life Insurance Offering: What You Need to Know

You may want to see also

Explore related products

![]()

Inheritance tax

Life insurance payouts are usually tax-free, but there are some exceptions. For example, if you live in the UK and the total value of your estate is more than £325,000, inheritance tax (IHT) will be deducted from your insurance payout at a rate of 40%. This threshold is expected to remain the same until April 2026.

Your 'estate' includes your savings, investments, and material possessions, such as cars, jewellery, money, and the proceeds of any life insurance, less any debts. It also includes your home. However, if you leave your home to your children or grandchildren, the threshold increases to £425,000.

If you are married or in a civil partnership, there is no IHT payable on anything left to your spouse or civil partner. Additionally, after one partner in a married couple or civil partnership dies, any unused inheritance tax allowances can be passed to the surviving partner. This means that when they die, they could potentially pass on £1 million free from inheritance tax.

If you are cohabiting without being married, your surviving partner will have no legal claim on your estate unless you name them in your will as a beneficiary or you own property jointly. In this case, you should make a will if you want them to inherit. Even if you are unmarried, you can name your partner (or anyone else) as the beneficiary of your life insurance.

To avoid your beneficiaries having to pay IHT on your life insurance payout, you can consider placing your life insurance policy in trust. This way, the payout won't be included in your estate when you die. A trust is a legal agreement that enables you to hand over your policy to trustees, who become the legal owners and manage it on behalf of the beneficiaries. You can choose family members, friends, or a solicitor to be trustees. While there is no time restriction for placing your policy in a trust, it is generally recommended to do it as early as possible, preferably when you first take out the cover.

Cash Value Life Insurance: A Bad Bet for Your Money

You may want to see also

Explore related products

![]()

Income tax

Life insurance payouts are generally not considered taxable income and do not need to be reported as such. However, there are certain scenarios where you may have to pay federal or state income taxes on the proceeds.

When the beneficiary is an estate

If there are no named beneficiaries on the policy, the life insurance proceeds may be included in the deceased's estate. If the value of the estate exceeds the federal estate tax threshold, which was $13.61 million as of 2024, estate taxes must be paid on the amount that is over the limit. Some states also assess inheritance or estate taxes, depending on the estate's value and location.

When the insured and the policy owner are different individuals

If a different person holds each role, there may be taxes involved.

When receiving the payout in installments

If a beneficiary chooses to receive their payout in installments over several years instead of a lump sum, any interest accrued by the annuity account may be subject to income taxes. The principal death benefit is still not taxed.

When withdrawing money from the cash value

Both whole life insurance and universal life insurance policies earn interest, referred to as cash value, and policyholders may be able to make withdrawals or take out a loan against the balance. If the withdrawal or loan is more than the total amount of premiums paid, the excess can be taxed.

When surrendering the policy

If you cancel a whole life or universal life insurance policy, you typically receive the cash surrender value, which is your policy's cash value minus any fees. While you don't have to pay taxes on the principal when it's returned, any cash value your policy has accrued will be taxed as income.

When selling the policy

If you sell your policy to a third party, the sales proceeds may be subject to income taxes if they exceed your cumulative premiums, minus the portion of your premiums attributed to the cost of insurance.

Calculating Life Insurance: The Essential Guide for Beginners

You may want to see also

Explore related products

![]()

Generation-skipping tax

Generation-Skipping Transfer Tax (GSTT)

The generation-skipping transfer tax is a federal tax on transfers of assets or property to individuals who are more than one generation below the transferor. This includes transfers from a grandparent to a grandchild or to individuals who are more than 37.5 years younger than the transferor (the "skip" generation). This tax is equal to the highest federal gift and estate tax rate at the time of transfer (40% in 2024) and is in addition to any other federal gift or estate tax owed.

The GSTT was introduced in 1976 to prevent what the IRS perceived as wealthy families avoiding estate taxes at the death of each generation. Prior to this tax, it was possible to pass an unlimited amount of assets to a trust for the benefit of multiple generations, thus permanently avoiding estate taxes as each generation passed away.

The GSTT only applies to transfers over an exemption amount, which for 2024 is $13,610,000 per person or $27,220,000 for a married couple. This exemption is scheduled to revert to $5 million, indexed for inflation, in 2026.

There are two types of skips:

- Direct skip: When the transferor gifts assets directly to a skip person, and they have immediate ownership rights.

- Indirect skip: When someone transfers money to an entity (such as a trust) that may eventually distribute assets to a skip person.

The GSTT affects only the very wealthy since the federal estate tax exemption is currently $13.61 million per person.

Life Insurance Payouts and Taxes

Life insurance payouts are generally not taxable. However, there are some exceptions:

- If the policy accrued interest, taxes are usually due on the interest accrued.

- If the policyholder names their estate as a beneficiary, taxes may apply depending on the estate's value.

- If the insured and the policy owner are different, there may be taxes involved.

Life Insurance Tax Laws in Texas: What You Need to Know

You may want to see also

Frequently asked questions

Life insurance payouts are generally not taxable. However, there are certain exceptions. The type of policy, the size of the estate, and the method of payment can determine if the proceeds are taxed.

Some common situations where beneficiaries might owe taxes on life insurance include:

- The policy accrued interest.

- The policyholder names their estate as a beneficiary.

- The insured and the policy owner are different individuals.

There are some strategies beneficiaries can use to avoid paying taxes on a life insurance payout, such as:

- Use an ownership transfer.

- Create an irrevocable life insurance trust (ILIT).