Medicare Supplement Insurance, also known as Medigap, is an optional add-on that can help cover out-of-pocket costs and gaps in Original Medicare (Part A and Part B) coverage. While Medicare Part A and Part B cover a large share of healthcare costs, they do not have maximum out-of-pocket caps, and there is no limit to how much you could owe in copays and coinsurance. Medigap policies help fill these coverage gaps by paying for deductibles, coinsurance, and other out-of-pocket costs, providing financial protection against unexpectedly high medical expenses. However, it is important to note that Medigap policies do not cover prescription drugs, dental care, routine eye care, or long-term care. The best time to purchase a Medigap policy is when you turn 65 and enroll in Medicare Part B, as you are guaranteed acceptance and cannot be denied coverage based on your health or medical history.

| Characteristics | Values |

|---|---|

| What is Medicare Supplemental Insurance? | Extra insurance to help pay your share of out-of-pocket costs in Original Medicare. |

| Who can buy it? | Anyone with Medicare Part A and Part B is eligible. |

| When to buy it? | The best time to buy is within 6 months of getting Medicare Part A and Part B when you turn 65. |

| Why buy it? | To cover out-of-pocket costs, deductibles, co-payments, and coinsurance costs not covered by Original Medicare. |

| What does it cover? | Most Medigap plans cover the Part A deductible. Some plans cover 50% of Part B coinsurance, while others cover the entire Part B coinsurance. Some plans also offer coverage for vision, hearing, and dental services. |

| What doesn't it cover? | Medigap policies generally do not cover prescription drugs, dental care, routine eye care, or long-term care. |

| Cost | You need to pay premiums throughout the year, which can vary based on plan type, age, location, and health status. |

Explore related products

$7.97 $10.97

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is an optional extra insurance that can be purchased from a private health insurance company. It helps to pay your share of out-of-pocket costs in Original Medicare (Medicare Part A and Part B). While it is not compulsory to have Medicare Supplement Insurance, it is recommended if you can afford it, as it can protect you from unexpectedly high out-of-pocket costs.

Medicare Part A and Part B do not have maximum out-of-pocket caps, meaning there is no limit on what you could owe in copays and coinsurance. Medigap policies can help to cover these large bills. Most Medigap plans cover the Part A deductible, which in 2024 was $1,632. This means that if you have a hospital stay, you will be paying this deductible, and your costs can add up quickly. Plans with premiums below $136 per month could put you ahead based on this benefit alone. After meeting your deductible, there are still out-of-pocket costs for many Medicare services, such as a 20% coinsurance for most medically necessary outpatient services covered by Part B. Medigap policies may also pay Medicare deductible amounts, except for the Part B deductible.

