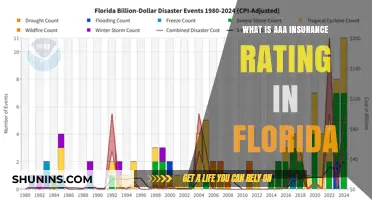

Florida is facing an insurance crisis as insurance companies are leaving the state, causing rates to skyrocket and leaving many property owners struggling to find affordable coverage. The crisis is caused by a combination of factors, including the high frequency of hurricanes and litigation costs. The state's vulnerability to extreme weather conditions and the resulting cleanup costs have significantly impacted insurance companies, with some choosing to pull out of the state entirely. Additionally, Florida experiences a disproportionately high number of homeowner lawsuits, leading to increased financial strain on insurance providers. The crisis has left many residents turning to state-backed insurance options, such as Citizens Insurance, which may not always provide optimal coverage. However, new legislation and the entry of new companies into the market are showing signs of easing the crisis.

| Characteristics | Values |

|---|---|

| Insurance companies that have left Florida | Progressive, Farmers, AAA, Bankers Insurance, Centauri Insurance, Lexington Insurance, St. Johns Insurance Company, Universal Health Care Insurance Company |

| Reason for leaving | Soaring litigation costs, fraudulent claims, and extreme weather threatening the market in the state |

| Impact | Over 100,000 homeowners are struggling to find new coverage, with many turning to state-backed Citizens Insurance |

| Legislative response | Senate Reform Bill 2-A passed in December 2022 to address insurance issues; Florida Office of Insurance Regulation approved 30+ new "take-out companies" |

Explore related products

What You'll Learn

![]()

Insurers are leaving due to the high litigation costs in Florida

Florida has been facing an insurance crisis, with several insurance companies leaving the state or reducing coverage. Some of the insurers that have exited Florida include Progressive, Farmers, AAA, Bankers Insurance, Centauri Insurance, and Lexington Insurance.

One of the key factors contributing to this crisis is the high litigation costs in the state. Florida leads the nation in homeowners' insurance-related litigation, accounting for about 79% of such lawsuits across the United States, while only 9% of the total claims originate in Florida. This disparity has resulted in significant financial losses for insurance companies.

The Insurance Information Institute (Triple-I) identified a 2017 State Supreme Court decision as a significant factor in the increase in litigation costs. This decision allows courts to award attorneys with higher hourly billing rates, sometimes two to two-and-a-half times their standard rate when ruling in favor of policyholders. This has incentivized more litigation and has been a contributing factor in the rise of roofing scams and fraudulent claims.

The high litigation costs have had a substantial impact on insurance premiums in Florida. Homeowners in the state pay an average of $6,000 per year for homeowners insurance, a 42% increase from the previous year. This is significantly higher than the national average of $1,700. The litigation costs have also contributed to insurance companies going insolvent or pulling out of the state, as they struggle to manage the financial burden.

In response to the crisis, Florida lawmakers passed Senate Reform Bill 2-A in December 2022 to address pressing insurance issues. Additionally, the Florida Office of Insurance Regulation (OIR) has approved more than 30 new "take-out companies" to provide alternative coverage options for residents. While these measures are expected to improve the situation over time, Florida continues to grapple with the challenges of high litigation costs and their impact on the insurance market.

Change of Heart Insurance: Protection for the Fickle

You may want to see also

Explore related products

![]()

Florida's high hurricane risk is a major factor

Florida has been hit by the most number of hurricanes since direct hits on land were first recorded in 1851. More than 41% of hurricanes that hit the United States also make some kind of landfall in the Sunshine State. Florida has also been hit by more than twice as many hurricanes as the next closest hurricane-prone state, Texas. Of the 292 hurricanes that have hit the U.S. since 1851, 120 have made some sort of landfall in Florida.

The northwest panhandle of Florida is the most hurricane-prone area in the state. It has been hit by the most hurricanes since 1851, with Hurricane Michael in 2018 being a Category 5 hurricane and one of the strongest on record. Sitting on the Gulf of Mexico, which has much warmer waters than the Atlantic Ocean, southwest Florida is tied with its southern counterpart on the Eastern Seaboard as the second most hurricane-prone area in the state.

The southeast coastline is extremely susceptible to a land-falling hurricane, followed by the panhandle. Areas around Tampa, Jacksonville, and the Big Bend do not have as high a risk of a direct strike from a hurricane but are still susceptible to a landfall each year. Even if the hurricane makes landfall elsewhere in the state, the impacts can be felt hundreds of miles away.

Florida's flat terrain means that strong winds do not rapidly weaken after a hurricane makes landfall. Hurricane Charley in 2004 moved through the state at 25 mph (nearly twice the typical speed of a landfalling hurricane) and brought hurricane-force winds to Orlando, which was nearly 100 miles away from the point of landfall. The strongest hurricanes can have winds in excess of 155 mph.

Hurricanes in Florida have caused billions of dollars in damage. Cleaning up after a major storm is expensive; Hurricane Ian caused an estimated $109 billion in damage in Florida alone. As a result, insurance companies may decide to pull out of the state. In addition to the risk of extreme weather, litigation costs are also a factor in insurance companies leaving Florida.

Verizon Phone Insurance: Does It Cover Broken Screens?

You may want to see also

Explore related products

![]()

Insurers are struggling to pay out more in claims than they take in

Florida is facing an insurance crisis, with rising premiums and a growing number of insurers leaving the state. Insurers are struggling to pay out more in claims than they take in, and this is causing them to raise their rates or leave the state.

Insurers in Florida are facing a challenging situation where they are paying out more in claims than they are taking in through premiums. This is due to a combination of factors, including the frequent occurrence of hurricanes and other extreme weather events, as well as high litigation and fraud costs.

Hurricanes and extreme weather events have had a significant impact on Florida, with storms like Hurricane Ian causing an estimated $109 billion in damage. As a result, insurance companies have been faced with a large number of claims, and the cost of repairs has often exceeded what insurers are willing to pay. In some cases, insurers have been accused of slashing payouts far below damage estimates, leaving homeowners to foot the bill for repairs.

Litigation and fraud costs have also contributed to the challenges faced by insurers in Florida. The state sees a disproportionately high number of homeowner lawsuits, with about 9% of homeowner property claims nationwide filed in Florida but 79% of lawsuits related to property claims. Fraudulent practices, such as contractors claiming for new roofs when there is minimal damage, have also added to the financial strain on insurance companies.

The combination of high claims, litigation, and fraud costs has led to insurers struggling to remain profitable in Florida. In some cases, insurers have had to increase premiums to make up for losses, while others have chosen to leave the state altogether. This has resulted in a challenging situation for homeowners, who are facing higher insurance costs and difficulty in obtaining coverage.

While the Florida insurance crisis is causing concern, there are some signs of improvement. New legislation, such as the Senate Reform Bill 2-A, aims to address insurance issues, and new insurance companies are entering the market. However, it will take time for these changes to have a significant impact, and in the meantime, insurers and homeowners continue to navigate a complex and challenging environment.

Insurance: A Commodity or Not?

You may want to see also

Explore related products

![]()

Fraudulent claims and scams are also an issue

Florida's home insurance crisis is the result of several factors, including hurricanes and litigation, causing home insurance companies to pull back, leave the state, or go out of business. Fraudulent claims and scams are also an issue.

Insurance fraud and scams are a significant problem in Florida, with around 79% of home insurance lawsuits in the US occurring in the state, despite only 9% of home insurance claims originating there. Fraudulent claims by homeowners are a common type of insurance scam in Florida. For example, an employee can commit workers' compensation insurance fraud by filing a claim for a fake injury or exaggerating the extent of their injuries to obtain benefits. This type of fraud is a third-degree felony in Florida, punishable by fines, civil liability, and jail time.

Another scam involves individuals pretending to represent an insurance company and offering to sell or increase coverage immediately before or after a disaster, such as a hurricane. During such times, many legitimate insurance companies cease binding new or additional coverage, making these unsolicited offers suspicious.

To protect themselves, Floridians should be wary of unsolicited calls and verify the identity of anyone claiming to represent an insurance company. They should also ensure that contractors and repair companies are legitimate and have the proper liability and workers' compensation insurance coverage.

The Florida government has been attempting to address the insurance crisis. In December 2022, Florida lawmakers passed the Senate Reform Bill 2-A to address some of the state's most pressing insurance issues. Additionally, the Florida Office of Insurance Regulation (OIR) has approved more than 30 new "take-out companies" to remove policyholders from Citizens Insurance, the state-backed insurer of last resort, which has been criticised for subpar coverage.

Florida's Insurance Pre-Appointment Requirements: What You Need to Know

You may want to see also

Explore related products

![]()

Some insurers are reducing coverage, rather than leaving

Florida has been experiencing an insurance crisis, with many insurance companies leaving the state. This has resulted in higher rates and reduced coverage options for homeowners. However, some insurers are choosing to reduce coverage rather than leaving the state altogether.

The Florida insurance crisis has been caused by several factors, including hurricanes, litigation costs, and fraud. The risk of extreme weather events, such as hurricanes, has led to significant financial losses for insurance companies. Additionally, soaring litigation costs and fraudulent claims have contributed to the crisis. In response, some insurance companies have tightened their underwriting restrictions and eligibility requirements to reduce the risk of scams and lower their financial exposure.

For example, companies such as Southern Fidelity, Progressive, and Universal have chosen to continue operating in Florida but have non-renewed tens of thousands of policies. They have also requested substantial rate increases to offset their losses. This has resulted in reduced coverage for many homeowners, as they are forced to find new insurance providers or pay higher premiums.

The impact of the insurance crisis is felt particularly in high-risk coastal areas, where the threat of hurricane damage is greater. Homeowners in these areas may struggle to find affordable coverage or any coverage at all. The crisis has also affected the real estate market, as buyers and sellers are impacted by the lack of available and affordable insurance options.

While the Florida insurance crisis has caused disruptions, there are signs of improvement. New legislation has been enacted to curb fraudulent claims and reduce litigation costs. Additionally, new insurance companies are entering the market, providing alternative coverage options for homeowners. Rate decreases have also been announced for state-backed Citizens Insurance, offering some relief to those struggling to find affordable coverage.

Citi Double Cash: Cell Phone Insurance Coverage Explained

You may want to see also

Frequently asked questions

Farmers Insurance, Progressive, AAA, Bankers Insurance, Centauri Insurance, Lexington Insurance, St. Johns Insurance Company, Universal Health Care Insurance Company, and Physicians United Plan are among the insurance companies that have left Florida.

There are several factors contributing to the Florida insurance crisis, including hurricanes and litigation, that have caused home insurance companies to pull back, leave the state, or even go out of business. Florida sees a disproportionate number of homeowner lawsuits compared to other states.

The Florida homeowners insurance market is on the brink of a collapse, with thousands of homeowners struggling to find affordable coverage. Many homeowners have no choice but to turn to state-backed Citizens Insurance, which may not be a reliable option in the face of a major disaster.