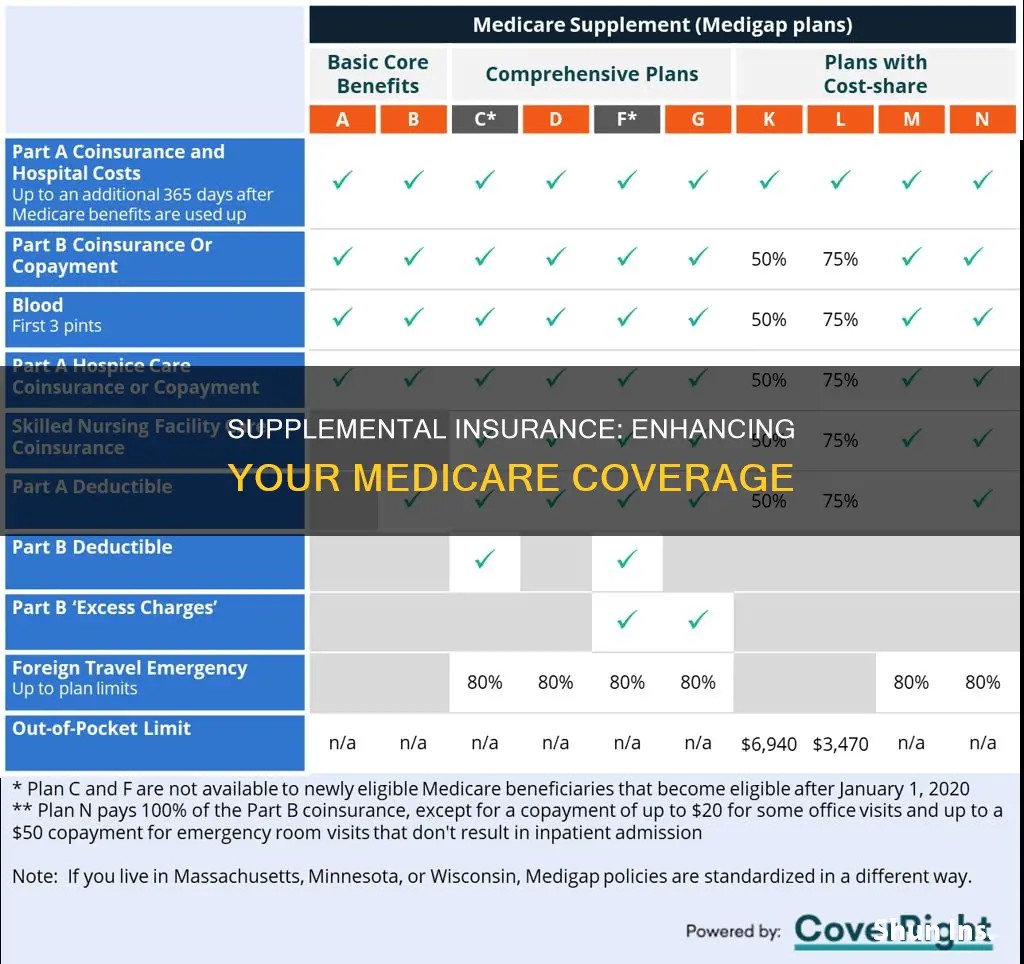

Medigap policies are standardized, and in most states, they are named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, no matter which insurance company sells it, and the price is the only difference between policies with the same letter sold by different companies. In Indiana, there are eight standard plans offered, labelled with letters A through N. The premium for a Medigap policy can be calculated in one of three ways: Issue Age, Attained Age, or No Age Rating. Issue Age means that if you were 65 when you bought the policy, you will pay the same premium the company charges people who are 65, regardless of your age. Attained Age means the premium is based on your current age and will increase as you get older. No Age Rating means everyone pays the same premium, regardless of age.

The best time to buy a Medigap policy is when you turn 65 and enroll in Medicare Part B. This is known as the Medigap Open Enrollment Period (OEP), and it lasts for six months. During this period, insurance companies cannot refuse to sell you a policy or charge you a higher premium based on your health or medical history. After this period, it may be more challenging or more expensive to obtain a Medigap policy.

Montana: Insurance Proof a Must

You may want to see also

Explore related products

![]()

Out-of-pocket costs

Medicare Supplement Insurance, also known as Medigap, is extra insurance that you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. Medigap policies are sold by private carriers to provide wraparound coverage for Medicare Parts A and B costs. However, they do not cover Medicare Advantage (Part C) or Part D drug plans.

Medigap premiums vary depending on the insurance company, the plan, and where you live. The insurance company you choose affects your Medicare supplement costs because each carrier determines its own rates. The benefits in each lettered plan are the same, regardless of which insurance company sells it. The premium amount is the only difference between policies with the same plan letter sold by different companies.

There are a variety of choices for Medicare supplement plans, and the premium and out-of-pocket expenses can vary significantly depending on the coverage you pick and your health needs. The Medicare supplement plans that offer the most coverage will usually cost you more each month. The main factors that affect your Medicare supplement costs include your age, gender, residential area, and smoking status, in addition to the type of Medigap plan you choose.

Medigap policies may also offer discounts that can lower your costs. For example, some companies offer discounts for women, non-smokers, married people, paying yearly, or using electronic funds transfer for premiums. Additionally, some Medigap policies include extra benefits, such as coverage when you travel out of the country.

How Moving Violations Affect Your Insurance Rates

You may want to see also

Explore related products

![]()

Medigap policy costs

The cost of a Medigap plan depends on several factors, including the type of plan, where you live, and the insurance company. Medigap premiums (the amount you pay each month) vary depending on the insurance company, the plan, and where you live. There can be significant differences in the premiums that different insurance companies charge for the same coverage. Therefore, it is essential to compare Medigap plans with the same letter when shopping for a policy. For example, compare Plan G from one company with Plan G from another company.

Medigap policies cover certain copays, coinsurance, and deductibles that you would otherwise be responsible for after Medicare pays its share of covered services. The cost of a Medigap plan can also depend on whether the insurance company offers discounts, such as discounts for women, non-smokers, married people, paying yearly, or using electronic funds transfer for premium payments. Additionally, some companies may offer discounted rates for multiple policies.

Medigap premiums can also vary by state and policy type. For example, in 2023, the average monthly premium for people enrolled in Plan G ranged from a low of around $140 in D.C., Hawaii, and New Mexico to $236 in New York. Generally, you'll pay lower premiums for high-deductible plans or plans with less coverage, like Plan K or Plan L. Conversely, plans that cover more, such as Plan G, tend to have higher premiums.

Medigap Plan F and Plan G offer a high-deductible option, with lower monthly premiums but a higher deductible before the plan starts to cover costs. In 2025, the deductible for these plans is $2,870. Medigap Plan K and Plan L have out-of-pocket limits, which are the maximum amounts you'll have to pay before the plan pays 100% of the covered services for the rest of the year. In 2024, the out-of-pocket limits for Plan K and Plan L were $7,220 and $3,610, respectively.

Medigap plans can range from $30-$40 per month on the lower end to hundreds of dollars per month on the higher end. When choosing a Medigap plan, it is important to compare the costs and benefits of different plans and insurance companies to find the best option for your needs.

Understanding Insurance Costs in Manufacturing Overhead

You may want to see also

Explore related products

![]()

Medigap eligibility

Once you have enrolled in Original Medicare, you are guaranteed issue for Medigap during a six-month window known as the Medigap Open Enrollment Period. This period begins when you turn 65 and enrol in Medicare Part B. During this time, you can enrol in any Medigap policy, and insurance companies cannot deny you coverage due to pre-existing health conditions. After this period, your options to purchase a Medigap policy may be limited, and the policy may cost more. Additionally, in most states, insurers can use your medical history to determine your premium and eligibility for coverage.

It is worth noting that if you are under 65 and eligible for Medicare due to a disability, Amyotrophic Lateral Sclerosis (ALS), or End-Stage Renal Disease (ESRD), the availability of Medigap depends on the state where you live. Some states allow you to buy a Medigap policy if you are eligible for Medicare due to these reasons. Therefore, it is important to check with your State Insurance Department about your rights under state law.

Furthermore, there are ten standardized Medigap plans offered in most states, named by letters: A-D, F, G, and K-N. The most comprehensive plan available to newly eligible enrollees is Plan G, which covers nearly all out-of-pocket costs for services covered by Original Medicare. On the other hand, Plan K is less expensive in terms of monthly premiums but only covers 50% of most Original Medicare out-of-pocket costs until a certain amount is reached.

In summary, to be eligible for Medigap, you must first enrol in Original Medicare Part A and Part B, and then you can take advantage of the Medigap Open Enrollment Period to select a plan that best suits your needs.

Earthquake Insurance: Admitted Carrier?

You may want to see also

Explore related products

![]()

Medigap vs. Medicare Advantage

When you're getting started with Medicare, you have two options: you can either buy Medigap or enroll in a Medicare Advantage Plan. However, you can't have both at the same time.

Medigap, or Medicare Supplement Insurance, is a supplement to Original Medicare coverage. It is sold by private companies that fill the "gaps" in Original Medicare by covering some out-of-pocket expenses, such as deductibles and copays. Medigap policies only cover one person, so if you and your spouse both want Medigap coverage, you will each have to buy your own policy. Generally, you must have Original Medicare (Part A and Part B) to buy a Medigap policy. Medigap plans sold after 2005 do not include prescription drug coverage, so if you want prescription drug coverage, you will need to join a separate Medicare drug plan (Part D).

Medicare Advantage, also known as Medicare Part C, is an alternative to Original Medicare that is offered by private health insurers. It covers the same benefits as Medicare Part A and Part B, and usually Part D (prescription drugs), and often includes extra benefits such as dental, vision, and hearing coverage. Medicare Advantage plans have provider networks, and you will usually have to pay more or may not be covered if you go to a doctor or facility outside of the plan's network.

Medigap plans give you the freedom to see any doctor that accepts Medicare, whereas Medicare Advantage plans generally require you to get care within the plan's network of providers. Medicare Advantage plans tend to have low or no monthly premiums, whereas Medigap plans can be quite a bit more expensive.

Understanding Insurance Premiums for Learner Drivers

You may want to see also

Frequently asked questions

Medicare Supplemental Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help pay out-of-pocket costs in Original Medicare (Part A and B).

Medicare Supplemental Insurance covers the gaps in Original Medicare, including deductibles, co-payments, coinsurance, and other medical expenses not fully covered by Medicare. It is important to note that Medigap does not cover prescription drugs, dental care, routine eye care, or long-term care.

Medicare Supplemental Insurance is advisable for individuals with Original Medicare who want additional financial protection against out-of-pocket costs and gaps in coverage. It is essential to consider your specific needs, budget, and eligibility when deciding whether to purchase a Medigap policy.

The best time to purchase Medicare Supplemental Insurance is during the Medigap open enrollment period, which starts when you turn 65 and enroll in Medicare Part B. During this six-month period, insurance companies cannot use medical underwriting to charge higher rates or deny coverage based on health history.